Additional reporting by Jen Wieczner.

THE LAWSUIT resonated throughout the worlds of tech, finance, and corporate law, halting one of the largest acquisitions of 2020 dead in its tracks. On Nov. 5 of last year, 10 months after payments conglomerate Visa agreed to a $5.3 billion deal to acquire financial data startup Plaid, the Department of Justice filed an antitrust complaint seeking to block the merger.

In its filing, the Justice Department claimed the deal was a cynical attempt by Visa—which it described as “a monopolist in online debit transactions”—to stifle competition and “eliminate a nascent competitive threat.” Corporate documents procured by the DOJ during its discovery process were unflattering to say the least; they depicted a dominant incumbent intimidated by what Plaid’s technological capabilities could mean for core segments of its business and keen on heading off the startup before such disruption could take place.

Since its founding in 2013 by a pair of twentysomething Bain & Co. alumni, Plaid has emerged at the forefront of the technological revolution in financial services. Through its development of application programming interfaces, or APIs, that allow financial apps to link directly with consumers’ bank accounts, the company has established itself as the preferred infrastructure through which edgy fintech startups in the U.S. have been able to grow and prosper—in the process radically digitizing how Americans conduct their financial lives. Venmo, Robinhood, Acorns, and Betterment are among the more than 5,000 financial services providers that rely on Plaid’s infrastructure to connect with no fewer than 200 million bank accounts across roughly 11,000 U.S. financial institutions.

“They are a huge part of the infrastructure of all of fintech,” says Andrei Cherny, cofounder and CEO of Aspiration, a branchless, digital “neo-bank” that has been a customer of Plaid’s since its own founding in 2014. “The entire ecosystem of companies that have come along over the last five years, and begun to reshape the way people use and think about their money, has been enabled by Plaid.”

Plaid is fundamentally a business-to-business enterprise with virtually no consumer-facing presence. It has often been described as the “plumbing” through which other fintech enterprises are able to operate, whether it’s allowing consumers to transfer funds, invest their money, or apply for a mortgage. Yet the Justice Department claimed Plaid had other ideas in the works that posed a threat to Visa: namely, plans to leverage its technology to create a new “pay-by-bank” platform that would allow merchants to directly transact with customers’ bank accounts. Such a platform would bypass payment systems, or “rails,” like Visa’s sprawling network, with the potential to “save merchants and consumers hundreds of millions of dollars per year in debit fees,” according to the complaint—threatening an online debit market in which Visa held a roughly 70% market share in the U.S. and generated around $2 billion in earnings in 2019.

