Rene Haas wants me to know he’s not the anxious type. “I’m not a worrier by nature,” he says. “I don’t mean to sound overly coy. But one of the things I like most about being in the technology business is that it changes so fast.” Change might unsettle some. Haas, the new chief executive of the computer chip design company Arm—whose technology is in practically every one of the world’s smartphones—wants me to know he isn’t one of them. “I just view that as opportunity,” he says.

Good thing too. Because, if Haas were a worrier, he might not be getting much sleep. The pioneering chip-design company faces challenges that would keep most executives tossing and turning.

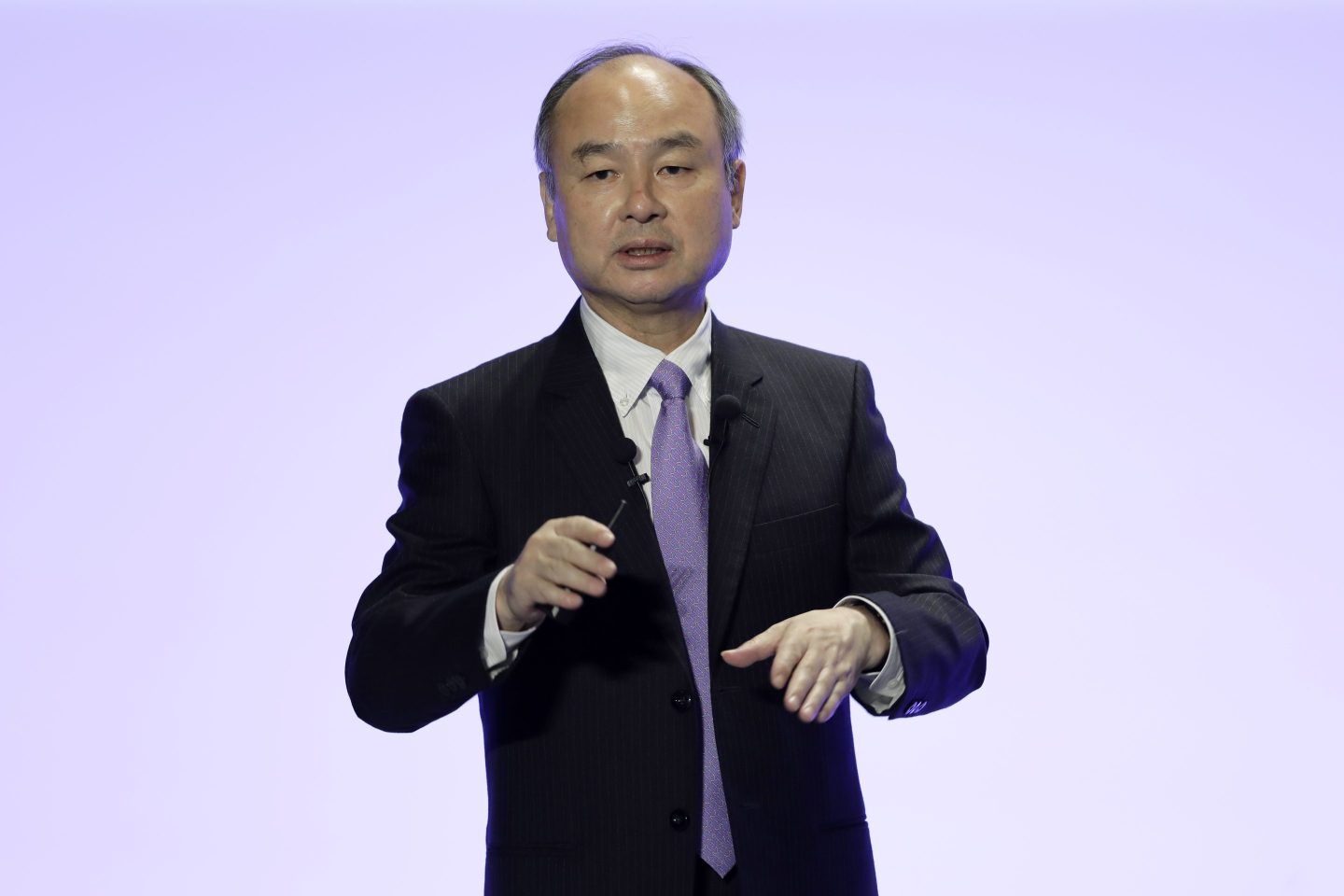

Among Haas’s top priorities is preparing Arm for an IPO, following the collapse of the company’s much-hyped sale to Nvidia, in what would have been the biggest acquisition in the semiconductor industry’s history. But the market for tech IPOs is suddenly softer than it’s been in years—even as Arm’s current owner, Japanese tech conglomerate Softbank, run by billionaire CEO Masayoshi Son, wants to take Arm public at a price-to-earnings valuation far higher than a semiconductor company has ever commanded. Indeed, the pressure on Softbank to achieve a high valuation is more intense than ever: Thanks to the recent rout in tech stocks, Softbank’s Vision Fund, which own some of Arm’s shares, posted a stunning $27 billion loss for the fiscal year through March. (Softbank, the conglomerate, lost more than $16 billion.)

Following years of expansion, Haas has just announced a painful round of layoffs, in part to streamline Arm’s cost structure ahead of that IPO. Plus, he has to deal with a renegade Chinese executive, supply chain chaos, geopolitical tensions from Ukraine to Taiwan, and increased competition from rivals large and small.

Few consumers know Arm by name, and it isn’t a huge company: It had revenues of $2.7 billion last year. But more chips based on its technology are shipped every year than those from any single semiconductor company, including better known brands such as Intel, AMD and Nvidia. Last year, that amounted to more than 29 billion chips worldwide. In fact, more central processing units—the general-purpose brains inside most computers—using Arm’s instruction set are shipped each year than those of all other rivals combined. Once synonymous with the smartphone revolution, Arm is today a bellwether for the semiconductor industry—and computing more generally. Known for designing power efficient chips, the company is well positioned for a world where energy costs, carbon footprints, and “Net Zero” pledges are at the forefront of the business agenda.

