Capital markets around the globe have been in a state of turbulence since the shock delivered by the COVID pandemic. Even as many countries exit this crisis, other issues, unfolding simultaneously and on multiple timescales, ensure that uncertainty remains high: the war in Ukraine, the ensuing inflation (and rising interest rates), instability in the banking sector, and the escalating threat of climate change. Given this persistent, multi-dimensional uncertainty, discount rates have risen, putting companies whose valuation rests on their long-term growth potential under particular threat.

Calibrating and putting these events into perspective is difficult: Are we witnessing a durable shift of focus towards short-term results, at the expense of long-term growth? Will the tech sector, which has been a growth engine, stagnate?

One way of gaining some perspective is by assessing shifting patterns in “vitality”—a measure of firms’ long-term growth potential. For the past five years, BCG and Fortune have published the Future 50, an index of the world’s most vital companies. Underlying this index is a predictive model, which quantifies a company’s long-term prospects based on a variety of financial and non-financial indicators, such as a company’s strategic orientation, its investments in technology, the quality of its patent portfolio, the diversity of its leadership, and its recent sales growth (read more on our methodology here). Our hypothesis, which has been borne out by results so far, is that these most vital companies will outperform the broader corporate universe in the longer run, both in revenue growth and shareholder returns.

We will publish the next Future 50 ranking in December 2023. In the meantime, we ran an interim analysis to cut through the short-term noise and provide a window into trends in the growth potential of the corporate economy.

Key trends in vitality from previous analysis

Our previous reports have shown that it is possible for any company, regardless of its industry or geography, to achieve high vitality. However, in aggregate, the most vital companies were tech-focused—concentrated in the IT and communication services industries or deploying digital technology intensively and disruptively in other sectors. The rising importance of sustainability as a business model opportunity has been reflected in an increasingly strong showing of green tech and renewable energy firms in the index. In 2020 and 2021, driven by the COVID pandemic, a number of health care players also achieved high vitality.

From a geographic perspective, the U.S. has historically dominated the index, with China taking a strong second place, while the rest of the world was more scarcely represented in the upper ranks.

What’s new (and what has stayed the same) in vitality?

