It’s a tense time to be a staffer at Goldman Sachs.

The bank’s infamously tough yearly performance reviews are looming. CEO David Solomon has publicly mused about the size of the storied firm’s staffing “footprint.” The huge reorganization that Solomon unveiled earlier this fall will be implemented later this month. And Solomon is still fighting to force employees back to their desks. Speaking at a Goldman financial services conference on Dec. 6, Solomon said the U.S. could face a recession in 2023 and that job cuts shouldn’t be a surprise. “Naturally compensation will be lower…We will pay people based on the overall performance of the firm,” Solomon said.

Where Goldman makes its money

Since Solomon took over as CEO in 2018, Goldman has sought to move beyond trading and investment banking (where revenues are very volatile), and into staid, but more predictable, consumer credit and wealth management, echoing consumer-facing moves rivals Morgan Stanley, JPMorgan Chase, and Bank of America have all made. The latest reorg, announced in October, solidifies that strategy.

And though its stock has outperformed rivals, Goldman hopes the latest moves will strengthen its position even further. The headline is that the firm plans to combine asset and wealth management into one segment and will put investment banking and global markets, including trading, into a second segment. A third unit, called Platform Solutions, will consolidate fintech platforms from across the firm including transaction banking, consumer partnerships (mainly credit cards with Apple and General Motors), and specialty lender GreenSky, according to Matt O’Connor, a Deutsche Bank analyst, in a research note. The reorganization is the biggest shakeup for Goldman since 2020 when the firm laid out plans for four core units—investment banking, global markets, consumer and wealth management, and asset management.

Goldman has always been a wealth manager but has traditionally focused on high-net-worth individuals, said Andrew Besheer, director of the wealth management practice at Boston consultancy, Aite-Novarica. With Marcus, Goldman had tried to move downstream, like many in the industry, and focus on the mass affluent consumer but is now reining in those plans, Besheer told Fortune. Goldman’s plan is to “move Marcus into supporting existing customers as opposed to growing it via a mass-market audience,” he said. He doesn’t expect Goldman to try to compete for the E*Trade demographic. “We are committed to our deposits business, our consumer partnerships, and GreenSky, all of which remain a focus for Goldman Sachs,” a spokesman said.

But as any Goldman tea leaf reader knows, strategic shuffles mean major winners and losers inside the company’s ranks. Fortune spoke to several current and former Goldman insiders to paint a picture of how the org chart has evolved of late. Here’s who is up, who has moved sideways, and who is out.