But Arm is also facing a world where Moore’s Law, the principle that the number of transistors that can be crammed onto the same silicon real estate doubles every two years while the price of a given amount of computing power is halved, is faltering. The investment needed to continue to cram more transistors into ever smaller spaces—while still turning a profit—has forced consolidation among large semiconductor producers. At the same time, the slowing of Moore’s Law has triggered a pre-Cambrian explosion of chip design startups, some with radical new ideas for how to configure chips and yoke them together. How quickly these technologies evolve and how companies like Arm respond to the new competition will determine how fast innovations like artificial intelligence, electric vehicles, and 5G become ubiquitous facets of our lives.

Haas and I are sipping coffee in the lobby of London’s St. Pancras Hotel. Haas, who is 59, is tall and lean, with a shock of gray hair swept back from his brow and a well-curated, stubbly goatee. He has flown in from San Jose, where he—like Arm’s previous CEO, Simon Segars—is based, along with a cadre of Arm’s top execs. He is en route to Arm’s headquarters in Cambridge, England—his first visit since assuming the company’s helm. Later in the week he will host a drinks party to welcome employees back to Arm’s brand-new headquarters building, which opened during the pandemic, as well as to wish Segars, a 31-year veteran of the company, farewell.

But first he needs to stop by No. 10 Downing Street: Having helped block Arm’s sale to Nvidia, the British government is now lobbying the company to list its shares on the London Stock Exchange rather than on the Nasdaq or the New York Stock Exchange. Arm has long-been one of the U.K.’s most prominent examples of homegrown tech success. A defection to the U.S. now would be another symbolic blow to a British financial sector that has endured a loss of prestige, influence, and actual capital since Brexit. But the Prime Minister’s hand is weak, not least because U.S. investors have been more willing to entertain eye-wateringly high tech valuations. (As of mid-May, Son had said he wanted Arm to go public “in New York,” but Softbank and Arm had not confirmed an IPO venue.)

Concerns about U.S. securities law prohibit Haas saying much about the IPO—which Son has said he wants to take place within Softbank’s current fiscal year, which runs through March 2023. But Haas tells me he is far more focused on opportunities five to ten years out than on what will happen in the next one to two years. Haas, a U.S. national and a semiconductor industry lifer, thinks Arm has a good chance to gain share in markets where it’s only had toeholds before: the datacenters that power cloud computing, a new generation of laptops and tablets, and in the vast new network equipment being deployed to support the rollout of 5G telecommunications. He also sees big growth potential in the automotive industry, with cars that increasingly function as smartphones on wheels and the electric vehicle revolution requiring careful use of precious battery power.

