Tesla’s fastest-growing business isn’t putting owners in its Model S and Model 3. It’s selling environmental credits that enable its SUV- and truckmaking rivals to avoid big emissions fines.

That sumptuous stream of earnings—accounting for all of Tesla’s operating profits in the first half of 2020, by Fortune’s estimate—has probably peaked, and will begin a long slide before pretty much vanishing in a few years.

The big looming shrink in pollution permits raises questions about the sustainability of the EV-maker’s bottom line. And it comes as Tesla bulls puzzle over why the firm got the big fat snub last month by the S&P 500. In any case, with the permit revenue line shrinking, the pace of Tesla car sales must offset the difference. The visionary who’s pledging to launch the Plaid, which bolts from zero to 60 in two seconds, needs to deliver a parallel feat of acceleration in making and selling Teslas.

It’s hardly surprising that Elon Musk didn’t mention the boost from regulatory credits at his annual Battery Day on Sept. 23. As usual, Musk made elaborate promises that, besides the Plaid announcement, encompassed offering $25,000 Teslas in three years and getting to that bargain price point by manufacturing in-house a new generation of “tabless” battery cells that per kilowatt-hour cost half of today’s version. But Musk did address the issue of Tesla’s slender earnings, acknowledging, “It’s not like Tesla’s profitability is crazy high. Our average profitability for the last four quarters is maybe 1%. It’s not like we’re minting money.”

By implication, Musk is including the over $1 billion in revenues from regulatory credits over that period, most of it pure profit, in asserting that Tesla is making money, though not a lot. But excluding that source, Tesla is actually taking losses on its core business of selling cars, batteries, and services that are probably a couple of points higher than the 1% Musk cites for profits. To assess the challenges Tesla faces in generating the huge earnings required to fund its epic plans for growth, it’s essential to understand how regulatory credits grew from a trickle into a substantial and growing contributor, then soared to multiples of their old heights in 2020, and why they’re destined to decline going forward.

From California to the EU

Tesla amasses tradable credits from four main sources. The first category is zero-emission vehicle (ZEV) programs run by the states, notably California. It also benefits from two U.S. federal standards, the greenhouse gas (GHG) emissions regulations imposed by the Environmental Protection Agency, and corporate average fuel economy (CAFE) rules established by the National Highway Traffic Safety Administration. The fourth is the European Union’s CO2 emissions targets.

All four regimes impose penalties on carmakers that lag in the proportion of their fleet that’s electric (ZEV), or in carbon emissions (EU and GHG), or miles-per-gallon (CAFE) benchmarks. In all cases, they bestow credits on manufacturers that exceed the standards. The players that earn those surpluses can trade their credits for cash to slow-to-go-green, over-the-limit manufacturers that need them to offset their deficits and achieve compliance. As a maker of only all-electric vehicles, Tesla accumulates loads of credits and sells more of them than any other carmaker. It’s good business to be so green. Customers from Honda to GM to Fiat Chrysler (FCA), among many others, have purchased Tesla credits. That’s enabled its permit customers to sidestep heavy fines while delaying introduction of low-margin EVs, and packing their fleets with lucrative, gas-guzzling SUVs, trucks, and vans.

The credits Tesla garners from the four regimes have changed dramatically in recent years and are set to shift again. Until recently, ZEV provided by far the biggest share of regulatory revenue. Then this year, a ramp-up in EU standards likely made Europe the top market, sending Tesla’s total take to fresh records. But as we’ll see, Europe’s contribution will fade after Tesla’s main customer, FCA, merges with Peugeot’s Groupe PSA, a maker of much cleaner cars. At the same time, the Trump administration reduced requirements for GHG and CAFE, making it easier for automakers to hit the mark and hence limiting the credits they’ll need from Tesla. (Unless, of course, a Biden administration restores or strengthens the much tougher Obama administration limits.) Meanwhile, the states are tightening, while the Feds ease, by stiffening the ZEV standards.

The future trajectory of Tesla’s regulatory revenue, now soaring, depends on two factors: first, the changing rules in the four jurisdictions and second, how fast the world’s automakers move to EVs, since the more all-electrics, hybrids, and plug-ins they produce, the fewer credits they’ll need to buy from Tesla.

In the U.S., the more lax CAFE and GHG rules probably mean that revenue from those sources will fall as U.S. regulators effectively will have removed the “stick” impelling U.S. carmakers to make more EVs in the coming years. By contrast, the tighter ZEV standards should lift Tesla’s credit sales in states like California. In Europe, the new CO2 regs are a big boon to Tesla right now. But they’re so stringent that European producers are rushing to make big portions of their fleets electric rather than pay billions in fines. That trend suggests that Tesla’s windfall will be short-lived.