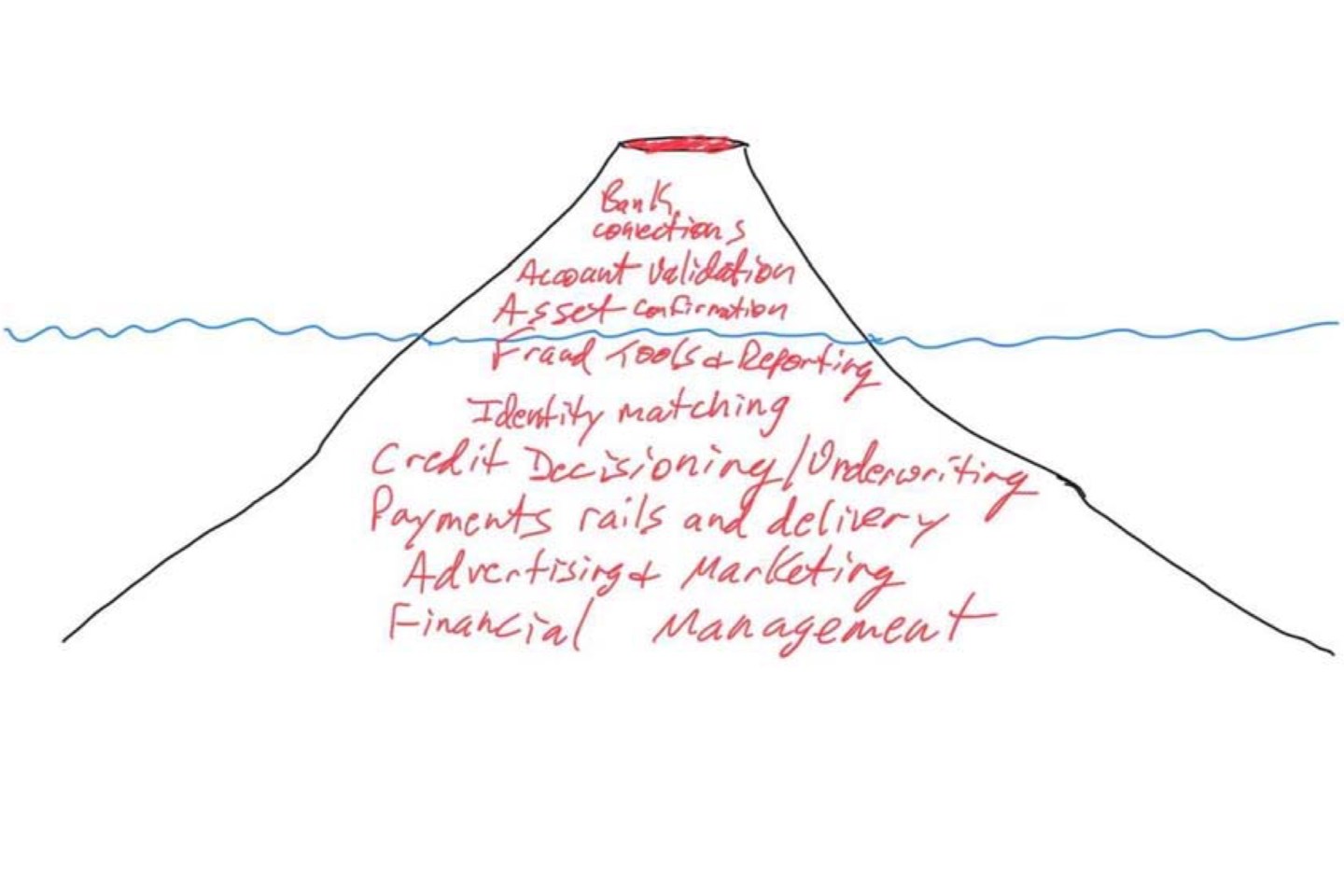

Antitrust prosecutors viewed Visa’s bid to acquire Plaid as an attempt to undercut that threat, and to back their assertion, they had a damning trove of documents detailing deliberations inside both companies. One piece of evidence quickly made the rounds on the Internet among tech circles: a sketch by a Visa executive that analogized Plaid to an island volcano—one whose current capabilities were only “the tip showing above the water,” while what lay beneath the surface represented what the executive called “a massive opportunity—one that threatens Visa.”

In another internal exchange documented by the DOJ, Visa CEO Al Kelly, after catching wind of Plaid’s plans to launch money movement capabilities, observed that the startup was “clearly, on their own or owned by a competitor, going to create some threat to our U.S. debit business.” An acquisition of Plaid, he added, would be an “insurance policy” against that threat—with Kelly acknowledging that the $5-billion-plus purchase of a startup with revenues that the DOJ pegged at less than $100 million in 2019 “does not hunt on financial grounds.” (Visa, No. 131 on this year’s Fortune 500, brought in nearly $22 billion in revenue in the fiscal year that ended in September 2020.)

As the Justice Department compiled its case over the course of 2020, other factors conspired to further complicate matters. The coronavirus pandemic prompted an unforeseen acceleration in fintech services, as consumers wary of leaving their homes turned to digital means of managing their finances. Plaid saw its customer base increase by 60% in 2020, according to the company—growth spurred as much by legacy banks and financial firms seeking to keep up with the times as by plucky, disruptive startups.

“We’ve hit an inflection point in digital finance,” Plaid cofounder and CEO Zach Perret tells Fortune. “Every bank has taken their five-year strategy on digitizing and brought it down into one or two years.”

