Good morning,

“Whether you’re talking about physical capital or human capital, under-investing might lead to great-looking results over a very short period, but they’re not sustainable over time.”

That’s what Target EVP and CFO Michael Fiddelke said during the retailer’s annual investors meeting on Tuesday. Target intends to focus on long-term investments for profitable growth, Fiddelke said. “First on that list—continued investments in pay and benefits to support our team,” he said.

In 2021, Target delivered $106 billion in total revenue, having grown nearly $28 billion, or more than 35% over the past two years, according to its Q4 earnings report released on Tuesday. Total sales have grown more than $27 billion since 2019, reflecting more than $14 billion of additional store sales and digital sales growth of nearly $13 billion.

Fiddelke became CFO in 2019 but has been with Target for more than 15 years. He has served in various roles across finance, merchandising, operations, and human resources, including VP of pay and benefits. During the investors’ meeting, he emphasized a focus on talent.

“I want to highlight the enormous benefit we’ve realized from the investments we’ve been making in our team,” Fiddelke said. “These investments have driven positive change to the lives of hundreds of thousands of team members, offering more steady income, pathways to career growth and education and access to benefits that meet their evolving needs.”

Target is increasing its wages to retain and attract employees in the war for talent. Leadership announced on Monday the company is investing up to $300 million more to set a new starting wage range and expand access to health care benefits. Target is setting a new starting wage range from $15 to $24 for hourly team members. The exact starting wage within the range will depend on the job and the local market, the company said.

But for some employees, the announcement hasn’t brought a sense of security. “They’re not stipulating how many of us are actually going to get paid $24 an hour, and I’m at $16 an hour,” says Adam Ryan, a Target team member who has worked at the Christiansburg, Va. store since May 2017. Ryan is one of the organizers of Target Workers Unite, an independent initiative ran by team members advocating for a union.

“I’m in the South, and wages generally are going to be lower in the South,” Ryan told me. “So, it would be nice to hear who exactly is going to get that $24 an hour.” He continued, “I definitely think a pay increase is justified. But I would say, it needs to be $24 as an hourly base pay rate for everybody at this point, especially with cost-of-living, inflation, how unstable the markets are right now, and the supply chain issues.”

I contacted Target for a statement regarding Ryan’s comments. A spokesperson referred me to the company’s website. It states, “We know that the pay and benefits we provide play a huge role in improving team members’ well-being. That’s why Target’s always listening to our team and why we’ll continue to make adjustments to better meet their needs at all stages of life.”

To drive continued growth in 2022, Target will invest in its physical stores, digital experiences, fulfillment capabilities and supply chain capacity. The company plans to open approximately 30 stores.

“Over time, our updated long-term algorithm anticipates mid-single digit annual growth in both total revenue and operating income, high single digit annual growth in adjusted EPS [earnings per share], annual CapEx [capital expenditures] of $4 to $5 billion, after tax ROIC [return on invested capital] in the high 20% to 30% range,” Fiddelke said.

Before ending his remarks on Tuesday, Fiddelke said the following: “I want to pause and express my gratitude to our team, many of whom are listening into this meeting today. You have delivered industry leading results over the last couple of years, while taking care of our guests and each other. And importantly, during that time, you’ve made Target a much stronger company.”

See you tomorrow.