Here’s the big picture: Tesla’s revenue from regulatory credits should fall in 2021—mainly owing to a reduction in Europe. It will keep declining from there, for a basic reason. The U.S. is moving much more slowly to EVs than Europe. But U.S. manufacturers have announced plans for electric and hybrid versions of many of their bestsellers over the next couple of years. So by 2023 at the latest, or around the time that $25,000 Tesla is scheduled to hit the streets, Tesla’s EV revenue should be heading downward, and the electric revolution in the years that follow will kill Tesla’s bounty from credits in the U.S.

Put simply, the profits that now put Tesla in the black in recent quarters will disappear just as the very industrywide transformation Musk pioneered gains speed. “Making these credit sales a big business has been a good strategy for Tesla, as a springboard to build its electric-car franchise,” says Matthias Schmidt, an independent auto analyst in Berlin. “But the biggest source will go away as the European market goes electric, and that’s happening fast. Tesla isn’t talking about it, but that will put tremendous pressure on them to sell a lot more cars, a lot faster than is happening now.”

Given that credits have proved so important to Tesla’s fortunes, let’s examine how those revenues have progressed over time, how the shifting rules governing the four major regimes are changing the outlook, and what its profits picture looks like without the big subsidy from its competitors that’s headed for extinction.

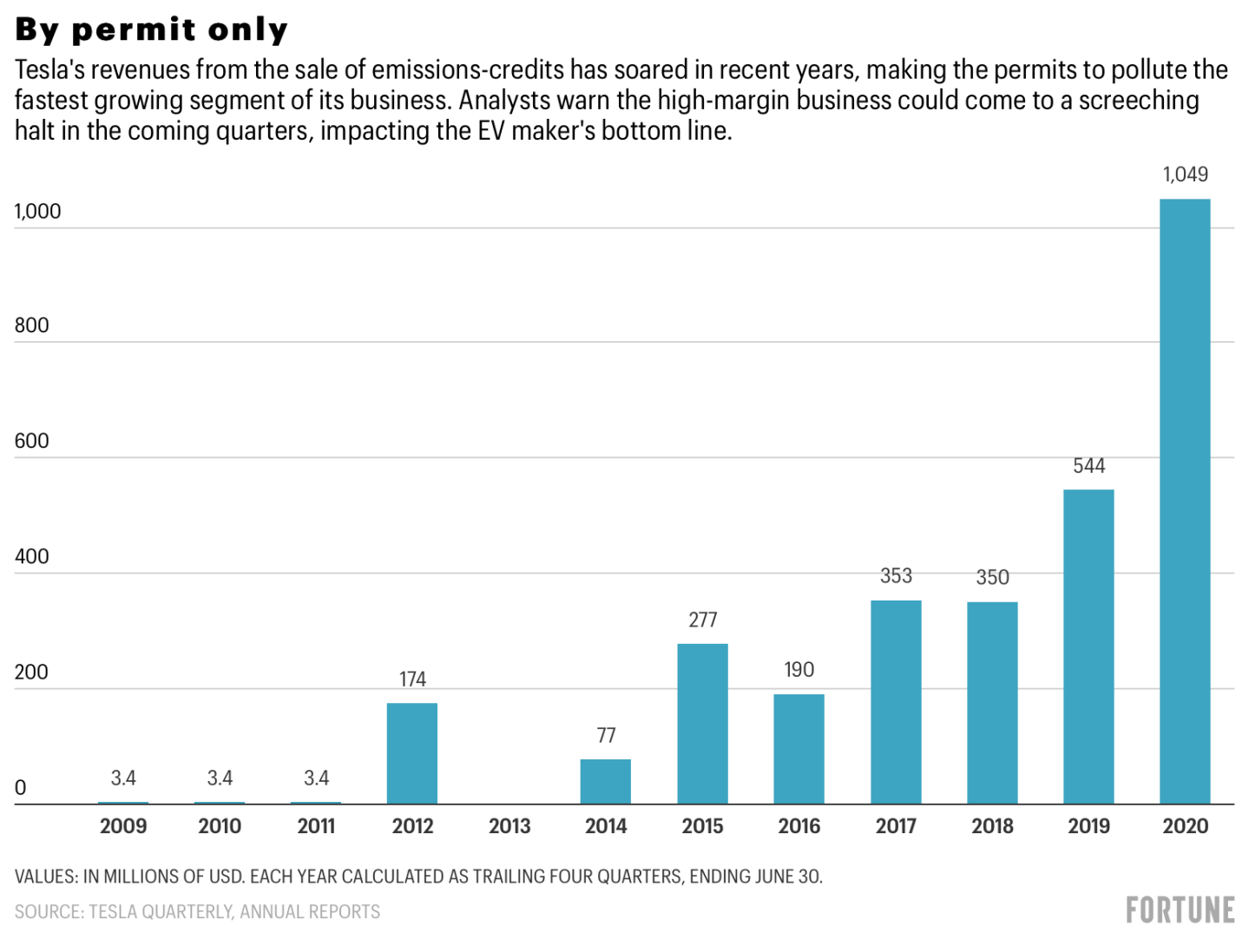

After contributing heavily for years, credit sales exploded in 2020

Tesla’s credit sales started off small, averaging $3.4 million per year through 2011, and rising to $1.049 billion through the last four quarters ended June 30, 2020.