Indeed, the DOJ’s investigation and intervention had dragged out the proposed acquisition through a pandemic that had seen Plaid’s business boom—making the $5.3 billion purchase price suddenly look like a bargain for Visa. Coupled with the specter of drawn-out antitrust litigation, the transaction suddenly made a lot less sense to those inside the startup.

On Jan. 12, two months after the DOJ filed its lawsuit and a day shy of the one-year anniversary of the merger announcement, Visa and Plaid released a joint statement announcing that they had agreed to terminate the deal. It soon became evident which side had the most to gain from calling things off: In April, Plaid announced a $425 million Series D funding round that valued the company at roughly $13.4 billion, or more than 2.5 times Visa’s purchase price.

Today, Perret says that Plaid “wouldn’t have entered into the deal” had it known of the antitrust scrutiny that lay in waiting. What’s more, he adds, the pandemic’s accelerating influence on digital finance had meant that “a lot had changed; our company was fundamentally a different company, and it was a fundamentally different market that we were in.”

Fortune spoke with more than two dozen sources across the realms of financial services and antitrust regulation to examine the factors behind the brief dalliance between Visa and Plaid and its ultimate demise. It is a story about the unprecedented, tech-fueled disruption currently remaking a multitrillion-dollar industry; how fledgling upstarts turned unicorns are aiming to upend the status quo, and how established incumbents are coping with the challenge. It is also about how government regulators are scrambling to keep up with changing paradigms that will impact hundreds of millions of consumers, while also straddling a thin line between ensuring fair competition and stifling the machinations of a free, entrepreneurial market.

“I think we’re at this tectonic shift in financial services that is kind of like what happened to offline retail with Amazon 15 years ago,” according to Mark Goldberg, a partner at Silicon Valley venture capital firm and Plaid investor Index Ventures. “We’re at the very beginning of this generational transformation, in a zero-sum way, from the old guard to the new guard.”

Like many Plaid investors who followed the company’s changing fortunes over the past year, Goldberg was pleased to see the Visa deal fall through, tweeting at the time: “The opportunity here is $50-billion-plus, not $5 billion.” But now he believes he may have been selling Plaid short.

“I think I got it wrong—I think it’s a $100 billion opportunity,” he says.

TO UNDERSTAND the impact that Plaid, as well as similar financial data firms, are now having on financial services, one must go back 11 years to Congress’s passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act. In enacting a wave of post–Great Recession regulations, an unassuming provision in Section 1033 of the bill had the effect of ushering in a new “open banking” paradigm.

With a couple hundred words, Section 1033 essentially mandated that U.S. consumers own the rights to their financial information and have the right to share that information as they see fit. What was previously a walled-off world of financial data—with banks serving as the gatekeepers—had now been opened up, allowing third-party entities to tap into consumers’ bank accounts and provide new, innovative, and lower-cost services to an unprecedented extent.

“I’m not sure that when Congress wrote Section 1033, they knew how powerful of a tool they were creating,” says Plaid head of policy John Pitts. “Fundamentally, it transforms something that didn’t belong to the consumer into something that does, and which the consumer can use to make their financial life better.”

As an example, Pitts cites the arrival of stock trading apps like Robinhood, an early Plaid customer whose digitally enabled, no-commission-fee model forced established brokerages to lower their costs in order to compete. “In 2008, if I want to invest, I’m paying a commission on every single [stock] trade I make. In 2021, I don’t pay a commission on any investment I make at all,” he notes. “So even if you’re a Charles Schwab or Fidelity customer, you are saving money right now because of fintech, and because of this consumer data access right that’s at the core of it.”

As the first wave of fintech apps began to capitalize on the new regulatory guidelines in the early 2010s, Plaid’s cofounders, Zach Perret and William Hockey, were among the would-be entrepreneurs who sought to make their mark. The pair met during a brief stint as associates at consulting giant Bain’s Atlanta office. Both had similar small-town backgrounds; Perret grew up in North Carolina before majoring in the hard sciences at Duke, while Hockey was raised on a farm in central California and earned his degree in computer science at Emory University. But they soon found themselves restless in the world of consulting and with a shared desire to build something new themselves.