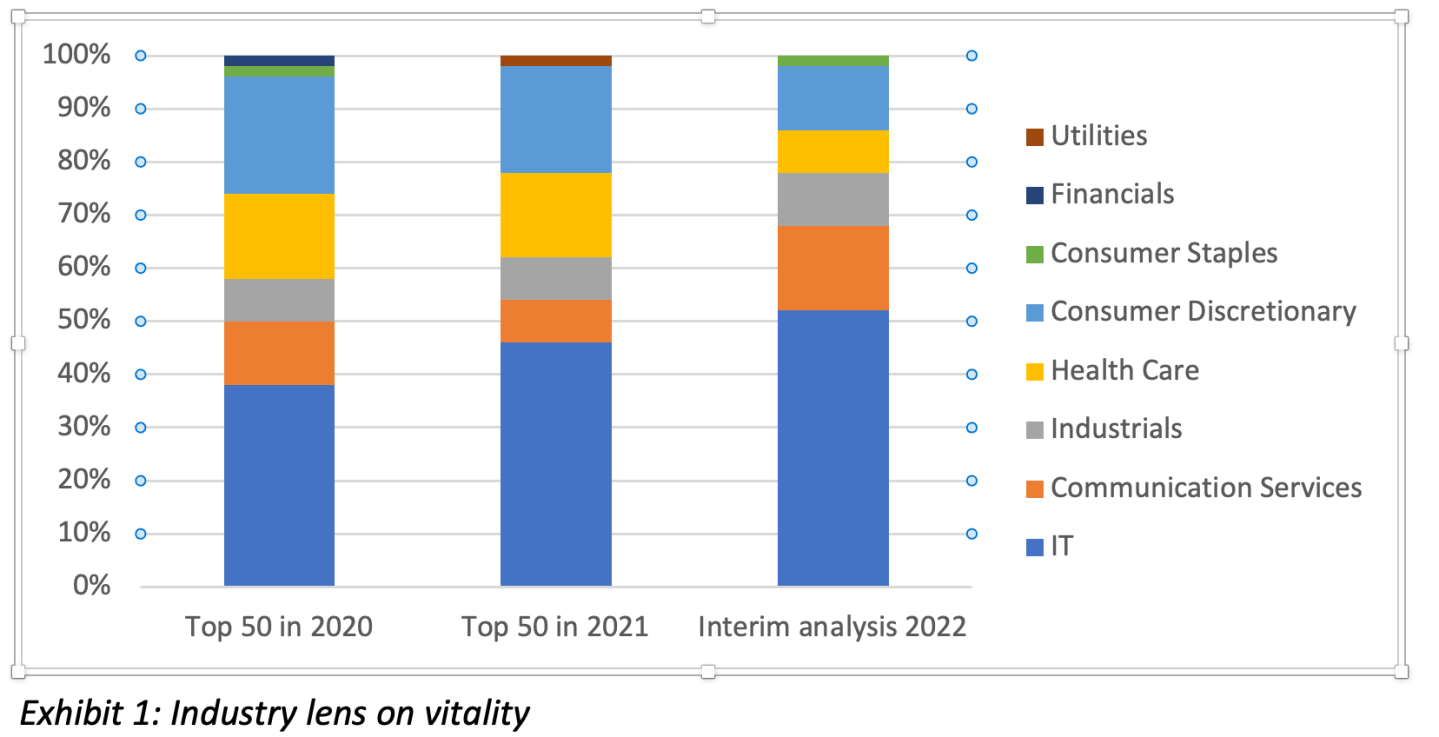

Industry view: Tech continues to be the dominant source of growth

As in previous years, tech-focused companies, particularly from the IT and communication services sectors, dominate vitality scores in our interim analysis. This trend continues even as these companies were significantly revalued by the market in 2022, with the MSCI World Information Technology index being down about 30% over the year (vs. a reduction of about 19% of the MSCI World) and in spite of a constant stream of headlines reporting on layoffs in this sector, with more than 150,000 employees being affected in recent months.

However, on closer inspection, the tech giants have made significant net additions to staff numbers over the past two years. As such, the recent dismissals can be interpreted as a short-term correction for recent over-hiring, given heightened investor pressure on profitability—and not an indicator of a lack of growth potential. Indeed, our analysis suggests that the long-term outlook for sectors such as business or consumer software and services, as well semiconductors, remains positive—and it is these segments in which many of the most vital tech players operate.

Business software: Under threat of possible recession and facing higher costs of capital, many businesses have been delaying or reducing investments in IT or cloud services; that said, the digital transformation of the workplace will almost certainly continue. Thus, companies providing tools that streamline operations, enhance efficiency, bolster (cyber-)security, or unlock new sources of value (e.g., marketing tech) still have room to grow.

One way in which some highly vital companies are succeeding in these challenging times is by reducing the costs of exploration—i.e., finding cheaper ways to build potential future sources of advantage. This is particularly crucial in times of constrained or expensive resources, such as labor and capital. Firms can do this by paying more attention to their customers’ execution and search processes, mining valuable information from them that informs their own exploration. For example, Datadog—a provider of monitoring and analytics tools in the cloud, ranked #3 on the 2021 Future 50 index—accepts user contributions to its software through an open-source model, which allows the company to extract clear signals on new functionalities their clients want. Such a strategy both reduces the costs of exploration and makes the firm more attractive to customers, which is particularly beneficial as many firms are consolidating cloud spendings with fewer providers.

Consumer software: Consumers continue to turn to their digital devices for entertainment, a trend that has stabilized at a high level as much of the world has emerged from COVID lockdown. While growth is cooling off in some core sectors, such as streaming (e.g., for Netflix and Disney+), our analysis suggests that players providing technology or services solutions for marketing, delivering, and monetizing entertainment (e.g., streaming technology platforms, marketing tech, and payment providers) continue to be well-positioned for growth. An example is The Trade Desk, #27 on the 2021 index, which specializes in digital marketing automation and personalization, and, in a challenging environment, has been able to outpace its peers and gain significant market share.

Semiconductors: The semiconductor industry also faced a difficult 2022, as demand for consumer electronics slowed down and the sector was hit by trade restrictions, with President Biden doubling down on export controls of advanced chip manufacturing equipment to China. However, in the long term, demand for computing power and data storage, electric cars, and industrial applications (e.g., automation) means that there is still plenty of room for growthfor companies like Nvidia, #49 on the 2021 Future 50—though it remains to be seen how much of that growth producers in different geographies will be able to capture.