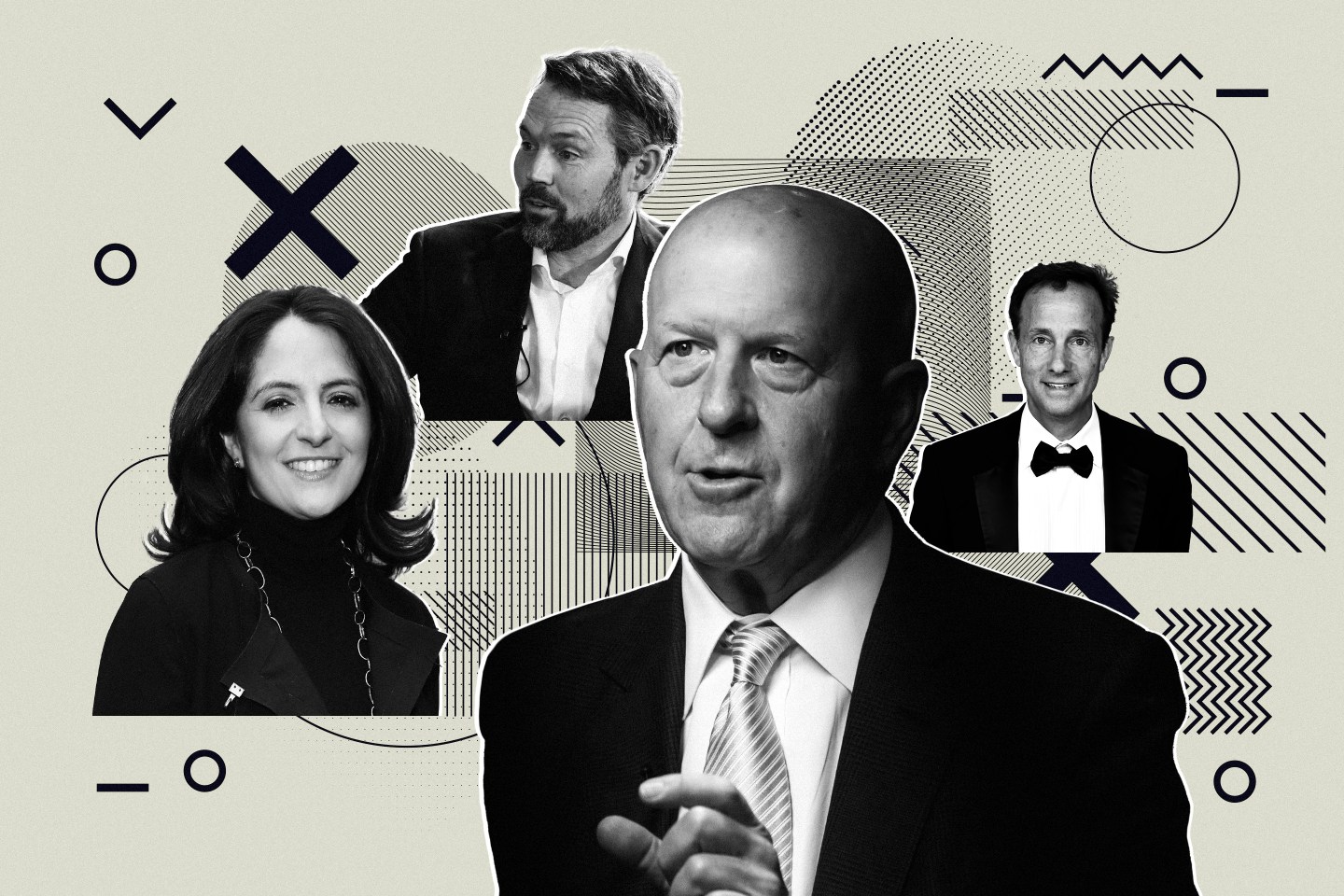

Power players inside Goldman Sachs

The biggest winner? Marc Nachmann, who will run the $2.4 trillion asset and wealth management unit. Nachmann, who was cohead of global markets (which includes trading), is considered a fixer and a cost-cutter. Trading revenue at Goldman hit $20 billion so far this year, up from $15 billion in 2019 when Nachmann took over, a spokeswoman said. He previously co-led investment banking from 2017 to 2019 and before that, from 2014 to 2017, was cohead of financing and head of Latin America.

The reorg also signals the dominance of investment banking and trading, which aren’t really impacted by the changes. Dan Dees and James Esposito, the coheads of investment banking, will lead the banking and trading operations, along with Ashok Varadhan, the prolific trader who made partner at Goldman before he hit 30 and was cohead of the global markets division. In the third quarter, investment banking and global markets generated the majority, 65%, of Goldman’s revenue, compared with consumer and wealth management, which produced just 20%. (Investment banking revenue, however, dropped 57% in the third quarter but was offset by global markets revenue, which rose 11%.) Before the deal market slowed this year, Goldman remained a powerhouse in M&A, advising on many of the biggest deals. This includes Microsoft’s $69 billion acquisition of game studio Activision Blizzard, Elon Musk’s $44 billion buy of social media site Twitter, and cloud computing company VMware’s $61 billion sale to Broadcom.

One metric to note here that’s getting a revamp: how Goldman reports profits. Goldman traditionally reports separate ROE (return on equity) figures for its global markets and investment banking units. Now that it’s combining the two, it will provide one number for the group when it reports earnings in January. This will better align it with rivals Morgan Stanley and JPMorgan, which typically offer one ROE. “We’ve been outperforming on a return on equity basis and haven’t gotten the credit we deserve,” one Goldman executive said.

Shifting roles

The reorganization spells big changes for Stephanie Cohen. During the last Goldman reorg, announced in September 2020 and put into effect the following January, the firm named Cohen, along with Tucker York, to cohead its consumer and wealth management business. With the current shuffle, Cohen will become head of Platform Solutions.

Some pegged the move as a lateral one for Cohen, while others pointed out that the executive remains the head of a major unit. It does cement her status as one of Goldman’s most powerful women. Cohen, former chief strategy officer at GS, is passionate about Goldman’s move to providing banking as a service (BaaS), which refers to companies offering banking services to clients through APIs, people familiar with the transition said. Platform Solutions is the logical place for BaaS, and Cohen is its best leader, they said. “Stephanie is fantastic and one of the people who really gets it,” a different person, no longer at Goldman, who had worked closely with her, said.

