If any CEO has earned a big payday over the past few years, it might be Cynthia Warner.

She’s not a household-name CEO. But in the three years since she became chief executive of Renewable Energy Group, a producer of “bio” diesel and other fossil-fuel alternatives, Warner has generated plenty of value for her company’s public shareholders. During Warner’s tenure, Renewable Energy’s stock has returned 29.1% to investors on an annualized basis—far outstripping the performance of its energy-industry peers and of the broader S&P 500, which returned an annualized 16.5% during the same period. In February, Warner helped line up another big payday for her shareholders, when Chevron agreed to buy the company. The oil giant is paying almost $3.2 billion—more than a 40% premium to Renewable Energy’s closing share price at the time of the deal—to take over Warner’s company and its green-energy focus.

Assuming the deal goes through, the big winners will be her company’s largest investors—and Chevron’s board, executives, and public-relations team, who are, like all oil-and-gas companies, facing mounting scrutiny and shareholder pressure over their responsibility for climate change. That’s another area where Warner’s company appears to be outperforming its larger, traditional peers: As CEOs across industries say they are embracing the environmental and social goals of such “stakeholder capitalism,” Renewable Energy is actually in the business of reducing greenhouse-gas emissions—without sacrificing financial returns for its public shareholders.

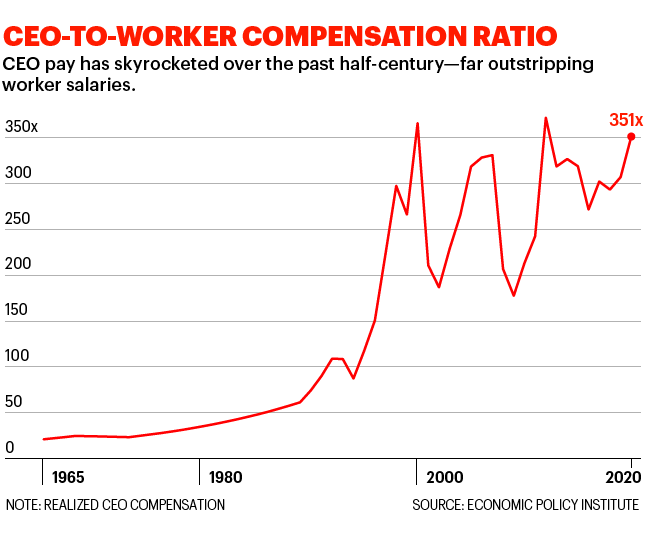

Her accomplishments netted Warner a 2021 compensation package valued at almost $4.5 million—a tidy sum, but a fraction of the skyrocketing CEO paydays among Fortune 500 companies. (Her counterpart at the much larger Chevron, CEO Michael Wirth, earned a package valued at $22.6 million.) And her 2021 payday also stands out as remarkably moderate by one key metric: Warner’s total 2021 compensation gives her only 49 times the typical salary that she pays her employees, who earn a median of $92,556.

That’s a quaint throwback to 1990—the last time that the average large-company CEO was granted compensation worth around 50 times a typical worker’s salary, according to the Economic Policy Institute (EPI). In 2021, Fortune 500 CEOs picked up pay packages worth a median of 205 times a typical worker’s annual salary. Meanwhile, average U.S. hourly wages fell 2.4% last year, when adjusted for skyrocketing inflation.

“Do we really think you have to earn hundreds of times more than your typical worker to get out of bed and do a good job?” asks Lawrence Mishel, the economist and former president of EPI, who has spent decades tracking the pay ratio between CEOs and their workers. “Would [companies] not be able to fill these jobs? I think they could.”

It’s one of many criticisms during proxy season, the period every spring when public companies reveal, in stultifyingly opaque detail, how much they’re paying their top executives. Once again, this year’s disclosures are breaking records—and drawing scrutiny. Chief executives at some of the largest companies by revenue have been awarded a median $20 million in total compensation, according to a mid-April report by Equilar, and some earned far more—often to the ire of their investors. Earlier this month, shareholders at companies including JPMorgan Chase and Intel voted down their CEOs’ pay packages—although, like all such “say on pay” votes, their objections are non-binding and the companies do not have to change anything as a result.

The CEO-worker pay ratio sometimes draws less attention than the total dollar figures bestowed upon top executives, in part because even some critics of executive compensation disagree about how relevant it is to their pay-reform proposals. But as a metric that all public companies are now required to disclose in their proxy legalese, it provides a useful—and often dramatic—snapshot of the link between how much value companies place on an individual’s leadership, versus the contributions of their rank-and-file employees.

