This article is part of Fortune‘s quarterly investment guide for Q4 2020.

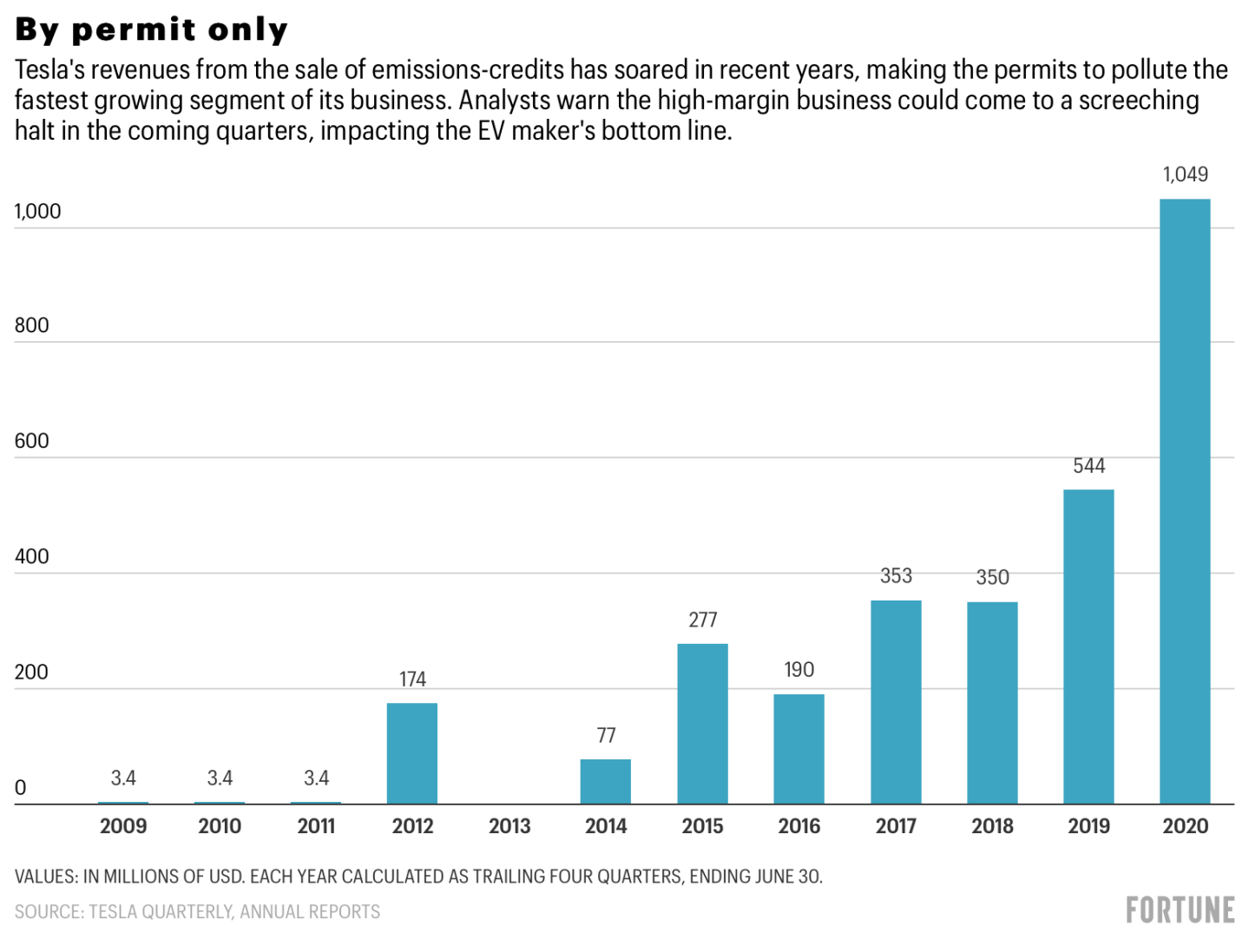

For years it has been a little-talked about secret hiding in plain sight: Tesla doesn’t make much of its money selling cars. Instead, the company has shrewdly capitalized on mastering a complex market for selling global emissions credits. As Fortune previously examined in detail, Tesla’s credit sales started off small, averaging $3.4 million per year through 2011, and rising to $1.049 billion through the last four quarters ended June 30, 2020.

To sum it up, Tesla amasses tradable credits from four main sources. The first category is zero-emission vehicle (ZEV) programs run by the states, notably California. It also benefits from two U.S. federal standards, the greenhouse gas (GHG) emissions regulations imposed by the Environmental Protection Agency, and corporate average fuel economy (CAFE) rules established by the National Highway Traffic Safety Administration. The fourth is the European Union’s CO2 emissions targets.

