A group of Kohl’s shareholders has had enough of the retailer’s yearslong middling performance.

A quartet of activist investors—displeased with Kohl’s declining operating profit and stagnant business in the past decade—said it had nominated a slate of nine directors on Monday, a majority of its 12-person board. That sets the stage for a potentially brutal proxy fight at Kohl’s annual shareholder meeting in May.

The group, made up of Macellum Advisors, Ancora Holdings, Legion Partners Asset Management, and 4010 Capital, collectively holds 9.5% of Kohl’s shares. The firms say that too few of Kohl’s directors have true retail experience and that too many have been around for too long. (Five of Kohl’s 12 directors have been on the board for more than five years.)

Other shareholders seemed to agree with the group’s displeasure: Kohl’s shares rose 9% on Monday morning on news of a shake-up. Kohl’s stock is down 16% from when Michelle Gass became CEO in 2018, though they have quadrupled in value since its nadir at the start of the pandemic.

The activists are also considering, among other things, whether to cut executive pay and sell some real estate that is not essential to Kohl’s day-to-day operations. In their letter, they took exception to aspects of Kohl’s business, such as how much it spends on advertising as well as its e-commerce strategy.

It is easy to see why the activists are being taken seriously: Beyond their large stake, Legion, Macellum, and Ancora previously teamed up to remake the board at Bed Bath & Beyond and install a new CEO.

The slate of board nominees includes Macellum chief executive Jonathan Duskin, former Burlington Stores CEO Thomas Kingsbury, and former Denny’s chief marketing officer Margaret Jenkins.

