Steve Jobs had been wheeled into the boardroom for what would be the Apple director’s last meeting of his life. It was Aug. 24, 2011. Chief Operating Officer Tim Cook and CFO Peter Oppenheimer made presentations on the company’s latest progress. Then Jobs, weakened by pancreatic cancer and speaking from his wheelchair, asked everyone but the outside directors to leave the room. Once they had, he said he could no longer carry out the duties of CEO. As expected, he recommended that Cook succeed him. The board passed the necessary resolutions. Jobs stayed for lunch, after which the directors hugged him in turn, and he was driven home. He died six weeks later.

That dramatic scene, chronicled by Walter Isaacson in his Jobs biography, marked a milestone in U.S. business history. It was the emotional final farewell of an all-time great entrepreneur and innovator. Against such a momentous backdrop, the board’s formalities in transferring power surely seemed insignificant. It turned out, however, that one of the board’s actions that day—giving Cook a new pay package—would prove far more important than it seemed at the time.

Cook’s compensation package arguably played a role in making Apple the world’s most valuable company. It made Tim Cook a billionaire. More broadly, it changed CEO pay profoundly, and its influence is still expanding. As this year’s proxy season unfolds, all the most eye-popping as-reported CEO pay packages—Warner Bros. Discovery CEO David Zaslav’s $247 million, Amazon CEO Andy Jassy’s $213 million, Intel CEO Pat Gelsinger’s $179 million, and many more—can trace their lineage to that board meeting more than a decade ago.

The rise of the ‘mega-grant’

When the board promoted Cook to CEO, it gave him a grant of “restricted stock units” representing Apple shares that he would receive on future dates so long as he was still employed. Such grants have long been a common device for retaining executives and incentivizing them to raise the stock price—but this was unlike any that had come before.

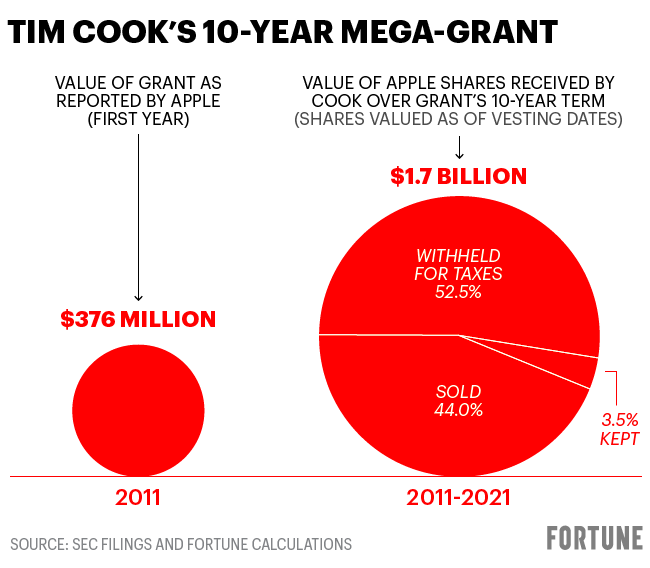

Restricted stock awards typically vest over three to five years. This one spanned 10 years. Even more remarkable was the grant’s breathtaking size: one million shares of a stock that was trading at $376 a share.

The grant’s vesting schedule ended last August, on the 10th anniversary of that unforgettable board meeting. Through stock splits, the original million shares had become 28 million shares, though Cook didn’t get quite that many, as we shall see. Still, on the grant’s final day, the shares he had received over the grant’s life were worth more than $4 billion—$4,159,519,189, to be exact. (Apple declined to make any comment for this article.)

Previous restricted-stock grants were considered big in their time. In the 1990s, Coca-Cola CEO Roberto Goizueta and Hewlett-Packard CEO Carly Fiorina made headlines when each received grants valued at about $80 million. (The price of Coke’s shares rose during the vesting period for Goizueta’s grant, while HP’s stock plunged in the dot-com bust as Fiorina’s grant was vesting.) Cook’s grant was so much larger, however, that in effect it reconceived the restricted stock grant. A comprehensive study in the Journal of Compensation and Benefits identifies Cook’s grant as launching the era of the “mega-grant.” Rankings of the highest-paid CEOs in any recent year, not just this year, are topped by mega-grant recipients.