Over the past three years, regulatory credits have been Tesla’s fastest-growing franchise, beating autos, energy generation and storage, and services. As we’ll see in the final section, credits are also the biggest factor in taking Tesla over that period from negative to moderately positive operating income.

Until at least 2019, it appears that almost all of Tesla’s sales of regulatory credits came from the U.S., flowing from the states’ ZEV programs, and the NHTSA’s CAFE and EPA’s GHG regimes. The biggest contributor was ZEV: From mid-2012 to mid-2019, ZEV credits accounted for $991 million, or 60% of the $1.66 billion in credits revenue, while GHG and CAFE furnished the balance of $668 million.

The ZEV regulations started in California in 1990 and over the years have expanded to 11 other states that adopt its requirements, including New York, New Jersey, Arizona, and Colorado. The ZEV penalties and credits are based on the share of electric vehicles in a manufacturer’s fleet. For credits, the top weights are reserved for all-electric cars, with lesser awards for hybrids and plug-ins. Manufacturers that generate surpluses can either trade their credits to rivals that don’t comply or bank them. For example, Toyota in the past has held on to credits until they expired, possibly to avoid aiding competitors.

The credits are traded privately, and the market is highly illiquid. They’re awarded once a year, and prices fluctuate widely depending on the volumes of credits made available by the “winners,” and how many the “deficit crowd” needs, which in turn depends on how their new model SUVs or trucks are faring in the ZEV states.

Remarkably, the Golden State’s eco-friendly drivers bought 77,000 Teslas last year, one in five of the vehicles it sold worldwide. So the EV maker has long collected fistfuls of credits and found lots of needy buyers, Honda among them. In its filings, Tesla has disclosed that it sells ZEV credits mainly in one-time transactions, often in big deals, and not on steady, long-term contracts. As a result, ZEV revenues arrive in clumps of $50 million or even $100 million in some quarters, and fall to zero in others. Even year to year, the numbers swing widely. For example, ZEV revenue totaled $279 million from mid-2016 to mid-2017, then dropped almost two-thirds to $103 million over the next four quarters. In Q2 of 2019, Tesla stopped breaking out ZEV versus GHG and CAFE sales, and now provides only a total for all revenue from environmental credits.

Led by California, states are stiffening the standards—and that’s welcome news for Tesla. For the 2020 model year, the weighted average for California is 9.5% of a manufacturer’s fleet must be electric; the higher the number over that threshold, the bigger the fine, or the more credits that must be purchased to comply. Credits work the same way: All electric vehicles exceeding 9.5% of a carmaker’s fleet in California earn the maximum. From this year’s bogey, the benchmark rises 2.5% a year, reaching 22% in 2030. “Tesla is getting credits on every car they sell in the ZEV states each year over the floor, since all of its cars are fully electric,” says Ben Leard, an environmental economist and an assistant professor at the University of Tennessee. So in California this year, Tesla is winning tradable permits on over 90% of the vehicles it delivers in the state.

Leard predicts that Tesla’s ZEV revenues, on average, will rise in the short term. “That’s because there aren’t a large number of electric versions of the bestselling models coming on the market for around three years,” he says. “So manufacturers will need those credits.” He adds that as the requirements rise, less of Tesla’s fleet each year will earn credits, but that higher permit prices will more than compensate, since automakers will need to buy a lot more as the floor for compliance keeps rising.

Still, he adds that starting around 2023, U.S. consumers will see a flood of electric cars. “That will be a game changer,” he notes. He cites that Ford plans to launch an all-electric version of its F-150 pickup, the bestselling vehicle in America, in 2022 or 2023. “When that happens, it will do a lot for Ford’s compliance, as will EV introductions by other automakers. They’ll no longer need to buy credits from Tesla.” He sees ZEV credit sales dwindling to much lower numbers by the start of 2024.

For Tesla, the credits that will probably stay high for longest are the ZEVs. And even those have only a few more years to run.