This widening pay gulf is also helping to fuel the record, toxic wealth gap, which business leaders across the political spectrum are calling a national emergency. Even on a more short-term, self-interested level, some corporate governance experts warn, private employers should worry about the reputational risk—and potential shareholder revolts—that could be sparked if companies continue to excessively overpay their executives.

“It’s in people’s self-interest to try to contain this,” says Rosanna Landis Weaver, wage justice and executive pay program senior manager at As You Sow, a non-profit shareholder-advocacy group. “The political instability that is created by income inequality is a real danger. It’s a danger to democracy, and it’s a danger to capitalism.”

But if CEOs are vastly overcompensated relative to their workers right now, how much should they be paid?

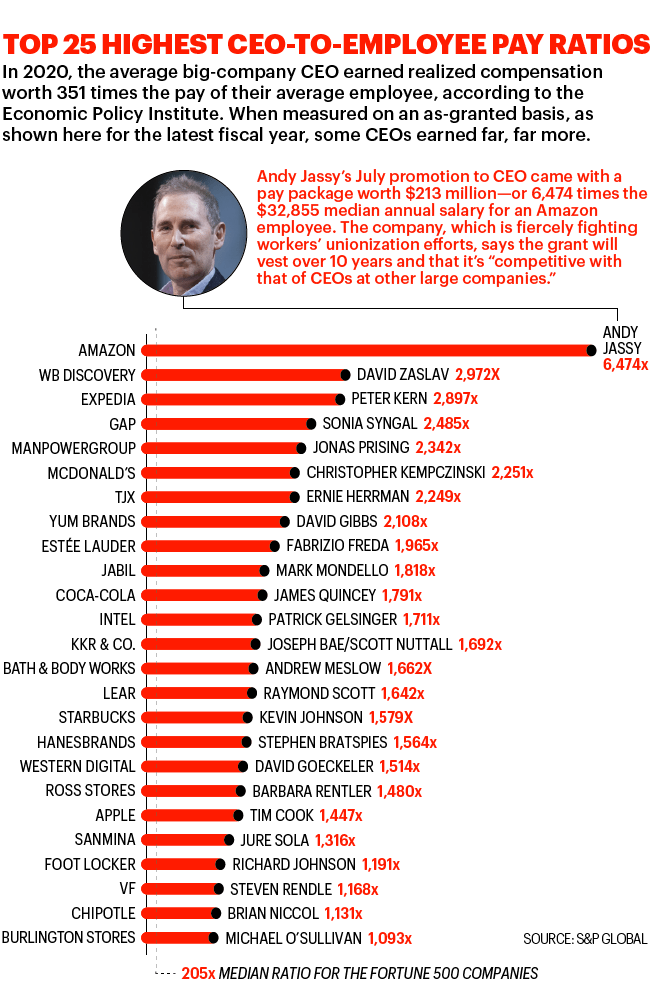

A 6,474-to-1 ratio for Amazon’s CEO

Some of the most highly paid CEOs last year also had some of the largest pay ratios. At Warner Bros. Discovery, for example, David Zaslav’s $247 million in granted compensation is 2,972 times his median worker’s salary of $82,964. Amazon CEO Andy Jassy is earning a little less, but also far more: His 2021 pay package of $213 million is 6,474 times his median worker’s salary of $32,855—giving him the highest CEO-to-worker pay ratio of all the Fortune 1000 companies that had filed proxy statements through the end of April, according to a Fortune analysis.

Much of what has led to these skyrocketing CEO raises has to do with how top executives are actually paid. Salaries have become negligible—which, cynically, might explain why so many CEOs were so willing to sacrifice them during the pandemic’s early days. At Amazon, for example, Jassy earned all of $175,000 in salary last year. (This may be the only financial metric by which Ames, Iowa-based Renewable Energy Group—a mere Fortune 1000 player—ranks above the country’s second-largest company: It paid its CEO $900,000 in 2021 salary.)

Instead, big CEO paydays mostly come in the form of “restricted stock units,” or grants of company shares that can only be redeemed years down the road—and which, in theory, incentivize executives to work towards longer-term goals, instead of short-term earnings and stock-price bumps. Such grants are supposed to give executives personal incentives to raise the company’s stock price, so that they reap the financial benefits—or suffer the downsides—of what they return to shareholders.