But success will require doubling down on a strategy Haas put in motion during the five years he headed the company’s intellectual property group—tailoring how the company markets its products for specific industries in which its customers are concentrated. The strategy is likely to require substantial investment, potentially eating into the company’s already modest margins. And it’s likely to take patience, a quality for which public-market investors are not renowned. The need for Arm to prioritize short-term investment in order to realize long-term gains was a point Son emphasized when he purchased Arm in 2016, and that Arm itself trotted out in its failed attempt to convince regulators to approve the Nvidia deal: that Arm would be a better business when shielded from the direct pressure of quarterly earnings and market fads. Now Haas to prove this logic was wrong all along—and that Arm can remake its business while delivering investor-pleasing earnings at the same time.

The ‘Switzerland of semiconductors’

Arm was founded as Advanced RISC Machines in 1990 in a converted barn in Cambridge. (RISC is a kind of simplified code used to program computer processors.) It was initially a joint venture between Apple and two other companies, and Arm’s task was designing the computer chips that would power the Apple Newton, one of the world’s first tablet computers. From there, the company pioneered a new kind of semiconductor business model: it did not produce the processors it designed. Instead, it simply licensed the designs to others, and then collected royalties for every circuit board incorporating that design that the customer ultimately shipped.

A key part of the company’s strategy was that it would be a neutral player—the “Switzerland of semiconductors”—licensing its technology to any qualified customer, rather entering exclusive relationships with a single company or tech ecosystem. Arm’s business prospects rose on the wave of digital mobile phones in the mid-1990s. The company went public for the first time, with a dual listing on the Nasdaq and the LSE, in 1998. It went on to dominate the smartphone market in the late 2000s.

In addition to designs for computer processors, Arm also licenses its “architecture”—the set of instructions for how computer code will actually be executed by a processor—to anyone who wants to buy it and then design their own processor to be compatible with it. This is what Apple, for instance, now does for the chips in its iPhones. Arm’s architecture is now the most pervasive in the world, used in hundreds of billions of chips, including those in almost every smartphone in the world—its market share for smartphone CPUs is well above 95%.

Son stepped in to buy the company in 2016 for $32 billion. At the time, the Japanese mogul said that the purchase was part of a “30-year vision” for a world in which artificial intelligence would be infused into everything from smart traffic lights and household thermostats to flying cars. He saw Arm’s technology as a key enabler of this vision.

With Son pushing the company aggressively for growth, Segars, the CEO at the time, reorganized Arm into two big units. The company’s licensing and royalty business—“classic Arm” as Haas calls it—became the Intellectual Property Group. The other unit was a new business dedicated to software for the Internet of Things. That buzzword postulated a future in which all kinds of stuff, from toasters to toll booths, was connected to the Internet. Arm’s IoT division was essentially a brand-new software services business that would help customers manage and secure all those thousands of Web-enabled things.

Haas, who had been at Arm for about three years at that point, was put in charge of classic Arm. He set about transforming the way the IP Group approached the market. Before, the company had designed processors and its architecture for big horizontal technology segments: a few types of central processing units for different performance and energy profiles, a graphics processing unit, and low-powered microcontrollers. It sold these mostly to “system-on-a-chip” (SOC) companies that would have the chips made and then integrate them into circuit boards to meet the needs of various end-users, be it a smartphone maker or auto parts company or Google.

But Haas says this “one size fits all” approach was limited. What worked for smartphones wasn’t quite right for datacenter customers. “We were starting to run out of runway,” Haas says. So Haas transformed the IP Group into big industry-oriented verticals: one around automotive and industrial customers who need safety critical features; another geared towards consumer devices from mobile phones and tablets to laptops; and another aimed at the big “hyperscalers”— Amazon Web Services, Microsoft Azure, Google Cloud, IBM, and Oracle—that dominated the datacenter business.

While Arm kept its engineering team centralized, it began to allow customization, in both hardware and software, to meet the needs of these industry verticals. Under Haas, the company unveiled its first product—Arm’s Neoverse CPU—geared specifically for datacenter hyperscalers. The company also created a line of “automotive enhanced” central processing units with better features for what is known as “functional safety.” These are systems that automatically detect and mitigate faults caused by random errors, and they are essential for automotive and industrial use cases. Dipti Vachani, who Haas hired away from Intel to head the automotive and IoT team for the IP Group, says the company was able to tweak the Arm architecture so that Amazon could get improved audio signal processing for Alexa. “That means going into the architecture and the pipeline of the architecture to make sure we can get signals processed for the lowest possible power, because you can imagine they care about that,” she says. Arm has done similar “fine-tuning” of its IP to serve other customers too.