Tesla’s European adventure may not last long

The huge jump in Tesla’s credit sales—to over $1 billion in the past four quarters—appears to be coming mainly from Europe, and specifically, a new deal with FCA, maker of Jeep, Fiat, Maserati, and Alfa Romeo. For the 2020 model year, the EU lowered the ceiling on CO2 emissions on 95% of carmakers’ fleets from an average of 130 grams to 95 grams per kilometer. The rule goes to 100% starting in 2021. From there, the requirement will get another 15% tighter in 2025, and then at least 37.5% more so in 2030. Since the norm for most manufacturers is now around 120 grams, they’ve long been in compliance. The major exception was FCA. Despite the tougher rules, most of its competitors have developed technology that will bring them into compliance this year. FCA simply fell further behind.

Tesla is a big generator of tradable credits in Europe, since its CO2 emissions average per car is zero. The EU gave Tesla an extra boost by establishing “super-credits” that count electric cars as two vehicles in 2020, effectively doubling its awards. The EU allows players with surplus credits to “pool” with another producer whose average stands above 95 grams. The point of pooling is to lower the average across the entire, combined fleet to below the requirement, so that the partner in need becomes compliant and avoids paying stiff fines for exceeding the limits.

In January, Tesla joined a pool formed by industry laggard FCA, which has among the highest emissions per vehicle in the EU. Neither company has disclosed what FCA is paying Tesla for adding the EVs that, when combined with FCA’s Jeeps and Fiat SUVs, brings the average into the safe green zone. In its second-quarter report, FCA disclosed payments for regulatory credits of roughly $350 million for the first half of 2020, more than double the number from 2019—a large portion reportedly going to Tesla.

But Europe may not be Tesla’s cash cow for long. FCA plans to launch a number of hybrids, plug-ins, and EVs from 2020 to 2022, including new versions of the Jeep Renegade SUV, as well as the new, all-electric version of the Fiat 500. FCA’s leaders have stated publicly that they expect the automaker to be compliant with the new rules on its own by 2022, implying that it will no longer need Tesla. At the end of 2019, FCA agreed to merge with Peugeot, a deal expected to close next year. That union could bring FCA in line even earlier. “Peugeot set the standard by purchasing GM’s Opel, which produced among the highest emissions of any high-volume brand in Europe, and quickly bringing its cars into compliance,” says Schmidt. He expects that Peugeot will shift FCA’s higher-polluting models to its far more efficient drivetrains that greatly lower emissions, just as it did for Opel.

So it’s unlikely a FCA-Tesla pool will last beyond the close of 2021 and could end earlier. Of course, Tesla could join another pool. But Schmidt predicts that because the new rules are so tough—as opposed to the lax federal regs in the U.S.—European producers will go electric at such a rapid pace that they’ll virtually all be in compliance by the end of 2022. “Tesla will lose its sales from the FCA pool, and almost all credit sales should disappear over the next two years,” says Schmidt.

But he adds an important proviso. If Europe’s momentum to produce clean cars fades, the big jump in standards in 2025 could restore the market for Tesla’s credits.

Excluding regulatory credits, Tesla is losing money

In the second quarter of 2020, Tesla posted $1.137 billion in “gross profits” in its auto business, representing revenues of $5.179 billion less costs of materials and labor. Of that almost $5.2 billion in sales, $428 million flowed from regulatory credits. Those reg revenues, however, are mostly profit, so their margins are much higher than what Tesla makes on selling cars (if anything). It’s impossible to say precisely how much goes straight into earnings, because Tesla doesn’t disclose overhead expenses by business, and selling credits obviously involves personnel costs. But even assuming that the activity absorbs a proportion of selling, general, and administrative expenses equal to its share of total revenues, credits would still contribute over $400 million in pretax profits. Take out that number, and Tesla’s total net income from autos, batteries, and services drops from a puny $104 million to minus $300 million, or almost 5% of all-in sales.

Tesla’s been shrewd in exploiting a system in which rivals help fund its rise. Those subsidies will soon end as its benefactors start making more and more of their own EVs. Musk claims that Tesla will grow so fast and so profitably that the loss of credit sales will barely be noticed. But the credits brought hard cash, and, so far, the vision of fabulous performance is just a promise.

Additional reporting by Bernhard Warner

More must-read finance coverage from Fortune:

- BlackRock’s Larry Fink to CEOs: Get serious on net-zero targets, or else

- Elon Musk says he “kinda” loves Etsy. Should you buy the stock?

- When will Biden’s $1,400 stimulus check pass? Here’s everything to know

- China’s society is going cashless. Now its central bank is pushing back

- Revolut disrupted banking in Europe—can it do the same in the U.S.?

- Why Mark Zuckerberg’s venture firm just invested millions in a Finnish food delivery startup