“We liked building things, and we both had this passion for engineering and technology,” Hockey recalls. In Hockey, Perret says he found a “kindred spirit” who was also “enamored by how technology can have a huge impact on the world,” and with the computer science chops to match. “He’s a much better engineer than I ever was,” Perret notes.

Before long, the pair had left Bain and headed for New York City, where they quickly fell into the lives of young startup founders—couch-surfing, credit card debt, and borrowed office space. “Pretty much wherever there was free stuff, we would go,” Hockey says. He slept on one friend’s couch for nearly a year, while Perret took the gamble of moving in with his now-fiancée after only four months together.

Initially, the two tried their hand at the sort of consumer financial app that was in vogue at the time, with personal finance startup Mint.com cited as an early reference point. They even won a TechCrunch hackathon with Rambler, a web app that accessed Foursquare’s APIs to map credit and debit card transactions. But before long, Perret and Hockey realized that the underlying API technology that they had developed—and its ability to provide a smoother integration with consumers’ bank accounts than existing methods—had far greater value than any consumer app they could hope to build on top of it.

“There were a lot of people building consumer financial services, but from an engineering perspective, it was really hard,” Hockey recounts. “The moment you had to do anything that involved the financial institution, it was like you were back in the 1980s. And as we met more people and understood the financial services landscape, we realized this was actually a pretty big problem.”

Perret and Hockey had happened upon the revelation that would drive Plaid’s business model: an if-you-build-it, they-will-come approach to financial data that would enable a fledgling fintech ecosystem to flourish, by making it easier for fintech developers to access the banking system. “I always told our crews early on that our mission is, ‘How do you convince a college kid—instead of making Instagram for cats or whatever—to make a fintech app?’” Hockey says. “And you do that by making it really easy; you do that by making all the complexity go away.”

After moving its base to San Francisco in 2013, Plaid quickly found ample demand for its API platform from fintech startups. Acorns, Robinhood, and Venmo were among early customers who were drawn to the company’s streamlined developer experience. (Plaid makes money by charging its fintech customers for every API “call,” or connection linking a consumer’s bank account data to that fintech firm’s services.) Plaid was far from the first firm to offer a means of accessing consumers’ banking data; one rival financial data aggregator, Envestnet-owned Yodlee, has been active in the space for over two decades. But Plaid’s technology offered an alternative to more cumbersome, less secure “screen-scraping” methods—which require consumers to share sensitive bank log-in credentials with third parties, and allow those parties to effectively “scrape” and extract consumers’ data as they see fit.

“That was the problem with fintech at the time; when it came to connecting with bank account data and things like that, it was clunky, difficult, and hacky,” says Matt Hamilton, vice president of product at digital business banking startup Novo. As one of Venmo’s earliest employees from its pre-PayPal days, Hamilton witnessed firsthand how Plaid changed the game from the way things were previously done, allowing companies like the now-pervasive money transfer service to grow in efficiency and scale. “The thing Plaid brought to a lot of these fintechs was a truly integrated, seamless user experience.”

Despite gaining traction early, Plaid still had a hard time initially convincing investors that the company and its relatively obscure technology were worth betting on. Hockey describes the period from 2012 to 2016 as a “constant existential crisis” for the company: “We almost died like 10 times.”

But as the fintech revolution gained steam in the mid-to-late-2010s and Plaid’s user base grew, investors came around to the potential at hand. In 2018, Plaid officially attained unicorn status with a $250 million Series C funding round that valued the firm at $2.65 billion; the round lured new investors like venture behemoths Kleiner Perkins and Andreessen Horowitz, as well as both Visa and Mastercard. (Hockey, who had served as Plaid’s president and chief technology officer, stepped down from those roles in the wake of that round, though he remains on the company’s board.)