For example, Amazon in 2021 awarded Jassy stock units worth $212 million, although the total value of those grants will likely change—and could very well increase—by the time he redeems them. Amazon also noted that this grant, which will vest over the next 10 years, is tied to Jassy’s July 2021 promotion to president and CEO, and is “expected to represent most of Mr. Jassy’s compensation for the coming years.” (At Renewable Energy Group, in contrast, Warner was awarded restricted stock units valued at $2.2 million for 2021—slightly more than what she was awarded in 2020, and slightly less than in 2019.)

An Amazon spokesperson says that Jassy’s 2021 pay package and what it “equates to from an annual compensation perspective is competitive with that of CEOs at other large companies.” A Renewable Energy spokesperson declined to comment.

Even with restrictions on when CEOs can actually cash in, their paydays are inarguably huge. Fortune’s new list of the 10 Most Overpaid CEOs, which analyzes how much each executive took home or “realized” last year, found that the chief executives we evaluated earned a median total compensation of $15.9 million in 2021—up 30% from a year earlier. Overall, realized CEO pay has skyrocketed 1,322% since the late 1970s through 2020, according to EPI, far outpacing wage growth of 18% over that same period.

“Right now, when those folks do well, others are doing incredibly poorly,” says Abigail E. Disney, the filmmaker and Disney heir who has become an outspoken critic of CEO pay, especially at the company her great-uncle and grandfather founded. (In 2021, Disney CEO Bob Chapek was awarded a pay package valued at $32.5 million—644 times the median Disney employee’s annual salary of $50,430.)

Since the labor of both workers and executives contributes to a company’s bottom line, Abigail Disney argues that companies should provide a larger share of returns to its employees—especially the lowest-wage ones “at the bottom of the pile.” The current pay ratio disclosure mandated by regulators focuses on median wages, but Disney proposes that CEO compensation should be capped at a few hundred times the annual salary each pays their lowest-paid employee.

“We all have the same basic needs,” she argues, “and we all have the same basic value.”

Incentives and “mega-grants“

The godfather of modern CEO pay was a McKinsey consultant named Arch Patton, who in 1951 published the first multi-industry survey on executive compensation. He found—somewhat inconceivably now—that hourly workers’ wage growth had actually outpaced that of their senior managers. Soon Patton was writing books and advising Fortune 500 board rooms on how to use bonuses and stock options to attract and retain executives; for several years, he personally accounted for almost 10% of McKinsey’s billings, according to the journalist Duff McDonald, author of the 2014 book The Firm: The Story of McKinsey and Its Secret Influence on American Business. By the mid-1980s, Patton reportedly said he felt “guilty” for contributing to skyrocketing executive pay, according to his New York Times obituary.

More recent government policies and private-sector decisions have encouraged boards to double-down on high-value, time-restricted grants. Several experts attribute the increasing popularity of stock-based executive compensation to early 1990’s changes to the federal tax code, which effectively capped individual salaries for companies’ top executives at $1 million. Senior-executive salaries above that threshold could not be deducted from corporate taxes—but there was a loophole for performance-based stock grants, giving companies even more reason to embrace such incentives. (The 2017 tax law eventually eliminated this exemption, meaning that companies can no longer deduct any compensation above $1 million, including stock grants.)

Meanwhile, the tech boom has led to the rise of the “mega-grant,” which is breathtakingly excessive even for mere millionaire CEOs. In 2011, Apple helped pioneer these grants by awarding incoming CEO Tim Cook with a 10-year package of restricted stock eventually worth $1.7 billion. Today, CEOs with similar high-stakes compensation agreements include Tesla CEO and would-be Twitter owner Elon Musk—whose 2018 multiyear “moonshot” pay package landed him nearly $23.5 billion in realized compensation in 2021. Musk has cleared a path for tech founders with much less name recognition to make similar demands: In April, ad-tech company Trade Desk awarded CEO Jeff Green a pay package valued at $835 million, in stock options that will vest in eight batches over the next decade. (Even so, Green didn’t outstrip Jassy’s worker-pay ratio at Amazon; since the Trade Desk CEO pays his typical employee almost $195,000, his 2021 package equates to only 4,283 times their median salary.)

The companies that hand out these pay packages, and the compensation advisers who design them, say that massive, stock-tied paydays are necessary to recruit and retain talented executives—especially in an era where public companies have to compete with highly valued, privately funded startups, or with the hedge funds and cryptocurrency firms that have created runaway wealth for some founders and executives.

“The system isn’t necessarily broken,” says Margaret Engel, a founding partner of Compensation Advisory Partners, which designs pay packages for Fortune 500 companies. “There are some individual examples out there of companies who push the envelope—but it generally works.”

