Paying your loans can be stressful for many reasons, but a top source of anguish is dealing with the people at the other end of those loans—typically, a faceless bureaucracy that likes to send form letters and put you on hold over the simplest of questions.

Sameh Elamawy, the founder of a San Francisco startup called Scratch, thinks he can help. Elamawy has assembled a team of Amazon and Pinterest veterans to recast the loan servicing business as a friendly, easy-to-use app.

Scratch, which has raised $17 million from Index Ventures and other investors, could prove to be disruptive because the current model of loan servicing is both inefficient and analog. That model relies on call centers and heaps of paperwork for even simple tasks like changing the monthly payment date of a loan.

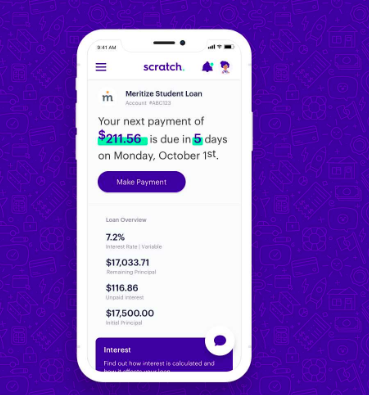

The Scratch model relies on APIs that pull data from lenders in order to show a person’s payment obligations in an app that looks like this:

The app, which also provides a clear overview of interest and borrowing terms, could help some users get a better idea of their financial options.

Currently, Scratch services student loans and personal loans, though it plans to expand to mortgages and other types of debt in the future. Borrowers do not sign up for the service directly but instead receive an email from Scratch inviting them to participate.

Elamawy, who used to be a product manager at Pinterest, says the idea for Scratch came in part from talking to an Uber driver who felt overwhelmed from keeping track of her debt payments.

He also believes the current model of loan servicing—in which companies charge lenders to collect and distribute payments— can create perverse incentives. Elamawy points out that established loan servicers (who include some of the same people who brought us the 2009 mortgage crisis) typically charge extra fees to lenders when a borrower falls behind, meaning they have little reason to help the borrower pay on time.

Elamawy says Scratch’s tech-intense approach means it spend much less on record-keeping, and can direct its resources to building a more empathetic experience for borrowers. While this doesn’t result in lower payments for the borrowers (since loan servicers don’t hold the debt), it does lower service fees for the lenders—savings that could, in theory, be passed on.

Scratch, which has been around since 2015 and already has millions of users, is just one example of how Silicon Valley is trying to reinvent the loan industry. A group of startups, including Prodigal and True Accord, want to make debt collection more high tech and less abrasive. And the likes of SoFi seek to impart a supportive, community-feel dimension to the student loan business.

Elamawy, who was recently named as an advisor to the Consumer Financial Protection Bureau, believes his company can be part of this push to make paying loans a less hostile experience.

“For scale we already have billions of dollars in loans flowing through our platform. Now that doesn’t yet make a dent in the 13 trillion of household debt out there, but we are excited to be growing by the day,” he said.

Scratch’s other investors include Ribbit Capital, Founders Fund, Nyca Partners and the Center for Financial Services Innovation.

An earlier version of this story, based on information from Scratch, listed JPMorgan Chase as an investor. Scratch has since clarified JPMorgan Chase is not an investor.