“There’s been a love-hate relationship [between Plaid and banks]. Plaid was saying, ‘We’re building an experience that you should be building, but you’re not doing it.’”

Matt Hamilton, Vice President of product, novo

Along with its developer-friendly ethos, Plaid has also presented itself as a consumer-conscious enterprise committed to improving the financial lives of ordinary people through the services it enables. Perret describes consumers as the “true north” at the heart of Plaid’s mission. Pitts, who joined Plaid in 2018 after six years as an official at the Consumer Financial Protection Bureau, recalls going into his final job interview with Perret having made up his mind to remain in the public sector. When Perret asked him how he would feel if Plaid started selling its data to hedge funds for profit, Pitts figured he would tell the CEO how he really felt: “Well, I would tell you all the reasons why that’s a bad idea, I would be really vocal in saying we shouldn’t do it, and if you decided to do it anyway, I would leave because I don’t think that’s something I could be a part of.”

To his surprise, Perret responded enthusiastically in agreement. “Zach said, ‘I don’t think we need to talk much further—I think you’ll be a great fit for the team,’” according to Pitts. “And by the end of that 30-minute interview, I had gone from, ‘I can’t leave government’ to ‘I have to leave because I have to come here.’”

INITIALLY, BANKS and financial institutions greeted the open banking revolution with considerable skepticism, if not downright hostility. Having long held a privileged position in which they had control over how their customers’ banking data was leveraged, they have found themselves at the eye of a storm of innovation surrounding their industry.

Venmo alum Hamilton recalls that it wasn’t uncommon in Plaid’s early days for some banks to “get mad at them and shut off their access” to customer accounts—though he added that as Plaid has grown, it has “shored up” its relationships with financial institutions, having sold them on the value and reliability of its platform. “There’s been a love-hate relationship there,” he notes. “Plaid was saying, ‘We’re building an experience that you should be building, but you’re not doing it.’”

Today, in contrast, many major banks work directly with Plaid to launch their own fintech offerings. Goldman Sachs’s Marcus consumer banking division is one notable client that uses Plaid’s APIs to power its own services, while Plaid and U.S. Bank recently announced a partnership to provide the bank’s customers with “an API-based, credential-less open finance experience.”

It is an adapt-or-die approach that JPMorgan Chase CEO Jamie Dimon summed up in his most recent annual shareholder letter, when he noted that banks “are facing extensive competition from Silicon Valley, both in the form of fintechs and Big Tech companies…that is here to stay.” (Plaid has also benefited as major tech players have made their own moves into financial services, with Google and Microsoft both becoming customers last year.)

“Financial services is one of the last industries to really be disrupted by technology,” says Chime cofounder and CEO Chris Britt, whose mobile banking platform is a Plaid customer. “The banks, for the most part, are balance sheet companies first that happen to have tech, whereas a lot of these [fintech] companies are technology companies first that happen to be involved in financial services.”

In the payments realm, the competition is no less fierce. Silicon Valley giants like Apple, Google, and PayPal have now established themselves as key players in cardless payments, while startups like Stripe have become formidable in their own right, paving the way for a flurry of upstarts looking for skin in the game. Mere months after raising $300 million at a $2.3 billion valuation, business-focused payments firm Rapyd is now reportedly eyeing a new funding round that would more than double that valuation to $5 billion.

But when it comes to actually operating the payment rails that allow consumers and businesses to transact globally, Visa continues to maintain a competitive advantage that has allowed it to stay one step ahead. Coupled with its longtime rival Mastercard, Visa finds itself as one half of a “duopoly,” as one analyst describes it, that continues to dominate debit and credit payments. Globally, Visa’s and Mastercard’s debit and credit networks processed a combined $10.2 trillion and $7.5 trillion in transactions, respectively, in 2020.

“They’ve created a centralized infrastructure that connects billions of consumers and millions of merchants and thousands of card-issuing banks, and that infrastructure is tough to displace because it is ingrained in so many economies around the world,” according to Bank of America senior equity research analyst Jason Kupferberg. “It makes sense for some of these fintechs to essentially innovate on top of that infrastructure, rather than try to replace it.”

