Negotiations were not going well in early June as Uber CEO Dara Khosrowshahi tried to wrap up his acquisition of Grubhub, a major competitor of his Uber Eats food delivery business. He and Grubhub founder Matt Maloney reportedly couldn’t agree on how to handle the inevitable antitrust scrutiny the deal would attract, the amount of a breakup fee, and who would run the combined delivery operation. Frustrated, Khosrowshahi walked away—and within hours a company most Americans had never heard of, Amsterdam-based Just Eat Takeaway.com, swooped in and signed a deal to buy Grubhub for $7.3 billion.

The move was even more audacious than it looked. Just Eat Takeaway is a money-losing startup that agreed to pay a price equal to half its market value. Nonetheless, while no one knows how the overcrowded food-delivery industry will shake out, history says the ambitious Dutch outfit may have done something very smart.

That’s because economic calamities—even tragic, once-a-century global pandemics—require business leaders to find opportunity in the chaos. It’s there to be found. Leaders who can seize it will mitigate the pain for employees, consumers, vendors, communities, and investors. The big lesson from past downturns is that the competitive order within industries will change far more now than it ever will in prosperous times. The big winners will be the bold companies that break from the mainstream, acting courageously and fast.

As economies reopen, the great challenge for business leaders in all industries is to look beyond their immediate operational issues, as critical as they are, and also think strategically about longer-term decisions they can make in this moment—positioning themselves to flourish in the good times ahead.

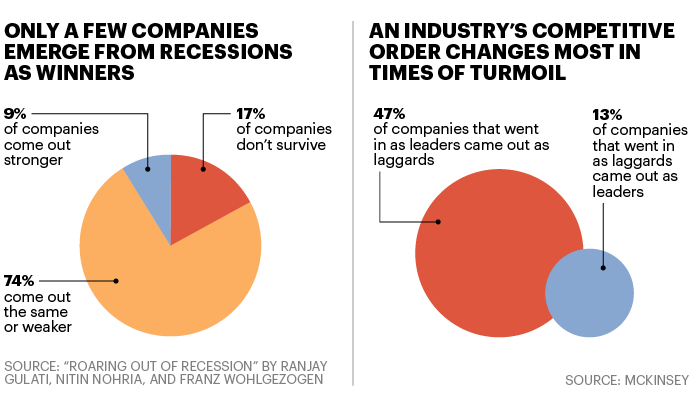

The results can be dramatic. In the technology bust of 2000 to 2002, 47% of the tech companies that went into the downturn as leaders emerged as laggards, while 13% of those that went in as laggards came out as leaders, as measured by McKinsey. That’s a radical reordering of a giant industry, and it all happened in just two years.

Every downturn is unique, and this one is especially unusual because it wasn’t sparked by economic or financial forces. A new disease combining with a digital, global economy produced truly new conditions. We’ve just had the Snapchat version of the Great Depression, with GDP plunging and unemployment spiking and then abating in a matter of weeks, producing what may have been the world’s shortest economic downturn. Now, although GDP is apparently growing again and the number of unemployed is declining, we’re experiencing the dial-up Internet version of a recovery—it will be maddeningly slow.

The upside: There’s still plenty of time to capitalize on the opportunities of this massive disruption. They’re available to anyone brave enough to follow the lessons of past downturns, unconventional though they may seem. Five principles stand out.

Don’t just cut costs—rethink them

The most timeworn maxim of tough times is “Cash is king,” and the first response to a downturn in many firms is to cut costs with a fervor and hoard cash desperately. Yet the results are surprisingly poor. In a massive study of 4,700 public companies during past recessions, researchers at the Harvard Business School found that the most energetic cost cutters “have the lowest probability—21%—of pulling ahead of the competition when times get better.”

The reasons are many. “Executives and employees start approaching every decision through a loss-minimizing lens,” the researchers found. “A siege mentality leads the organization to aim low… Pessimism permeates the organization.” More concretely, the fiercest cost cutters are most likely to miss investments that would pay off after the recession, leaving them behind the industry leaders and trying to catch up in a hotter environment where costs are higher.

By contrast, companies that come out of downturns most strongly actually increase spending on some items while cutting carefully elsewhere. Consider Apple, which was a much smaller and more troubled company going into the 2001–2002 recession than it is today. Even though revenue fell 33% in 2001, the company increased R&D spending substantially and kept it there for the next two years. Results included the iTunes music store in 2003 and other iPod innovations in 2004, helping to turn the company around and setting it on its historically successful path.