There’s also Peeyush Nahar, who joined Goldman a little over a year ago as a partner and was head of the consumer business, which includes Marcus. Nahar was previously VP of technology at Uber and a 14-year vet of Amazon. With the reorg, he will be co–chief operating officer of Platform Solutions with Hari Moorthy, who was head of transaction banking. Nahar is considered more of a tech exec, and while he has worked at consumer businesses like Uber, he isn’t a consumer banker, people said.

With the reorganization, Goldman is also recombining its asset and wealth management business, which it had split up in 2020. York, who was cohead of the consumer and wealth management business with Cohen, will resume his prior role as head of wealth management. This unit includes private wealth management, which works with ultra–high-net-worth executives with more than $10 million in assets; personal financial management, which focuses on high-net-worth individuals with $1 million to $10 million; and Ayco, which offers financial planning for corporate partners. This is considered a lateral move for York.

The corporate shuffle will also see Julian Salisbury and Luke Sarsfield no longer serving as coheads of the asset management business. Salisbury will become the unit’s chief investment officer, which Goldman classified as a very substantive role. He will report to John Waldron, president and chief operating officer (the No. 2 executive at Goldman). “Our clients see his role as critically important,” a Goldman spokeswoman said.

Still, the asset management business lagged this year thanks in part to runaway inflation and poor market performance overall. GS asset management revenue in the third quarter dropped 20% to $1.82 billion compared with the same time period in 2021, comprising just 15% of Goldman’s revenue. The unit also had a notable defection last year. In 2020, Eric Lane and Salisbury were named coheads of asset management, but Lane, who had spent nearly 27 years at Goldman and was considered a potential successor to Solomon, left in March 2021 to join Tiger Global Management. In January 2022, Goldman tapped Sarsfield, who was cohead of the client business for asset management, to replace Lane as cohead of asset management. After less than a year in that role, Sarsfield will now serve as its chief commercial officer. “We’re looking to Luke to create the growth strategy for one of the largest active asset managers in the world—and expand our success in alternatives, customized SMA [separately managed account] portfolios, and other areas where we believe we have a real competitive advantage,” the Goldman spokeswoman said.

Who’s down and who’s out

The most obvious loser in the reorg is Marcus. Of course, that’s not actually a person, it’s Goldman’s digital bank, which is getting sidelined. Goldman had launched Marcus, its direct to consumer business, in 2016. The fintech offers high-yield savings accounts and personal loans to millions of customers. Marcus is actually a mashup of several businesses. First Goldman acquired the online deposit platform of GE Capital Bank in 2016, getting $16 billion in deposits, which have since grown to $110 billion in deposits globally and remain a focus for the bank. Two years later, Goldman picked up Clarity Money, a personal finance management app, for $100 million. Goldman closed its $2.24 billion buy of GreenSky, the buy-now-pay-later fintech, in September, which is part of the broader consumer business.

In the past few years, Marcus lost momentum after most of its founding team departed Goldman, people said. One of the most significant exits was Harit Talwar, who spent more than six years at Marcus, including several as head of the unit before becoming chairman in January 2021. Talwar departed in December 2021 and is now chairman of Better, the troubled online mortgage lender.

Omer Ismail, who was one of the first employees at Marcus, replaced Talwar when he became head of the consumer bank in late 2020. Ismail, and his top lieutenant, David Stark, who was head of large partnerships, including Apple Card, left Goldman in February 2021 to join One, a mobile banking app that is backed by Walmart. Sonali Divilek, the head of product for Marcus, exited GS in July 2021 to join JPMorgan Chase. One month later, Sherry Ann Mohan, who was chief financial officer of Marcus, left for JPMorgan. Elisabeth Kozack, who held several positions at Marcus including VP of product lending and head of point-of-sale financing, also joined JPMorgan in February of this year.

Marcus has suffered from product delays; its long-expected checking account is still not available (it’s in beta); and the digital bank is said to be operating at a loss. There were always voices at Goldman that questioned whether the firm should push forward with Marcus, people said. “Those voices got stronger during this recessionary period,” the former staffer added.

The market broadly has soured on BNPL (buy now, pay later) ventures such as Klarna and Affirm, but GreenSky, which has a network of 10,000 merchants, remains a priority at Goldman, another person familiar with the situation noted.

That said, bankers and private equity executives say they expect Goldman will eventually try to sell off Marcus and GreenSky. A sale has always been an option for Marcus, while others don’t believe GreenSky fits with Goldman’s strategy, people said. Goldman has flirted with going after lower-level consumers, but they’re not very good at it, one banker noted. “Goldman’s focus is rich people and corporations,” the banker said.

At least until the next reorganization.