That is exactly what virtually all major payments-focused fintech firms today find themselves having to do. Mobile wallet services like Apple Pay deploy Visa’s rails to enable its contactless payments, while Visa has made inroads to partner with cryptocurrency players including Coinbase (which recently launched a debit card on Visa’s network) and money transfer startups like Wise. The company has also been aggressive in developing internal product offerings like Visa Direct, an accounts-to-accounts payments service, akin to settlement networks like the Clearing House, that has real-time cross-border capabilities and processed 3.5 billion transactions last year.

Visa’s efforts in the realm of tech-enabled payments have meant that “rather than [fintech] being a disruptive influence, it actually creates more distribution points” for the company’s network, according to Kupferberg.

That sentiment is echoed by Visa president Ryan McInerney, who tells Fortune that the company views the technological evolution of financial services as “tremendously positive” development for its own business.

“Early on, we decided that we were absolutely going to lean into this and open up our network,” McInerney says. He notes that Visa’s San Francisco home base has allowed it to develop relationships early with many fintech startups, including as an investor (as evidenced by its participation in Plaid’s Series C round). “We want every fintech out there to build on our platform, and so far we’ve been relatively successful.”

McInerney says that the Plaid acquisition was motivated by a desire “to expand our network,” with Visa seeing a “natural synergy” with Plaid’s business and an opportunity to diversify its infrastructure capabilities. “It was just a natural way for us to expand our connectivity with U.S. fintechs, and would only have enhanced Visa’s role as a partner to fintech developers.”

For Plaid, the benefits of the merger were clear: the backing of a major Fortune 500 corporation with the kind of global reach that would allow it to scale its own business—not to mention a healthy windfall for the company’s principals and investors. And though Visa would have acquired Plaid outright, the agreement called for the startup to maintain considerable operational autonomy, keeping its own offices and functioning as an independent business unit within Visa.

Currently, Plaid is active in the U.S., Canada, the U.K., and four European countries. But as fintech capabilities continue to proliferate globally and more countries begin to adapt their own regulatory frameworks around open banking, Plaid was counting on Visa’s expansive reach to help it navigate the weeds in foreign markets. “That concept of internationalization and breadth was incredibly inspiring and intriguing to us,” Perret says.

“The biggest benefit to me was the global scale of Visa, as I thought: ‘Oh, my God, what is it going to take me to build relationships with 60 governments over the next two years? That sounds like a lot of work,’” Pitts adds. “I will say, though—now that the acquisition isn’t happening, I’m pretty damn excited to do all that myself.”

DESPITE THE EVIDENCE outlined in the Justice Department’s bombshell complaint, Plaid insists it has little in the way of plans to build a payments network that could compete with the likes of Visa. Outside observers harbor their own doubts over whether the startup would have the ability or desire to establish such a platform, given the extensive back-end capabilities required. “At the end of the day, Plaid doesn’t have any connectivity to merchants,” notes BofA’s Kupferberg.

Even in its own existing market, Plaid is facing increased competition from rivals seeking to stake a claim in the ever-expanding realm of fintech infrastructure. One such rival, Utah-based MX, has gunned for market share by working more closely with banks—collaborating with them to develop what MX founder and CEO Ryan Caldwell calls “bank-endorsed APIs.”

“We actually have superstrong relationships with the banks. We work with them to help create those connections, so they’re superfast and you know the data is reliable,” Caldwell tells Fortune. Caldwell notes that MX shares many of the same customers as Plaid since fintech firms often rely on multiple data providers. “It’s not an API built without the bank’s permission; it’s built with their knowledge and participation.” In January, MX closed a $300 million funding round that quadrupled the company’s valuation to $1.9 billion.

