Société Générale’s chief global strategist, Albert Edwards, isn’t known for his optimism. The Wall Street veteran made a name for himself in financial papers in 1996 with a bold prediction about an “ice age” of economic stagnation and negative bond yields in the West that proved at least partially correct. And in recent years, Edwards has been the rare voice from finance legitimizing the controversial term “greedflation”—the criticism of corporations for using rising material costs during the pandemic and war in Ukraine as an “excuse” to boost their profit margins. In April 2023, his lament about the economic impact of corporate greed rang out across the Street: “We may be looking at the end of capitalism.”

While many economists argue that the rise in corporate profits during the inflationary post-pandemic lockdown period wasn’t a result of greedflation, but rather a standard part of the cyclical nature of profits during business cycles. Edwards said last June that, in his view, this time really is different. “Greedflation is a controversial topic. For me it is simple—I can find no precedent in history (including the inflationary 1970s) during which unit costs have risen sharply and yet unit profits have also risen, except in this cycle,” he wrote in a note to clients. “Things certainly are different this time.”

Now, Edwards, who has been forecasting a recession for years, is turning his attention to the hype surrounding artificial intelligence—and, as usual, he’s not convinced.

“Every bubble has a compelling narrative,” he wrote in a Thursday note. “The current narrative centers on the anticipation of an AI-driven surge in corporate profits to fully justify the current stratospheric valuations. Those of us who lived through the late 1990s [tech] bubble have heard it all before and roll our eyes skyward.”

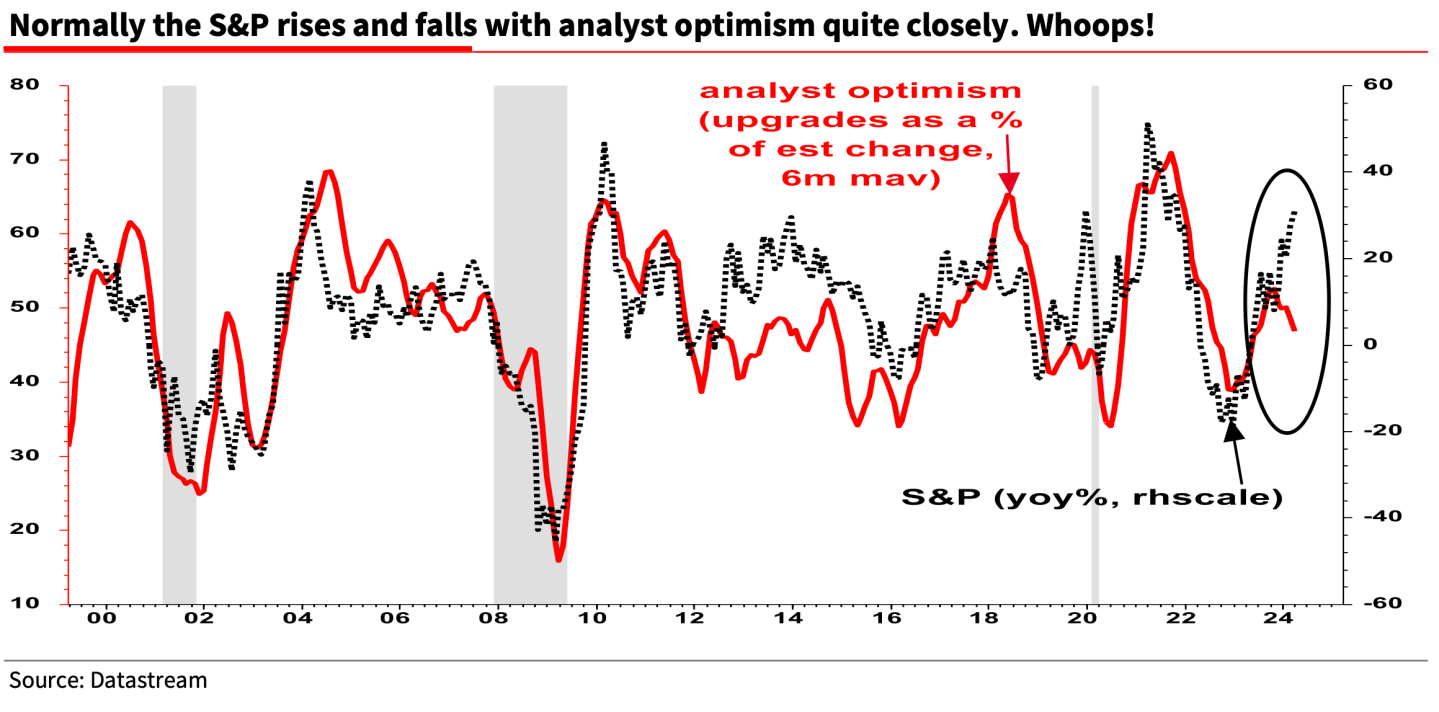

Edwards said that the theory that Al will drive a corporate profit boom is “entirely plausible,” but he hasn’t seen enough earnings growth to back it up. In a bid to measure “momentum” in earnings growth, the strategist looked at the percentage of Wall Street analysts’ S&P 500 earnings per share (EPS) forecast changes that were upgrades, rather than downgrades. He found that in the fourth quarter of 2023 around 48% of analysts’ EPS estimate changes were upgrades, compared with nearly 80% in early 2021. Similarly, a six-month moving average of the EPS upgrade percentage shows a clear trend of fewer analyst upgrades at the end of last year.

“All I can say is that for analyst optimism on the S&P to have topped out only at 50% before subsiding is not the stuff of normal cyclical recoveries, let alone an AI ‘new era,’” Edwards wrote. “But it is the downtrend that catches my eye. Is this anemic profits backdrop really consistent with the S&P rising by one-third in a year?”

It’s not AI driving markets, it’s ‘loose’ monetary policy

Edwards argued Thursday that while many experts believe stocks’ nearly 10% year-to-date rise has been driven by the potential for AI to boost earnings, “it may simply be excessively loose monetary policy that is the key reason why the S&P is at record highs.”

Despite raising interest rates to fight inflation and reducing the size of its balance sheet, the Fed is actually increasing the U.S. economy’s monetary base, according to Edwards. That means monetary policy isn’t as tight as many imagine. The much-ballyhooed end of the “easy money” era doesn’t mean that money has been hard to come by, in other words, at least for now.

“It is a joke to even suggest that monetary policy is restrictive,” Edwards argued, noting that the Fed’s money market operations are “pumping enough liquidity into the system” in the form of reduced reverse repos to more than offset the impact of the Fed’s efforts to suck “easy money” out of the economy through a process called quantitative tightening. Hence, he concludes, there has been an increase in “base money” even as quantitative easing has shifted to tightening.

As for the stock market rally, Edwards said, “maybe it’s all about Fed-induced liquidity after all” and the AI boom is just a narrative that makes sense of the trend.