The rise of climate tech continues

Continuing a trend from recent years, climate tech companies, e.g., those developing components for solar panels and batteries, score highly on vitality. This segment will continue to grow as the effects of climate change (and changing societal perceptions) compel governments and firms around the globe to transition towards more sustainable energy sources and systems.

Green tech is not a game exclusive to young, purpose-built companies: incumbents can also reposition for growth. For example, Chinese firm Tongwei Co started out as fish feed supplier in 1995, but identified a way to leverage its established connections to fish farmers throughout the country to enter the sustainable energy field, as state policies encouraged the set-up of photovoltaic power stations on unused spaces of land and water. Tongwei expanded into the development and production of photovoltaic modules, creating solar fishery projects, in which solar farms provide shade to the fish ponds, increasing the yield of seafood—and has become the world’s largest supplier of polysilicon, a key solar material, in the process.

Health care players are coming back down to earth

The health care sector experienced accelerated growth during the pandemic, which was reflected in some players topping the vitality charts, particularly from the biotechnology field (e.g., vaccine makers Moderna and Chongqing Zhifei Biological achieved ranks #6 and #35, respectively, on the Future 50 in 2021). While analysts continue to expect the long-term prospects for this sector to be strong, some of the boost provided by the pandemic has receded.

Old-economy companies continue to lag behind

In aggregate, sectors like financials, utilities, real estate, and consumer staples continue to lag behind in terms of vitality. In some of these sectors, there are tangible limits to growth due to encroaching constraints on natural resources, labor, and capital, as well as a less obvious scope for innovation. However, there are always firms that buck the trend, by viewing constraints as opportunities for differentiation and growth. One option is to expand into the digital realm to find innovative, less resource-intensive paths to growth: for example, fitness apparel company Lululemon athletica (#30 of the 2021 Future 50) acquired Mirror, a tech start-up selling fitness mirrors for working out at home, in 2020, expanding into digital fitness subscription services. Lululemon is using the service to build a community of fitness enthusiasts, which will also help the success of its core business.