Perret acknowledges that Plaid has “really big ambitions” to diversify its business by leveraging “the level of data analytics that we have to bear.” He says it is examining a product that could predict potential fraud on fund transfers to third-party apps, as well as efforts that would leverage consumers’ financial data to enhance their credit profiles, making it easier for them to access loans and other products. (The company has also launched what it calls the Plaid Portal, an online platform with the domain my.plaid.com that allows people to control and manage the financial data that they share with various fintech services.) Still, he notes that Plaid’s “thesis is very different than Visa’s”; rather than providing financial services itself, and competing with others that do so, he claims Plaid is “trying to build a network that focuses on enabling consumers to do financial services really well.”

Antitrust regulators, however, took an entirely different view of Plaid’s potential and Visa’s intentions in acquiring the company. Given the documents uncovered, the Justice Department saw fit to launch the sort of lawsuit that critics argue have been too few and far between in recent years—one blocking the acquisition of a “nascent” competitor by a dominant incumbent. In this respect, the specter of Big Tech looms large, as federal regulators have drawn scrutiny for permitting Silicon Valley behemoths like Facebook and Google to swallow up smaller enterprises that could have eventually posed a challenge to their market share.

“If you don’t have antitrust enforcement, the only exit for new innovators is going to be the incumbents, whereby you sell to the incumbents and get out of the way. It’s important we make sure the marketplace allows disruption to occur.”

Makan Delrahim, former head of the department of justice’s antitrust division

“The focus for a long time in antitrust generally has been prohibiting only the grossest limitations on what we would call horizontal competition—when one firm acquires another that’s selling exactly the same product to the same people,” according to Christopher Sagers, a professor of law at Cleveland State University’s Cleveland-Marshall College of Law. In challenging the Visa-Plaid transaction, Sagers believes regulators have come around to the realization that “in markets with a lot of technological disruption, a deal doesn’t have to be horizontal today to be horizontal in the near future.”

For the Justice Department, the inquiry into the Visa-Plaid deal came in lockstep with a heightened focus on fintech and financial services at large. Under the guidance of Makan Delrahim, the then–assistant attorney general of the antitrust division, the DOJ formed a consolidated unit focused on oversight of the financial sector, with an emphasis on fintech.

“Because of fintech disruption, it was important that we pay more attention to the financial services industry at all levels,” Delrahim tells Fortune. Another transaction heavily scrutinized by Delrahim’s division was financial software firm Intuit’s $8.1 billion acquisition of Credit Karma. The DOJ eventually allowed that deal to proceed, but not before forcing Credit Karma to divest its tax preparation business because of concerns that Intuit, which owns TurboTax, was cornering the market on tax-filing software.

As far as the Visa-Plaid deal was concerned, Visa likely found itself a victim of its ubiquitous success. Six months after Visa announced the Plaid acquisition, Mastercard unveiled its own deal to buy Finicity, a Plaid competitor in the financial data space, for roughly $1 billion. But the DOJ allowed the Mastercard-Finicity transaction to proceed unchallenged, with Mastercard’s more limited market share in its core businesses widely acknowledged as a key factor. While Visa and Mastercard accounted more than $5.9 trillion in purchase volume across debit, credit, and prepaid cards issued in the U.S. last year, Visa alone accounted for more than 70% of that figure, according to data from the Nilson Report.

Visa is also currently facing an antitrust investigation into allegedly anticompetitive practices in the debit card market, and whether it has flouted Dodd-Frank regulations designed to give merchants greater choice in the debit card routing networks they are able to use.

The sum effect of regulators’ scrutiny of Visa has been a sentiment, espoused by multiple legal and financial industry sources, that the DOJ’s antitrust division has taken a deliberately hostile approach to the company and its business model. “The division does not like Visa,” one corporate antitrust attorney opines.

Inside both Visa and Plaid, the feeling was that the Justice Department’s discovery process had given the companies a raw deal. Though the documents procured—the volcano sketch, the disclosure of boardroom deliberations—were damning, there was a sense that the DOJ had front-loaded its case in the complaint, and that it would have struggled to produce additional evidence at trial depicting a deliberately anticompetitive effort by Visa.