Arm also decided to get much closer to the users of its technology. “We took it up a few notches in terms of talking to your customer and your customer’s customer and your customer’s customer’s customer,” Haas says. In the automotive segment, for example, Arm would once have primarily engaged with companies like Infineon, Texas Instruments, and Renesas, that supply SOCs to various automotive parts companies. Now it sought to have relationships with the parts suppliers themselves. Plus, Haas says, Arm also started speaking directly to the likes of Toyota, General Motors, and Audi, as well as Google and Blackberry QNX, that make the software the cars run. This strategy allowed the company to better understand the problems its technology was meant to solve, Haas says, ensuring that Arm would have designs with the right kind of capabilities out in the market at the right time.

Haas also took steps to make it less expensive for startups to license Arm’s technology, with the idea being that Arm would eventually earn more in royalties if more companies had access to Arm’s IP. He also felt a focus on royalties would help as the semiconductor industry—the SOC players—consolidated. “Ultimately [royalties] were going to be the growth engine for the company,” he says.

By all accounts, Haas was willing to get creative to make deals happen. Matt Murphy, the chief executive of Marvell Technology, which makes systems for datacenters, says Haas was instrumental in putting together a strategic partnership in 2019 that allowed Marvell to roll-out a product called ThunderX based on Arm’s CPUs and architecture. The deal involved an unusual incentive structure in which Arm and Marvell received warrants for Marvell stock that would vest if certain revenue targets for the ThunderX were hit. This was not the sort of conventional royalty deal Arm did, and it ultimately needed approval from Arm’s board to go through. “He uniquely impacted that deal,” Murphy says of Haas. “I’m not sure that without him, how we would have actually gotten it across the line.”

For various reasons, the ThunderX product line didn’t pay off for Marvell to the extent it had hoped, although Marvell has kept selling bespoke servers based on Arm’s IP. And overall, the success of Haas’ strategies is reflected in Arm’s financial figures. Arm went from averaging about $81.2 million per month in royalty fees in late 2016 to about $128 million per month by the end of 2021. (Licensing revenue remained relatively constant over the same period.)

Meanwhile, the other part of Arm’s new structure, the IoT software business, was foundering. The IoT market was developing far more slowly than Softbank had expected, and Arm faced stiff competition from IoT products marketed by better-known software brands, such as Google, Amazon, and Microsoft. It also was battling industrial companies like Siemens and General Electric that were creating software to support their own connected devices. Arm’s organic software sales remained essentially flat from 2016 to 2018. In 2019, Arm spent a reported $600 million to buy Treasure Data, a data management company it hoped would give it an edge in IoT services. The purchase boosted Arm’s annual software sales to $191 million, but it also added to its headcount and payroll costs.The ballooning expense of pursuing the new market, which involved adding more than 2,000 employees in total, torpedoed Arm’s profitability. The company’s EBITDA earnings declined from about $827 million the year Softbank took over, to $365 million in its 2019 fiscal year. This past fiscal year, which ran through March 2022, those same earnings, excluding discontinued operations, climbed back up to just under $1 billion.

A deal with Nvidia falls through

The lack of growth frustrated Son and the financial managers of Softbank’s $100 billion Vision Fund, which had received a 25% stake in Arm from Softbank itself in early 2017. When many of Softbank’s other investments—most notably WeWork and Uber—turned south, Son decided, his “30-year vision” for Arm notwithstanding, to sell the chip design firm.