Time for a compensation cap?

Over the past several weeks, I’ve spoken with many experts who disagree—although they didn’t always agree about how to build a better system. “If you ask 10 different executive compensation folks, you’re going to get 10 different responses about what’s wrong—and how to fix it,” acknowledges Michael Varner of SOC Investment Group, which works with union pension funds. (His proposal: Eliminate performance-based equity grants, and pay CEOs in smaller grants of “full value awards” that vest over time, such as restricted stock units.)

And it admittedly would be complicated to design a one-size-fits-all fix to CEO pay, especially given the wide variety of industries in the Fortune 500; the vastly diverging levels of performance among individual companies; and even the different ways to measure performance.

Many boards choose to judge executive performance against the company’s stock-market returns, as well as against the performance of “peer groups” of other companies. But Nell Minow, a corporate governance expert and vice chair with ValueEdge Advisors, argues that boards should tie more CEO pay to peer groups, and less to overall market performance. That way executives would be judged more on their company’s individual performance within a sector—and less rewarded for things that boost (or hurt) all of their peers. (Think a runup in oil prices that juices revenues, and share prices, for all energy companies—or a global pandemic that effectively shuts down the airline industry for months.)

But in Minow’s experience—including as a former president of the powerful proxy advisor Institutional Shareholder Services—as much as 70% of executives’ options-based pay is attributable to the market as a whole. This means that, in essence, these leaders are being judged and rewarded on the market’s overall performance, rather than the individual performance of the companies they run.

“We’re paying [CEOs] to beat the competition,” she says. “We shouldn’t be paying them because the market goes up—and yet, that is exactly what we’re doing.”

However, even Minow’s proposed fix has pitfalls: Peer group comparisons can also be manipulated to help juice a CEO’s pay. A 2019 academic paper found that “companies tend to choose [peer] firms that historically underperform” and are thus easier to beat, explains one of the paper’s authors, University of Delaware finance professor Hamed Mahmudi.

It’s also worth noting that, despite companies—and institutional investors’—mounting rhetoric over environmental and social goals, these commitments have yet to make a big dent in CEO pay. In 2021, 50% of companies included ESG in their compensation targets, up from 30% in 2019, according to an April report from Compensation Advisory Partners—but the firm acknowledges that those goals only account for “usually 5 to 15 percent” of annual incentives. “By far, CEOs are still mostly paid out on financial performance,” says Lauren Peek, a principal with CAP.

Even the harshest critics of CEO pay generally declined to put hard dollar figures or ceilings on their proposed compensation fixes. One exception was a casual estimate by EPI’s Mishel, who argues that top executives’ pay “could be cut in half, or more” without damaging companies’ economic efficiency—or their ability to attract and retain senior talent.

But several critics focus on the CEO-to-median-worker pay ratio, in part because it’s one of the clearest numbers in the morass of proxy-statement legalese. Companies only had to start disclosing these ratios in 2018, after the SEC finalized a rule as part of the Dodd-Frank financial reform law. Since then, these ratios have inspired specific proposals from both shareholders and lawmakers. A year ago, Sen. Bernie Sanders introduced a bill that would raise corporate taxes on companies whose CEOs earn more than 50 times a typical worker’s salary.

Meanwhile, As You Sow recommends that shareholders vote against any pay packages with a CEO-worker pay ratio higher than 100 to 1. Weaver acknowledges that choosing this ratio “was a matter of much discussion internally,” but that As You Sow had to balance practical considerations of the talent market today. “I can’t imagine a situation where one person contributes as much as 100 people do,” she says, but for S&P 500 companies, “we concur that there might be hiring and retention risks if ratios were set too low.”

Back at Renewable Energy Group, one of the relatively few companies that meets As You Sow’s threshold, Warner’s 49-to-1 pay ratio is unlikely to be repeated. Chevron’s deal to buy the company is likely to close later this year, at which point Warner is supposed to join the oil-and-gas giant’s board, the companies have announced.

The consummation of the deal is also likely to make Warner a much-better-compensated executive.

She owns a stack of Renewable Energy’s stock, which—while under 1% of shares outstanding—will be worth about $7 million at the sale price. If Warner leaves after the merger is complete, she’ll also be eligible for a “golden parachute” compensation package valued at $15.2 million, according to the company’s proxy statement.

It’s a generous payday indeed—and the vast majority of Renewable Energy’s shareholders voted to approve it.

Read more: Meet the 10 Most Overpaid and 10 Most Undervalued CEOs in the Fortune 500