In any case, Visa and Plaid now found themselves on the verge of a drawn-out court battle—one that likely would have dragged on through 2021, if not longer—in order to consummate their merger. “I think a turning point for us was seeing how long it was going to take,” Plaid general counsel Meredith Fuchs tells Fortune. Fuchs notes that the DOJ’s “single-minded focus” on blocking the transaction—as opposed to working out a settlement—was another deterring factor. “It wasn’t like there was another route [for the Justice Department] other than the merger ending.”

With Plaid “looking down the barrel of another 18 months of uncertainty,” according to Perret, the transaction no longer made sense for his rapidly growing startup—though both Plaid and Visa insist the decision to call off their agreement was a mutual one.

In the wake of the deal’s collapse, one prevailing line of thought is that government efforts to more stringently regulate such acquisitions could have the effect of hurting startups more than the purchasing incumbents—depriving them of an exit ramp through which founders, as well as investors, can capitalize on innovations.

But for the regulators, those concerns are outweighed by the benefits of ensuring that the largest companies aren’t allowed to swallow smaller ones unencumbered, to the detriment of the wider market. “If you don’t have antitrust enforcement, basically the only exit for new innovators is going to be the incumbents, whereby you sell to the incumbents and get out of the way,” Delrahim says. “Innovators are the disruptive entrants that bring dynamic competition to the marketplace, and it’s important we make sure the marketplace allows disruption to occur.”

THE PUBLIC MARKETS now appear to be Plaid’s destiny—though perhaps not anytime very soon.

“I think this company could be public today if it wanted to be,” according to Rick Yang of venture capital firm New Enterprise Associates, who sits on Plaid’s board as one of the company’s earliest investors. Though noting that Plaid’s latest funding round, which featured the likes of Altimeter Capital and Silver Lake Partners as new investors, had the makeup of a pre-IPO round, Yang adds that the company will take its time to “make sure we’re prepared for the public markets.” Sources inside Plaid say that the company’s brain trust is not currently deliberating over an IPO, which likely means it won’t be tapping the public markets before late 2022, at the earliest.

The feeling within Plaid is that the company has been reinvigorated, now that the clouds of uncertainty around the Visa deal have dissipated. With a team of more than 800 people and counting across two continents, Plaid is now able to push ahead and grow its business on its own terms—with its reestablished status as an independent enterprise having allowed the company to recapture “that startup vibe,” as Index Ventures’ Mark Goldberg describes it.

“I think the company, for the past 12 months, kind of went into this period of not being as aggressive as we wanted to be, just because we were focused on the transaction stuff,” Yang notes. The next 12 months, he says, should bring “a very steady cadence of super interesting product launches” that should expand Plaid’s market reach. A pay-by-bank platform like that mooted by the DOJ, company sources insist, will not be one of them.

And though 2020 was as challenging of a year as any, it proved to those inside Plaid that their company’s mission of improving peoples’ financial lives could deliver at a time when they were most in need. Pitts says his proudest moment in his time at Plaid was the frantic week, during the height of the pandemic-induced lockdown in the spring of 2020, in which the company custom-built a product enabling small businesses to access their payroll information—allowing them to more easily apply for relief loans through the Paycheck Protection Program.

“Plaid in seven days developed a product that fintech lenders could use to help get those loans out the door faster,” Pitts recalls. “That to me was like, ‘Oh, my God, we aren’t tangential. We’ve answered the question of whether fintech is real financial services—it is.”

For his part, Perret believes financial services has barely scratched the surface of the digital revolution to come. The financial system is “still significantly analog,” he notes. “A huge proportion of mortgages in the U.S. still get issued by walking into a bank branch with a shoebox full of paper, and handing it to someone who then types it into a system.”

“People ask us frequently, ‘Who’s your biggest competitor?’ And my honest answer is that it’s paper,” Perret adds. “We’re digitizing the industry—we’re getting rid of that shoebox full of paper, and we’re putting it on the Internet.” In that context, “digital finance is just at the tip of the iceberg.”

Or, rather, the tip of the volcano.

Subscribe to Fortune Daily to get essential business stories straight to your inbox each morning.