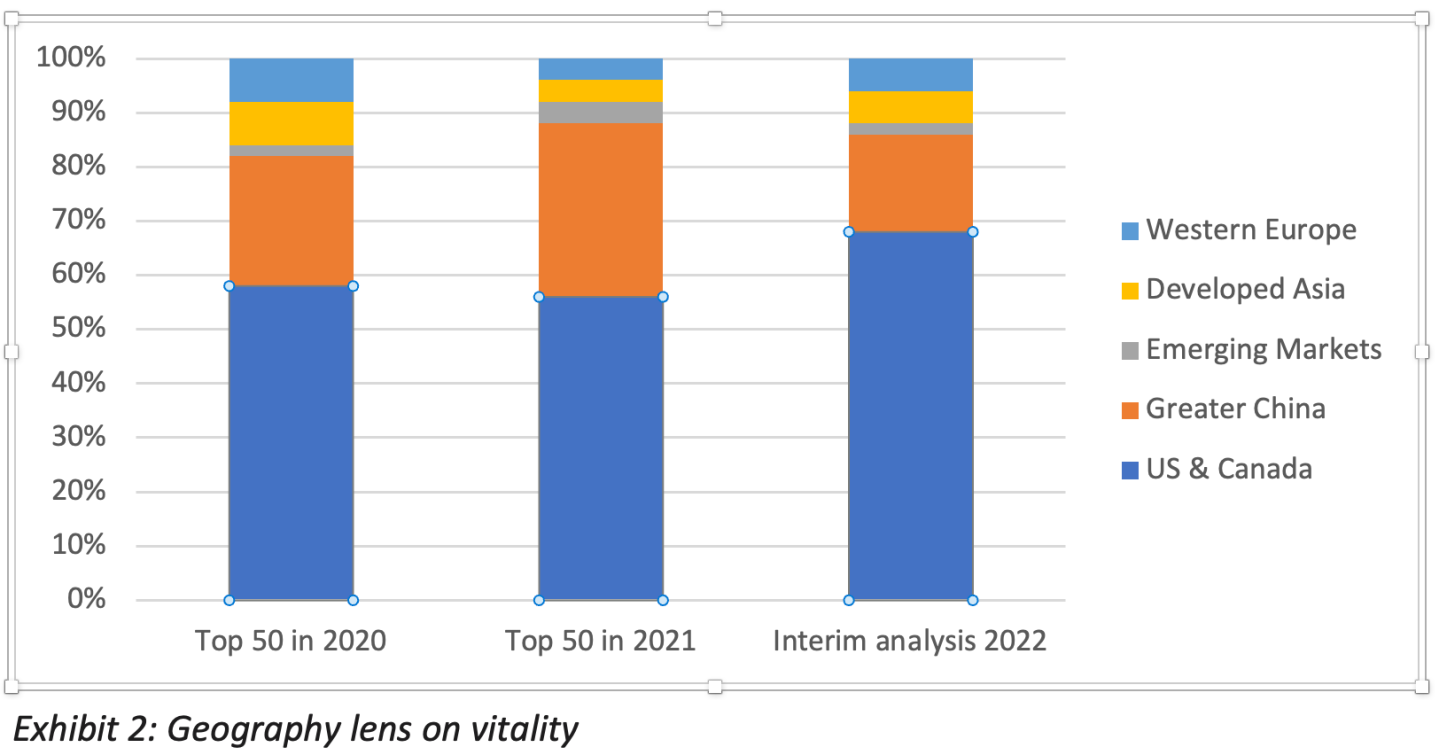

Geography lens on vitality

The U.S. extended its lead in the vitality rankings

The historical dominance of the U.S. in our vitality rankings can be explained by structural advantages, such as a mature venture capital industry, strong entrepreneurial activity, and a well-established technology industry. In 2022, this position was further bolstered by the relative strength of the U.S. economy, which has seen a faster recovery than others from the COVID-induced crisis.

China’s vitality waned somewhat—but it remains in second place

The Chinese economy was under pressure in 2022 due to, first, COVID lockdowns and, subsequently, persistent outbreaks. A troubled real estate market and geopolitical tensions have also contributed to a difficult environment for Chinese companies to remain vital in. Of those companies that continue to score highly on vitality, more than half hail from the green technology sector. Here, China has ambitious goals—it is racing to produce 33% of its energy with renewable sources by 2030, and has put significant subsidies into developing and capturing the market domestically and globally. Other vital Chinese players are mostly concentrated in the tech space.

Europe continues to struggle on vitality

Finally, Europe continues to lag behind in terms of vitality. This is driven by lack of VC funding and the fragmentation of the market, with few global champion technology enterprises. The outbreak of war on the continent and surging energy prices amplified these effects in 2022.

Diversity matters, but progress is still slow

In past analyses, we have found that companies scoring highly on vitality tend to be more diverse in terms of gender—likely due to a resulting greater capacity for innovation and reinvention, which is key to achieving growth. This continues to be the case, with the most vital companies having higher shares of female executives (median 17% vs. 13%) and managers (30% vs. 27%) than other players. Still, these statistics show that there is a long way to go yet to achieve gender parity and that progress on this front remains slow—for the market overall and even for the most vital companies.

Overall continuity—but with new trends emerging

Empirical evidence shows that long-term returns are predominantly driven by differential growth, particularly in volatile times. As such, companies and investors alike should be careful of sacrificing long-term growth potential for short-term returns even at an elevated cost of capital. Our analysis helps make sense of trends in vitality—by showing that, while the world has experienced much short-term turbulence, there is much continuity in these trends. Moreover, while the environment is the most difficult it has been for growth-oriented companies in at least two decades, we show that companies can succeed in remaining vital. Some of the keys to success are enhancing efficiency in the search for new growth options (e.g., Datadog) and looking for growth opportunities outside of one’s traditional core business—ideally linked to sustainable or less resource-intensive approaches (e.g., Tongwei, Lululemon).

Even as we write this report, new trends are emerging that may change the picture again. For one, the recent fall of SVB added financial instability to macroeconmic landscape, making recession or even structural break more probable. The other elephant in the room is artificial intelligence, which appears poised to disrupt industries and workflows. For a comprehensive view on how these trends will affect long-term growth prospects, watch this space for our full update on the state of vitality, including the Future 50 index, in December 2023.

Martin Reeves is a managing director and senior partner at BCG and chairman of the BCG Henderson Institute. Magdalena Krupa is a lead data scientist at BCG X and an ambassador to the BCG Henderson institute. Adam Job is a director at the BCG Henderson Institute.