Sheryl Estrada

sheryl.estrada@fortune.com

Big deal

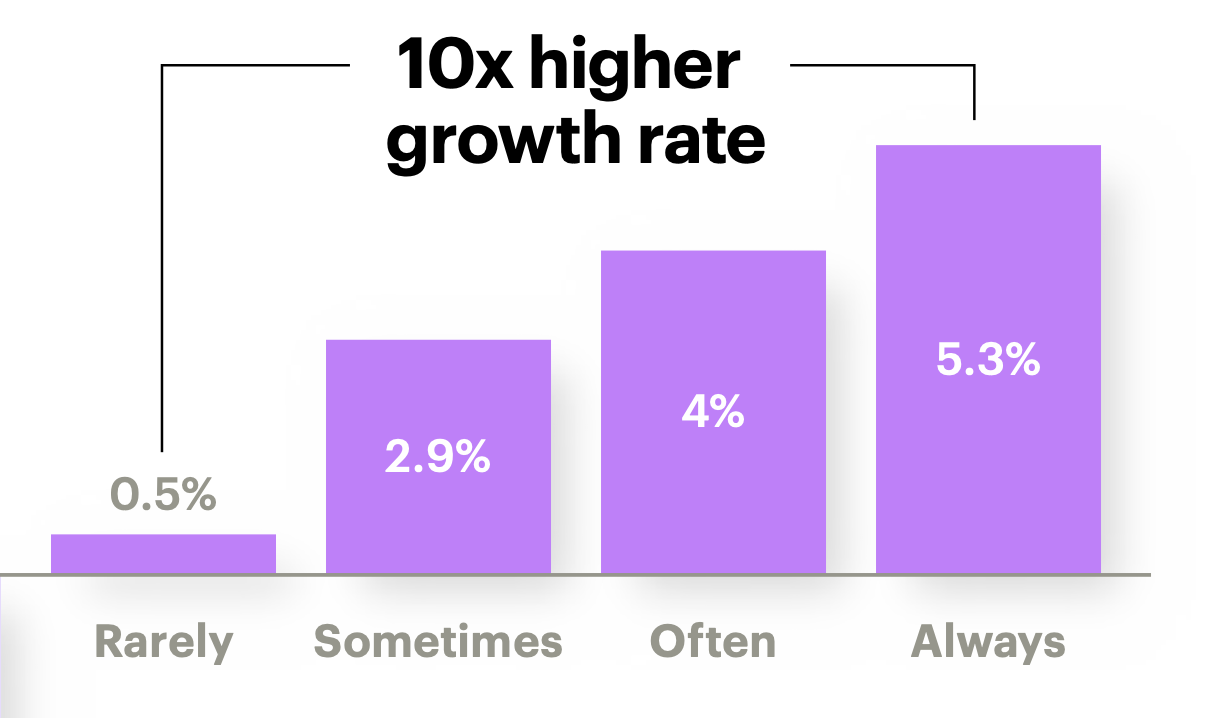

Companies that view customer service as a value center, rather than as a cost center, are more profitable, according to a new Accenture report. In End-to-Endless Customer Service, about 60% of businesses surveyed involve customer service in product development. These same companies also experience higher revenue growth. Companies that report always involving their service organization in new product development are achieving up to 10 times the revenue growth than companies that keep these functions separate. The findings include the sentiment of more than 2,000 executives with customer service responsibilities, surveyed alongside 16,700 consumers and business customers in 13 countries and 14 industries, according to Accenture.

Going deeper

A new report by global advisory WTW (Willis Towers Watson, Nasdaq: WTW) found many U.S. workers feel their employers have kept them safe and supported them during the pandemic. For example, 70% of respondents said employers have been prioritizing safety measures. More than half (58%) of employees support employer vaccinate mandates. The findings are based on a survey of more than 9,600 employees.

Leaderboard

Thomas Etergino was named CFO at 1stDibs (Nasdaq: DIBS), an e-commerce company that sells luxury items. Etergino will succeed Tu Nguyen, who has served as the company’s CFO for the last two years and will be taking on a new role outside of the company. Etergino will join the company later this month. He joins 1stDibs from Vesta Healthcare, where he served as CFO for the past five years. Previously, he held public company CFO positions at AtriCure and The Street, and at several private equity and venture-backed entities including Refinery29. He also previously served as chief accounting officer and treasurer of DoubleClick.

Jennifer Thresher was named CFO at Emtrain, which provides eLearning and analytics. Thresher brings more than 12 years of financial leadership experience to Emtrain. Prior to joining Emtrain, she served as VP of finance and head of human resources at Apex Learning Inc.

Overheard

"Just last year, 55 Fortune 500 corporations earned $40 billion in profits and paid zero dollars in federal income tax,” Biden said during his address. “That’s simply not fair."

—President Joe Biden said during his first State of the Union address on Tuesday. Biden highlighted his plan to levy a 15% minimum tax on global corporations. Last year, Fortune reported that 55 of the companies on the Fortune 500, which ranks the 500 largest corporations in the U.S. by total revenue, paid zero federal income tax for the year. This was mostly due to exploiting a difference between so-called book income and tax income.

This is the web version of CFO Daily, a newsletter on the trends and individuals shaping corporate finance. Sign up to get it delivered free to your inbox.