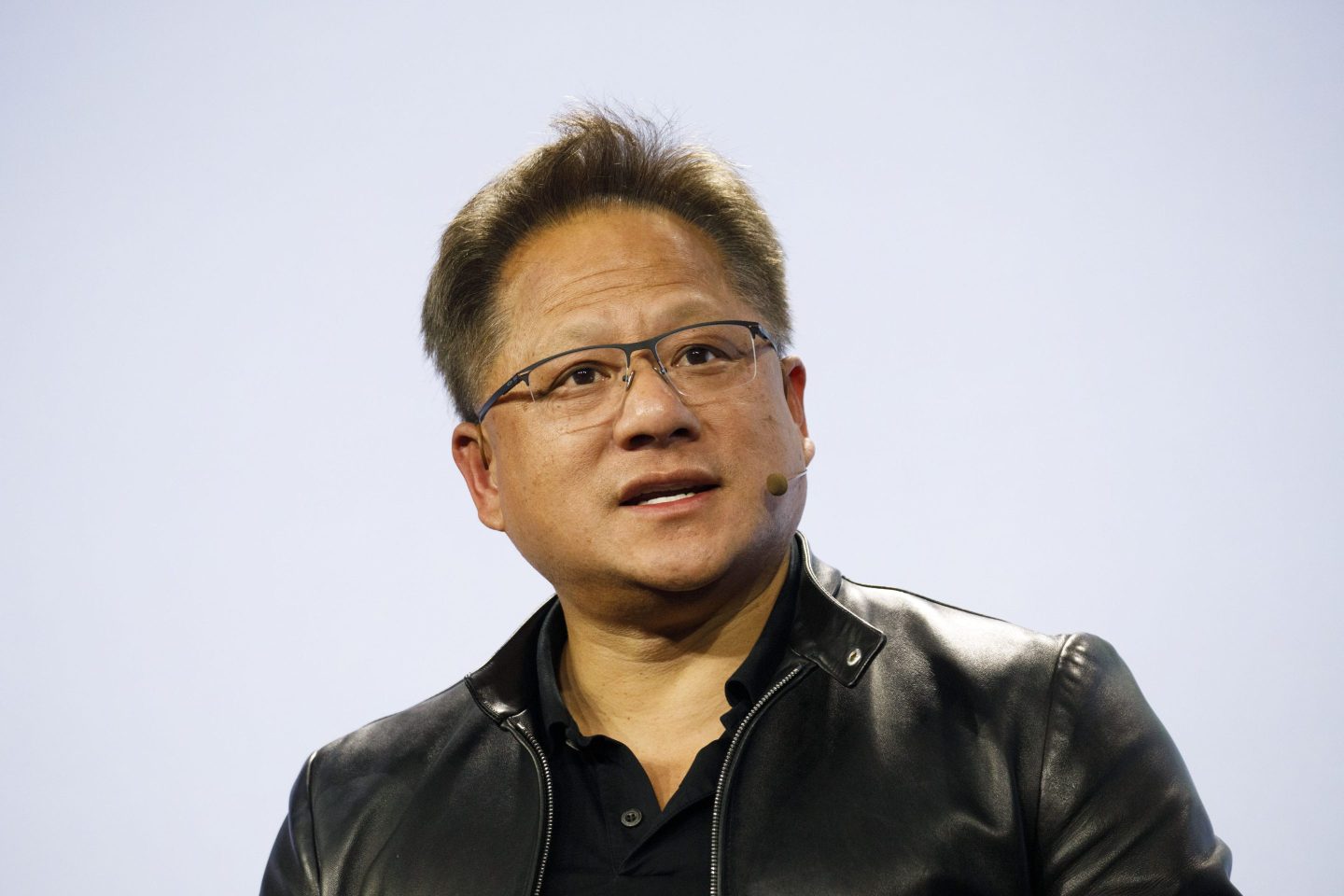

Son made a phone call to Jensen Huang. Huang is the chief executive officer of Nvidia, the Santa Clara, Calif., semiconductor company that dominates the market for graphics processing units, specialized chips that have found vast new markets in running the algorithms that power artificial intelligence and those that mine cryptocurrency. Would Nvidia like to buy Arm? Son asked.

“I responded with, ‘I would love to buy Arm and I will be the highest bidder.’ That’s it. That’s about all the negotiation there was,” Huang tells Fortune. He says he thought Arm was “a singular asset,” and that Nvidia would not get the opportunity again. Huang offered $40 billion—the highest price ever paid for an acquisition in the semiconductor industry. That represented a modest 20% gain for Son’s four years of ownership; then again, Son needed the money and Huang knew it.

The deal, however, raised immediate concerns among chipmakers and computer hardware producers, who feared Nvidia might not maintain Arm’s neutrality and would instead give itself privileged access to Arm’s future technology. “My belief is that that several companies really lobbied hard against the deal,” Huang says. “The companies were really afraid, really, for no good reason at all.” (Qualcomm, Microsoft, and Google all publicly voiced opposition to the deal.)