Eight- and nine-figure pay numbers spark disbelief, envy, and outrage. In the age of the mega-grant, two important questions immediately arise: Are such giant awards a good thing? And when we read the massive figures, what do they mean—specifically, are we learning how much money CEOs really make? The best way to answer both questions is to examine the proto-mega-grant, Tim Cook’s.

The answer to the first question—whether today’s mammoth awards are good—is an emphatic “That depends.” Stock grants are infinitely variable; details matter. Cook’s grant, like virtually all restricted-stock grants before his, was initially time-based. The recipient had only to stay employed at the company through the vesting schedule to get the shares. Even if the price went down through CEO incompetence, the shares were still worth something, and they were typically awarded on top of salary, bonus, and perks. Bottom line: Restricted stock 1.0 was effective at retention but otherwise not a great incentive.

In Cook’s second year as CEO the board moved to version 2.0, adding a performance requirement to his grant (at his request, the company says). Vesting hadn’t yet begun. Under the revised plan, starting in 2013 about one-third of his grant would be based on Apple’s total shareholder return (TSR) relative to the S&P 500. Great performance wouldn’t get him any more shares, but if Apple’s TSR wasn’t in the top third of the S&P, he could get fewer or no shares that year.

The penalty took effect just once, in 2013. As a result, Cook ultimately received 27.8 million shares of the potential maximum 28 million.

So are mega-grants a good thing? A huge grant with three-year time-based vesting is hard to defend; it’s little more than a gift. Sometimes it has to be offered to land an outsider CEO who’s forfeiting a similar grant from a previous employer, but it’s still a subpar incentive. By contrast, a five- to 10-year grant with at least partial performance-based vesting—though one featuring a heavier performance component than in Cook’s plan would be better—forces a CEO to think long-term. In Cook’s case, the grant incentivized him to show he could do more than just ride Jobs’ momentum.

Some observers are outraged that a non-founder CEO could become a billionaire entirely through pay, as Cook did. The way to judge such CEOs is against the fortunes of the shareholders. With Cook at the helm, Apple’s market value has increased by $2.2 trillion. His stock grant plus all the other forms of compensation he has received in his years as CEO (salary, incentive pay, perks) have in total brought him less than 0.1% of that amount. It’s hard to argue that the shareholders got a bad deal.

The second question asks what the reported pay of mega-grant recipients tells us, specifically whether we’re learning how much money they’re getting. The answer to that one is simple: No. Don’t believe those numbers. They’re almost certainly wrong, and if they’re right, it’s only by coincidence.

Here’s why: Accounting standards and SEC rules require that companies report the value of a stock grant like Cook’s by simply multiplying the number of shares by the share price on the date of the grant. In Cook’s case, the result was $376.2 million. Add his salary, incentive pay, and perks, and his 2011 pay was reported in headlines nationwide as $378 million, the largest pay package of any CEO in America that year. In Apple’s SEC-filed documents, the value of his grant would never be reported as any other amount.

But such valuations, seemingly precise, are estimates of amounts that won’t be known for years—and the estimates may turn out to be radically wrong. Stock grants have grown far more complex since 2011, sometimes linked to multiple specific performance measures and valued using head-spinning statistical techniques, but the problem hasn’t changed.

Cook’s grant is an illuminating example. Investors cannot easily find the value of what he received from his grant, but SEC filings over the past decade, rarely publicized in the media, report the data. The result is revealed here for the first time.

Cook received his shares in 10 tranches from 2013 to 2021. With all shares valued at their market price on the day he received them, they were worth $1.7 billion—over four times more than the value of the grant as reported in Apple’s proxy statement.