The most successful companies—industry leaders that remain leaders through recessions—are master managers of operating expenses. Compared with competitors who come out of recessions badly, they actually spend less on SG&A (selling, general, and administrative expenses) in good times but then spend significantly more on it during the downturn, according to McKinsey researchers—“the most dramatic and least expected response of the leaders to the recession,” they say. In addition, those leaders “more than doubled their already higher-than-average level of spending on R&D during the recession.”

A favorite target of cost cutters is advertising because it’s so easy to turn up or down, but the most successful companies don’t cut even that. Compared with their less successful peers, they spend less on advertising in the good times, then spend more in the recession while the competition has cut back, giving them an edge when the economy turns up. De Beers, the world’s largest diamond seller, increased marketing spending in the 2008 holiday season, at the depth of the financial crisis, rather than risk losing its place in the minds of gift givers. Researchers at Boston Consulting Group conclude, “Companies that injudiciously slash marketing spending often find that they later must spend far more than they saved in order to recover.”

To be sure, sometimes cash really is king. When lockdowns virtually close businesses like Hertz, Neiman Marcus, and Gold’s Gym, all of which have filed for bankruptcy protection, a cash obsession makes sense. Everybody else must find what the Harvard researchers call “the elusive balance” between cutting costs, usually through operational efficiency, and spending more, often on R&D and marketing. That’s what the winners do.

Don’t just accept the new normal—embrace it

Step into one of Alibaba’s Hema stores in Beijing and you’ll notice 10 or 15 small restaurants around the perimeter. It looks like a food court until you notice a fresh-foods area plus some dry grocery, “but much greater choice than a convenience store, and better brands,” says Dan O’Connor, a veteran retail consultant and a fellow at Harvard Business School’s Advanced Leadership Initiative. Look closer and you’ll see “people running all around the store with these bags,” which they fill with items and deposit on a conveyor taking them “up and across the ceiling and into a back room,” outside of which are parked 100 motorcycles. “Their brand promise is, ‘Anything here in 30 minutes if you live within three kilometers [1.8 miles] of the store.’ That gives them eight minutes to pick the order. And they’re picking 200,000 digital orders a month out of 40,000 square feet,” he marvels. “This is where we’re going.”

Many of the most successful retailers in the pandemic worldwide are those that most quickly embraced a new reality: Millions of consumers want everyday items delivered, fast, and as economies reopen, shoppers are not going back to their old ways of buying. That trend was already underway, and the pandemic powerfully accelerated it, as it has done with trends in many industries. The challenge is adapting to these trends in weeks or months rather than years.

Some of the most dramatic shifts are happening in office buildings, many of which have sat almost empty for months and are only beginning to open up. The trend that’s accelerating is what the industry calls community—creating and managing the workplace to offer a building-wide experience through events, amenities, concierge services, and related elements. “The crisis is highlighting this need for community,” says Emma Buckland, in charge of property management at CBRE, a commercial real estate services and investment firm. “We’ve been talking about differentiation through the building experience. Now that’s been taken up to a whole new place, and community will be central. Landlords will win with how they can build it.”

For example, a building’s amenities—restaurant, gym, terrace childcare center—must all be managed differently, or, in future buildings, planned differently. Landlords and tenants at the forefront are rethinking every detail. “How do you solve for coffee?” asks Karen Ellzey, CBRE’s executive managing director. “People are thinking about being able to order it remotely. A machine makes it, and maybe somebody brings it to you, or maybe in the future a robot does because it knows where you are.”

It’s a small thing that exemplifies a larger issue, what Ellzey calls “the service culture” that landlords and tenants are trying to elevate. Reaching that goal has now become more complex. Rethinking coffee is “a way to marry up the need for safety with something that feels like a higher level of service.”

Business leaders in any industry can confidently embrace the new normal because in most cases it was already on the way, just on a much slower schedule. In one of those coincidences that publishers dream about, a book called Healthy Buildings appeared in April. It argues that people are far more productive in healthier environments, based on air quality, temperature, noise, lighting, and other factors, and shows that a trend toward healthier buildings was already underway. Suddenly it’s happening much faster.

But beware: An accelerating trend can derail other trends. “Will we get a vaccine or not, and what happens with the price of oil?” asks John Macomber, a coauthor of Healthy Buildings, former chairman of a major New England construction firm, and now an instructor at the Harvard Business School. “If oil prices remain low and it’s inexpensive to drive, and COVID-19 remains a problem, there’s much more incentive to spread out—a total reversal of the trend of the last many years.”

Update your business model

No one in the hotel industry knows how quickly business will return—before reopening, revenue was down 90% in some markets—but they know one thing for sure: They won’t be making money in the same way they did pre-COVID for a long time, if ever. The problem is that most hotels operate on a business model that includes revenue from many sources in addition to rooms. Guests spend on restaurants, bars, golf, retail shops, parking, spas, meetings, conventions, and other offerings. Even when travelers eventually feel safe again checking into a room, they may balk at some of those other activities.