CAFE was born during the oil crisis of 1978 and sets annual average miles per gallon standards that a manufacturer must meet for its entire fleet. GHG arose from a 2007 Supreme Court decision that designated CO2 as a pollutant, and hence gave the EPA authority to regulate vehicles. GHG establishes a limit for the amount of CO2 per vehicle a manufacturer’s fleet can emit before triggering penalties. Both programs, which closely coordinate their regulations, required that automakers start complying in 2012. That same year, they also began awarding ZEV-like credits to manufacturers that exceeded the benchmarks.

Under both programs, Tesla earns maximum credits for every car it produces, since its vehicles neither consume gasoline nor spew CO2. In fact, the credits it receives rise smoothly with production. Its customers’ need for credits rises in parallel as they make more noncompliant trucks and SUVs. Since Tesla’s credits and its customers’ deficits run in tandem, Tesla trades its CAFE and GHG credits on long-term contracts that produce more consistent, though in the past smaller, revenue than the inflow from lumpy ZEV sales.

Under President Obama, the CAFE and GHG rules got a lot stricter, mandating 5% annual increases in fuel economy and a like decline in grams of CO2. But the Trump administration rolled back the requirements to yearly improvements of just 1.5%. If it remains in effect, that downshift means that most carmakers posting shortfalls won’t need to increase their purchases of credits in the future, and may buy fewer of them.

“This is totally different from California, which is like a different country,” says Ben Leard, an environmental economist and an assistant professor at the University of Tennessee. “The Obama rules were putting a lot of pressure on carmakers to buy more credits.” That pressure is expected to ease in the years ahead, given the rollback in standards. As a result, he predicts that the price of credits, and possibly the volumes sold, will decrease in 2021 and the years ahead.

If the current rules hold, Tesla is likely to see its CAFE and GHG revenues fall going forward. The decline should should be gradual, in contrast to ZEV, which should see a spike followed by a steep slide starting in a couple of years.

But a new administration could flip that script. If President Biden were to restore the aggressive targets, it would be a huge boost CAFE and GHG sales. In his “Plan for Climate Change and Environmental Justice,” Biden cites his pride in raising the CAFE mileage requirements during the Obama administration, implying that he’d push to revive or even tighten those standards as President. To do so, he’d need a buy-in from the auto companies that initially agreed to the Obama rules before convincing Trump to roll them back. If he doesn’t get carmakers to agree, he’d likely need to resort to legislation. And toughening the GHG rules requires amending the Clean Air Act. So if Biden wins the presidency in a blue sweep, keeps the House majority and wins the Senate, automakers will probably be forced to buy a lot more of Tesla’s credits to skirt big fines. That’s only a short-term benefit, however. The stricter regime will also force the manufacturers to accelerate their move to electric cars.

Meanwhile in Europe, the glory days of selling carbon credits may already be numbered. There, Tesla’s biggest buyer of credits has been FCA, maker of Jeep, Fiat, Maserati, and Alfa Romeo. But FCA plans to launch a number of hybrids, plug-ins, and EVs from 2020 to 2022, including new versions of the Jeep Renegade SUV, as well as the new all-electric version of the Fiat 500. FCA’s leaders have stated publicly that they expect the automaker to be compliant with the new rules on its own by 2022, implying that it will no longer need Tesla. At the end of 2019, FCA agreed to merge with the much greener Peugeot, a deal expected to close next year. That union could bring FCA in line still earlier.

But even an environmentalist in the White House will only buy Tesla some time, rather than preserve its current flood of profits. CAFE and GHG revenues will eventually succumb to the blow of increased competition: Starting around 2023 an influx of new EVs from manufacturers like Ford will bring their fleets closer to full compliance, reducing their purchases of Tesla credits relative to the past.

After that, it appears Tesla will have to reach profitability the old-fashioned way: by selling cars.

Explore Fortune’s Q4 investment guide:

- The biggest economic threat facing the next administration

- These 6 economic charts tell the story of Trump’s presidency

- What Wall Street’s favorite election indicators say about who will win the White House in 2020

- 10 stocks to buy now: These names should perform well no matter who wins the White House

- ESG investing is bigger than ever. Here’s how you can save the world, and your portfolio

- This year’s ‘October surprise’ could impact your portfolio for years to come

- The next President will hold a lot of sway over Tesla’s biggest profit center

- Q&A: Former Commerce Secretary Penny Pritzker talks America’s R&D problem, taxes, and the country’s economic outlook