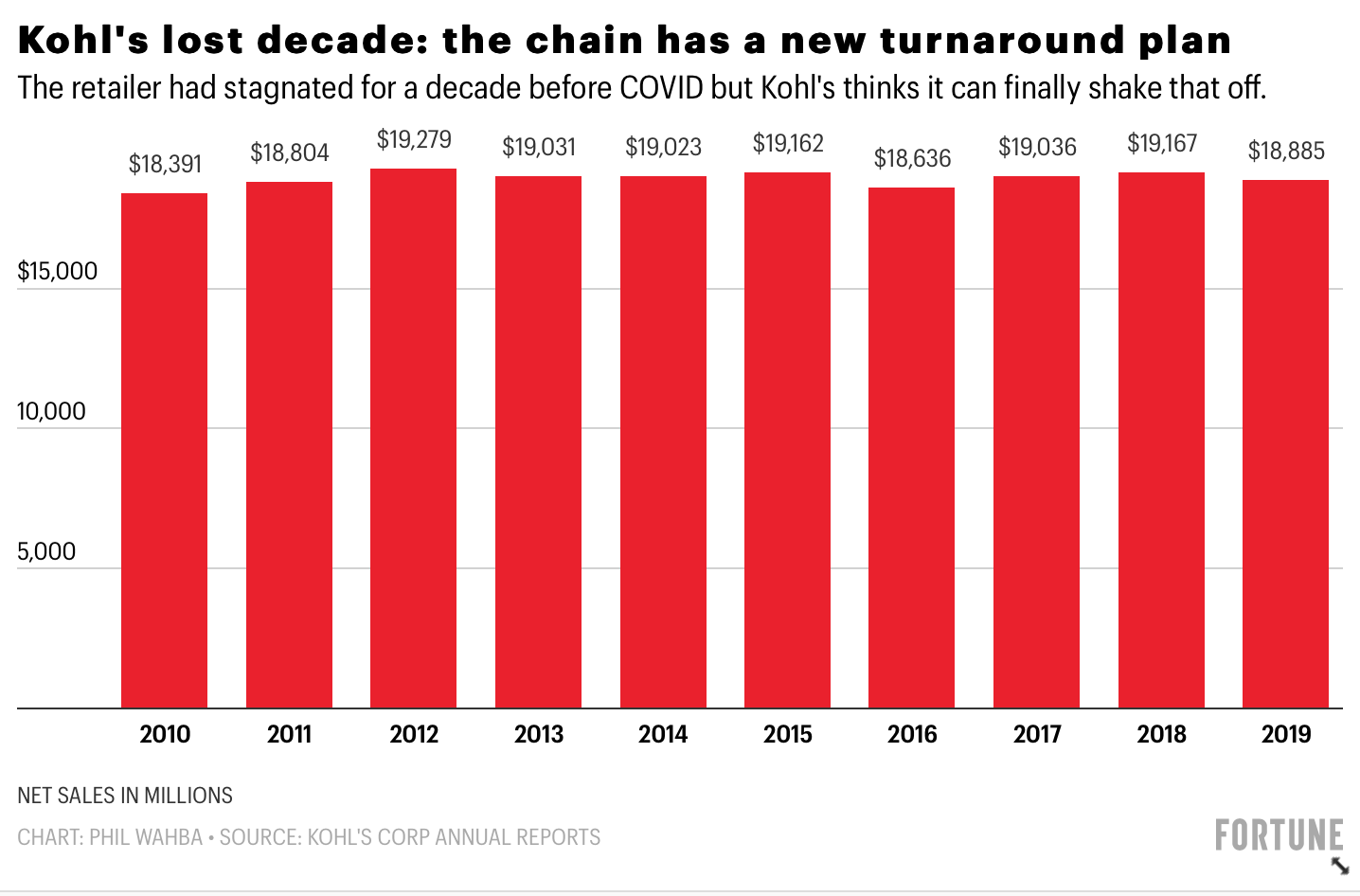

At the top of their list of complaints is a net sales level that remained virtually unchanged between 2011 and 2019 despite a number of turnaround attempts, including one announced in October, and an operating profit margin that fell by nearly half during that time, despite Kohl’s ostensibly taking market share from weakened mall-based rivals like J.C. Penney and Macy’s.

“These persistent failures have been led by several different senior executive teams but overseen by substantially the same Board,” the group said in a letter dated Feb. 22 to fellow shareholders.

Kohl’s said it had been in discussions with the group in December. “Kohl’s is deeply committed to enhancing shareholder value and is confident the Company’s new strategic framework, published in October 2020, will accelerate growth and profitability,” a spokesperson said in an emailed statement. Kohl’s later sent a second statement saying, “We reject the Investor Group’s attempt to seize control of our Board and disrupt our momentum, especially considering that we are well underway in implementing a strong growth strategy.”

However, the firms said they are worried that once the pandemic recedes, Kohl’s won’t be able to capitalize on the reopening, because of the purported “systemic inability of the Company to execute a plan that creates shareholder value.”

On that front, the group has a point: In the fiscal year ended in early 2020, prior to the COVID-19 outbreak, net sales were $18.9 billion, roughly where they were eight years earlier. Meanwhile, operating profits came to 6.1% from 11.5%.

Struggling with off-mall rivals

Kohl’s has fared much better than its mall-based department store rivals. Indeed the company frequently reminds investors that 95% of its stores are off-mall. But its off-mall rivals, from Ulta Beauty to Gap Inc.’s Old Navy to Dick’s Sporting Goods to Target, have handily bested Kohl’s.

Kohl’s net sales fell 25.3% in the first three quarters of the year, much of that because of store closures last spring. But while declines moderated significantly by the time the holiday season came around, falling 10%, that contrasts sharply with those off-mall retailers.

Kohl’s unveiled a new turnaround strategy in October predicated on building upon its recent success in activewear, further phasing out weak store brands, and finally becoming a sizable player in beauty. The company also promised to get its operating profit margins back up in the 7% to 8% range. (It will provide an update on that effort next week when it reports fourth-quarter financial results.)

A previous turnaround strategy in 2014, called the Greatness Agenda, which was also based on a bigger beauty business and refreshed store brands, failed to change Kohl’s overall sales trajectory.

Still, under Gass, who has been Kohl’s CEO since 2018, the retailer has made big moves that likely averted big sales declines. After joining Kohl’s in 2013, she was the architect of Kohl’s big push into activewear, notably bringing in Under Armour: The category now represents 20% of sales, and Gass has said that could hit 30%.

Kohl’s has finally pared stale brands like Dana Buchman and Rock & Republic, but struggled to create new ones with the same touch and agility as Target has. Instead, Kohl’s has focused on bringing in more national brands that its rivals don’t carry, such as Lands’ End, Cole Haan, and Toms.

And in a daring move, Kohl’s has teamed up with Amazon to handle returns in its stores for the e-commerce giant, betting that the extra shopper traffic would lift sales. The company doesn’t give out much information on that front, so it’s hard to know whether the partnership has panned out.

More recently, Gass landed a coup by winning a shop-in-shop partnership with LVMH’s Sephora away from Penney, instantly and finally making Kohl’s a major player in the beauty wars. The challenge of course will be to see if Kohl’s manages to get Sephora customers to shop in the rest of its stores too, something they did not do much at Penney. (Kohl’s will be going up against the upcoming Ulta Beauty shops within Target stores.)

For all its problems, Kohl’s has plenty going for it. While many competitors are withering, the retailer boasts a loyal clientele along with a ton of stores dotting the country that offer well-known brands. But, ultimately, it also struggles to offer customers things they cannot find elsewhere or online.

What’s more, as Target’s holiday results as well as those of Walmart have shown, customers are consolidating shopping trips during the pandemic, opting to get everything from clothes to groceries to sports gear under the same roof.

It’s anybody’s guess if they will continue to do so after COVID-19 recedes. But Kohl’s will have to make a very compelling case to get them to break these new habits.

Never miss a story: Follow your favorite topics and authors to get a personalized email with the journalism that matters most to you.