To make a profit on rooms only, hotels would need far higher occupancy rates. A new analysis by HotStats, a hotel industry data firm, finds that full-service hotels normally break even at 39% occupancy, but without those ancillary revenues they need 46% occupancy—a level U.S. hotels on average aren’t reaching.

It’s time for an updated business model. For example, hotels “could use their meeting facilities with groups from the community to find new revenue,” says Kate Walsh, dean of Cornell University’s famed hotel school. “Green spaces will be more valuable,” so hotels might open their golf courses to the public. As guests remain leery of gyms, “a Peloton in your room” could make sense.

Other industries are adjusting their operating models. Companies that had relied on in-person sales calls were forced to go digital during lockdowns, and an April survey by McKinsey found that 60% of those companies judged their new remote sales model at least as effective as their old model, and often more effective. Those companies won’t be going back as the economy reopens. Companies in almost every industry—food, technology, furniture, toys, pharmaceuticals, and many more—have faced disrupted supply chains. Rather than continue with business models based on lowest-cost suppliers, they’re switching to a more diversified and less risky set of suppliers.

Make strategic acquisitions

Corporate takeovers have plunged in the pandemic, with U.S. deal value down 50% from last year, says Refinitiv. Yet some business leaders are bucking the trend; they think now is a great time to be buying. “M&A is the No. 1 priority in our capital allocation strategy,” VF Corp. CEO Steve Rendle told Yahoo Finance last month. Just to make sure the world knows he’s looking, he told the Financial Times in mid-June, “In times like this, some of the greatest returns could be generated through acquiring.” VF owns apparel brands including Vans, Timberland, and Dickies, all of which were acquired.

This is how winners behave in a downturn. In a study of nearly 1,000 industrial companies, McKinsey researchers found pre-recession industry laggards that emerged from a recession as leaders made far more acquisitions than their less successful peers did, and those acquisitions were much larger. The winning companies made courageous bets, spending much more of their cash than their former peers. And, the researchers observe, the winners “seem to have pursued transactions that offered greater opportunity to shape industries.” That is exactly why canny M&A is so valuable in a downturn.

Tech companies in particular are busy making deals. Microsoft, Facebook, Zoom, and others announced 10 major acquisitions in May, and Amazon was rumored to be acquiring Zoox, a developer of autonomous driving technology. Yes, the biggest tech companies are among this downturn’s most successful businesses, so they have deep pockets. But smaller firms are active, too, and smart deals can be even more transformative for them, especially on terms that may not be available again. Just Eat Takeaway.com’s agreement with Grubhub is only one example.

Steal great people

Financial stress sometimes addles the mind, even in top-level executives. In the midst of the financial crisis, when Boston Consulting Group asked almost a thousand of them about their experience in the previous downturn, they said their third-most-effective action (out of 22) was “hiring high-performing employees of competitors.” But when asked to name the actions they planned to take in the then-current crisis, their No. 1 response was “cutting back on recruiting.” Huh?

Irrational competitors offer a rare chance to build the most valuable capital in your business, the human capital. Now is “an unprecedented opportunity to hire great talent,” says Claudio Fernández-Aráoz, a former partner in the Egon Zehnder executive search firm. “A lot of people are available,” he notes, with record layoffs at every level. The best people may not be laid off but may be reassigned or asked to move. In addition, “people are recalculating their priorities” in this massive reset, “asking, ‘What is my purpose in life?’” And even in the post-lockdown era, “candidates are more accessible than ever because they’re still working from home and can have conversations without the boss looking over their shoulder.”

Ask your company’s leaders to name specific people they’d like to have onboard, and contact them. Identify people you may not know who’ve been laid off in heavily hit industries, not just your own. When trying to close the deal with an attractive candidate, it’s often effective to bring in the CEO to express his or her passion for the business.

One more thing: Don’t forget to assess your own people and protect the stars. In boom times it’s easy to delude oneself into thinking the team is all A players. In tough times you find out who they really are. Make sure they know they’re valued. As Fernández-Aráoz says, “It’s stupid to hire great people if your great people are leaving.”

Climbing out of this economic ditch will be slow, hard work; 86% of Fortune 500 CEOs think economic activity will not return to pre-pandemic levels before the first quarter of 2022. Much of the news will be bad, and business leaders will be easily consumed by immediate, urgent problems. But as former General Electric chief Jack Welch famously said, “Anybody can manage short. Anybody can manage long. Balancing those two things is what management is.”

Keeping an eye on the long term will be hard in this environment. But that’s where wise leaders will find their greatest opportunities.