Despite reassurances from Huang that Arm would still license to all equally, regulators in the U.K., U.S., and the European Union were soon scrutinizing the deal—and by the summer of 2021 it was looking increasingly unlikely to pass muster. The coup de grace came in December, when the U.S. Federal Trade Commission announced that it was formally suing Nvidia to stop the takeover, arguing that “the combined firm would have the means and incentive to stifle innovative next-generation technologies.”

Haas says he thinks the deal failed for several reasons, but a key factor was that “the geopolitics just got a lot harder,” leading to far greater regulatory scrutiny than Softbank, Arm, and Nvidia had anticipated. Thanks in part to the supply chain crunch in semiconductors caused by the COVID-19 pandemic, governments around the world increasingly viewed semiconductors as a vital strategic asset—and they were worried about the risk of concentrating the vital technology in the hands of just a few companies. The U.S. and Europe also increasingly viewed computer chips as a vital weapon in a technological arms race with China.

In the face of this multi-front opposition, Son and Huang decided to cut bait. Son pivoted from trying to sell Arm to Nvidia to trying to sell a minority stake in Arm to the public, via an initial public offering. Only now he reportedly won’t be content with a mere $40 billion. He is now seeking a $60 billion valuation, according to a report in Bloomberg News that cited sources familiar with the IPO plans. That price assumes a valuation for Arm that is more than double what the average price-to-sales ratio for a semiconductor would imply. Son said earlier this week that Softbank intends to retain a majority stake in Arm following its IPO.

Even before trying to sell Arm to Nvidia, Son had proposed reabsorbing Arm’s money-sucking IoT software services business back into Softbank. When the Nvidia sale collapsed, Arm decided to dispose of the entire division, taking a $50 million impairment charge. The failure of the IoT software business may have also played a role in Segars’ decision to step down after more than eight years as CEO. And it made sense to elevate Haas, who had run the part of Arm that was actually successful, into the top job. Haas became CEO on February 8.

Basketball as a management master class

Arm’s new leader benefits from his long history in the semiconductor business. He cut his teeth in the industry in the early 2000s at Tensilica, a chip design firm, before working for seven years at Nvidia. Huang remembers Haas fondly as one of his general managers. “He’s very supportive of his teammates. He’s very strategic. And he takes punches really well,” Huang says. And Huang remembers throwing plenty of punches. The Nvidia CEO says his style is to ask tough questions of his general managers and to constantly probe and push them to improve. “He took that heat from me for many years and he just got better and better over time,” Huang says.

Haas likes basketball, both as a fan and as an amateur player— at six feet, four inches, he has the height for the sport, and he tries to find the time to polish the parquet a couple of times a week at a local gym. It’s “the ultimate team sport,” he says. “Yes, talent matters and means a great deal. But if you have five people working really together on a basketball court, it’s like magic, because people know what the other person’s thinking, they can move really, really well, they can get a lot done, without having a lot of coaching.”

He also likes basketball as management master class. He says he particularly admires Phil Jackson, the head coach of the Chicago Bulls during its golden era in the 1990s and later of the Los Angeles Lakers. The 11-time NBA championship coach, according to Haas, was not a micro-manager. When his team began to trail on the scoreboard, a situation in which other coaches would call a time out to troubleshoot, Jackson tended to demur. He wanted the players to figure it out for themselves on the court.

Haas says he tends to manage the same way: letting his deputies hash out a problem in staff meetings, often well past the point where they seem deadlocked and would prefer for him to come in and make a decision. “I need that team to work together to come up with the right answer for Arm,” he says. “I can’t arbitrate everything at that level.”

By most accounts, the new Arm boss likes his subordinates to challenge him. “He allows me to disagree with him, which I do, probably more than he appreciates,” says Vachani, the head of the automotive and IoT vertical. “I come from a different perspective. And he appreciates that perspective. I haven’t gotten fired yet for disagreeing with him.” Drew Henry, Arm’s senior vice president of strategy and operations, says Haas is humble enough to listen to others’ opinions—to a point. “He’s also decisive enough to know when to say, ‘okay, we’re done. We’re going this way,’” Henry says.