As noted above, those shares would have been worth over $4 billion on the day he received his last tranche, in August 2021, and would be worth even more now. But Cook didn’t keep them all. In fact, he kept only about 11% of them.

What happened to the rest? He never saw most of the shares he was awarded during the years of his grant; Apple withheld them for taxes, as required by law. As a result, 52% of his grant went directly from Apple to the tax authorities. Of the remaining shares, Cook sold three-quarters of them, receiving proceeds of $739 million.

In retrospect, dumping all those Apple shares may seem like an egregious personal finance blunder. But Cook was following a strategy used by many CEOs and founders who realize it’s imprudent to hold the vast majority of their net worth in a single asset. They file a plan with the SEC under which they sell shares on a regular schedule, enabling them to reduce their exposure to company stock without violating insider trading rules. Whether Cook sacrificed significant wealth by selling all that Apple stock is unknowable since we don’t know how he invested the proceeds—though it would take a superstar portfolio to have outperformed Apple.

Figuring all this out is hard work, which exposes another problem with mega-grant reporting. Investors care about the details of a CEO’s wealth. A CEO who holds virtually all their net worth in company stock could be seen by investors as an utterly devoted manager, or could be seen as too risk-averse, unwilling to take chances with the basket holding all the CEO’s eggs. A CEO’s holding of company stock is reported in the annual proxy statement, but that’s only half the story: Finding data on how many shares a mega-grant recipient didn’t keep, and the proceeds from selling them, requires combing through SEC documents and building a spreadsheet—not something many investors will do.

The errors in reporting mega-grants’ values can be wrong in either direction. The value of Cook’s grant was drastically understated, but other grants have been hugely overstated. A notable example—rich with irony when compared with Cook’s—is that of Ron Johnson. When Cook’s mega-grant made him America’s highest-paid CEO in 2011, Johnson ranked No. 4 as JCPenney’s new CEO, with total pay of $53.2 million; of that amount, $52.6 million represented a mega-grant of restricted stock. His grant vested in full on his first day at work, and he held the shares (after tax withholding) through his famously brief tenure. When the board fired him after 17 months, the stock had plunged 50%—and so had the value of his grant. Penney struggled on for years thereafter and filed for Chapter 11 bankruptcy in 2020.

As for the irony: Before joining Penney, Johnson was an Apple executive, the mastermind who built the company’s highly successful retail business. He left Apple for Penney shortly after Cook became CEO. Penney gave Johnson that mega-grant to compensate him for forfeiting unvested grants at Apple. It was an unfortunate trade. Had Johnson stayed at Apple long enough for the grants to vest, his shares would today be worth $1.1 billion.

Cook’s new pay package

Mega-grants of eight or nine figures are still rare. But because they fill the top positions on lists of the highest-paid CEOs, those CEOs attract extra attention and fuel cries to regulate exorbitant CEO pay. Tim Cook, his original mega-grant, and Apple’s extraordinary performance over the past decade remain one of the strongest arguments that massive pay can be worth every cent.

But the case isn’t closed—because now he’ll have to prove it all over again. Apple’s board gave Cook another mega-grant in the company’s fiscal 2021. It’s valued at $82.3 million with vesting scheduled in 2023 through 2025, when Cook will reach age 65.

If Cook can reprise or even approach his past performance, he will powerfully strengthen the argument that mega-grants make sense, and that the flowering of such giant awards is a good thing, not a bad thing. But if he falls significantly short, critics will argue that such grants merely heap riches on CEOs who get lucky. Matching his own record will be staggeringly hard. The S&P 500 delivered a stunning total shareholder return of 366% in the decade of his first grant, and Apple whomped it with a TSR of 1,197%.

Can Cook possibly repeat that achievement? Apple’s shareholders—and aspiring mega-grant recipients everywhere—are praying that he can.

Sign up for the Fortune Features email list so you don’t miss our biggest features, exclusive interviews, and investigations.