The risks of going public

The biggest problem Haas now faces is that once Arm becomes a public company—especially one asking for an expensive valuation—shareholders are likely to expect consistent revenue and profit growth. But analysts say it isn’t easy for Arm to ratchet up either sales or earnings. New chip designs take months and years to come to fruition. License and royalty revenues ramp up often over years. And Arm has relatively limited pricing power, since its IP is usually only a small fraction of the “value” of a circuit board, amounting to maybe $50 in a specialized chip that might cost thousands for a datacenter. “You can’t just twiddle the knobs to drive up revenue,” Alan Priestly, a senior analyst at technology research firm Gartner, says.

The biggest new opportunity for Arm may lay in datacenters. Intel long dominated the datacenter market. As recently as 2017, the company had a 98% share of that market. But since then, other firms have caught up to Intel’s speed and reliability, and its market share has since fallen to 77%, according to tech research firm Omdia.

The greatest beneficiary of Intel’s decline has been AMD, which still uses Intel’s x86 architecture. But the x86 architecture has a big drawback: it is not designed to minimize power consumption. That’s where Arm has a big potential advantage. The move towards carbon neutrality and “net zero,” has been a help. But more than that, says Chris Bergey, the senior vice president and general manager of Arm’s infrastructure business, power consumption has become a major concern for the large datacenters built by the likes of Amazon and Microsoft. Those companies simply can’t get any more megawatts of power into any given server-farm building. If each rack of servers can only consume, say, 25 kilowatt hours of electricity, and Arm is able to provide more compute—literally do more stuff—for that same 25 kilowatts, that means more money for the datacenter owner, and Arm starts to look very attractive, Bergey says.

Among Arm’s biggest datacenter wins to date have been Amazon’s Graviton processors, which the huge AWS cloud operation uses. Graviton chips use Arm processors, alongside hardware Amazon itself created, and they run on Arm’s architecture. Amazon claims Graviton can provide up to 40% improved performance for certain computer workloads. And the company says that 48 of its top 50 customers have now switched to using Graviton. “That’s a pretty strong performance point,” Bergey says. “We think we’ve got a lot of momentum. We are really just starting to see the traction and we don’t think there’s any reason why it’s going to stop.” Another datapoint: Nvidia, which has long dominated the market for specialized chips for processing graphics and running artificial intelligence, has just launched its first general CPU product aimed at datacenter customers, and it is based on Arm’s architecture.

But Priestly, the Gartner analyst, questions whether strong datacenter growth will be enough to make Arm a stock market darling. Unlike Arm’s traditional sweet spot of smartphones, he says, data centers don’t require vast volumes of chips—the kind of numbers needed to significantly advance Arm’s royalty revenues. There are only about 12 to 14 million servers shipped per year, Priestly says. The personal computing market is larger, but still in in the low hundreds of millions of devices shipped per year. “These high value markets don’t go to billions,” he says.

Another issue is the amount it costs for Arm to stay at the leading edge of chip design. The company has always spent heavily on research and development. During Softbank’s ownership, that amount climbed 53%, to $887 million per year, a figure that now amounts to 32% of Arm’s revenues. But there are doubts about whether Arm can keep this up as a public company while delivering the short-term earnings investors demand. Priestly notes that Arm is up against much larger competitors, such as Intel and AMD, that are not sitting still—the company will need to keep spending at pace or risk the gains it has made in areas such as datacenter chips.

Haas says he’s confident that R&D spending—which he calls “table stakes” for any company in technology—will be sufficient to keep Arm at the forefront of chip innovation. But he has already had to try to cut costs, including in R&D, to prep Arm for an IPO. In March, he announced the company was laying off almost 15% of its workforce, with some 1,000 jobs being eliminated. Among those facing the ax were Arm engineers who worked on long-term R&D projects and exotic new chip architectures. Haas says the move was necessary, in part because Arm had built an employee base to support the now discontinued IoT business. But he also acknowledges that the layoffs are “about getting the cost structure in line” for the IPO.

Huang says that if he were Arm, the answer to this dilemma would be obvious: raise prices. As a public company, Arm will need to keep shareholders happy, while having a high-performing stock that can help attract talented employees, who are often rewarded with shares. As a result, Huang predicts once Arm goes public, he and every other Arm customer will have to pay more to access its tech. “I expect that,” he says. “I expect that and I think it is good for them.” He says Nvidia would be willing to pay more, he says, because Arm is such a key part of the semiconductor ecosystem. “If we had anything close to a mature and a long-term view, we would encourage Arm to have a good business model,” Huang says.

If Arm were to ramp up its prices too much, it could become more vulnerable a different threat. RISC-V, created in 2010 by a group of researchers at the University of California Berkeley, is a simplified computer code similar to Arm’s architecture, but it is open-source, meaning that it is free to use. RISC-V has managed to accomplish some impressive technological feats: A microprocessor using the architecture and designed by Micro Magic, a California-based chip design boutique, recently set a speed record—running at 5 gigahertz—while running with more energy efficiency than comparable chips from Intel and Samsung.

The Nvidia purchase of Arm drove a big surge of interest in RISC-V. In 2021, while the deal was being mooted, membership in the organization that helps oversee RISC-V’s open-source architecture soared 130% to almost 2,500. RISC-V has only about 1% market share globally. But Priestly, the Gartner analyst, says RISC-V is particularly attractive for those building lower-end, lower-cost chips, where Arm’s licensing and royalty payments represent a larger share of the total price.

Haas is dismissive of the risk from RISC-V. “We’ve seen over the years, various attempts to steal Arm’s crown,” he says. “And they really fail because of the sheer lack of computability.” He notes that there is far more software that runs on Arm’s architecture than on rivals’, and that Arm constantly invests in rolling out more. RISC-V user, he says, have far less to lean on. Still, the technology has an allure: It’s hard to argue with fast and free.

Complicated relationships

Haas has other headaches to resolve before Arm’s eventual IPO. Among them is a struggle over the company’s China business, a joint venture that both creates its own chip designs and sells Arm’s IP, and accounts for a fifth of Arm’s global revenues. Arm China’s former chief executive, Allen Wu, has resisted the company’s efforts to oust him; he has been able to protract the dispute by refusing to surrender the company’s “chop,” the official seal that gives an individual the legal right to act on a company’s behalf in China and, at one point, hiring security guards to prevent a new management team Arm China’s board appointed from accessing Arm China’s offices. After two years of legal wrangling, Arm China succeeded earlier this month in getting a new chop issued to a new CEO. And to prevent the uncertainty over the China business from undermining Arm’s public offering, Arm effectively transferred most of its ownership stake in Arm China to a new joint venture jointly run by Softbank.

That solution underscores a key point: Among the most complicated relationships Haas will have to navigate is the one with Softbank’s Son. Not only is Son driving for a sky-high valuation in an Arm IPO; even after the stock offering, Softbank is expected to remain a major shareholder. And Son has a reputation for being a tough boss, impatient for his investments to hit targets that some of his portfolio executives have complained are unrealistic.

Haas says he has a good rapport with Son, although he does acknowledge the Japanese tycoon “will always take anything you projected forward and challenge you to be bigger and challenge you to be bolder.” Haas recalls the day, shortly after Softbank bought Arm, that he saw Son present to Arm’s executive leadership at Softbank’s offices in San Carlos, California. That was the day that Haas felt Arm’s understated, British-influenced culture truly collided with the Silicon Valley ethos that Haas and Son share. “We were a FTSE-traded company being very, very careful and cautious,” Haas recalls. “Now here’s Masa being massively animated, massively passionate. He has big dreams, big visions.”

For instance, Son forced Arm’s executive team to produce financial projections for the business 10 years out. The request freaked out some long-time Arm execs, Haas says. “But [Son’s] idea around it was not, ‘I want to see a precise number in the outer years,’ but ‘I want you to think about what the future could look like in the outer years.’ And that really does stretch your mind suddenly.” Haas says he found the exercise “liberating.”

Haas says he currently speaks to Son a few times a week. Some of that discussion is undoubtedly around the upcoming IPO, which Haas says Son sees “as a mile marker.” As for reports that Son is pushing bankers to take Arm public at a valuation far higher than what any semiconductor company has ever commanded before, Haas says Arm’s business has a lot more in common with today’s more profitable software business models, based on recurring subscription revenue, than it does a traditional computer hardware business.

Haas also says many equity analysts don’t realize how much Arm has changed since it was last a public company, in the pre-Softbank days. “I don’t think they know the Arm of 2022 that well yet,” he says. Haas’s job now depends on re-educating them.

Sign up for the Fortune Features email list so you don’t miss our biggest features, exclusive interviews, and investigations.