Ever had the experience of seeing that the temperature is 40 degrees, but then you step outside and the ‘real feel’ is more like 20?

Well, something similar is going on in the economy, specifically with inflation. Currently only slightly above the Federal Reserve’s target 2% level, the inflation rate remains at historical lows. Stories of the double-digit annual inflation of the 1970s and 1980s that made buying a home or filling a gas tank painful seem almost apocryphal.

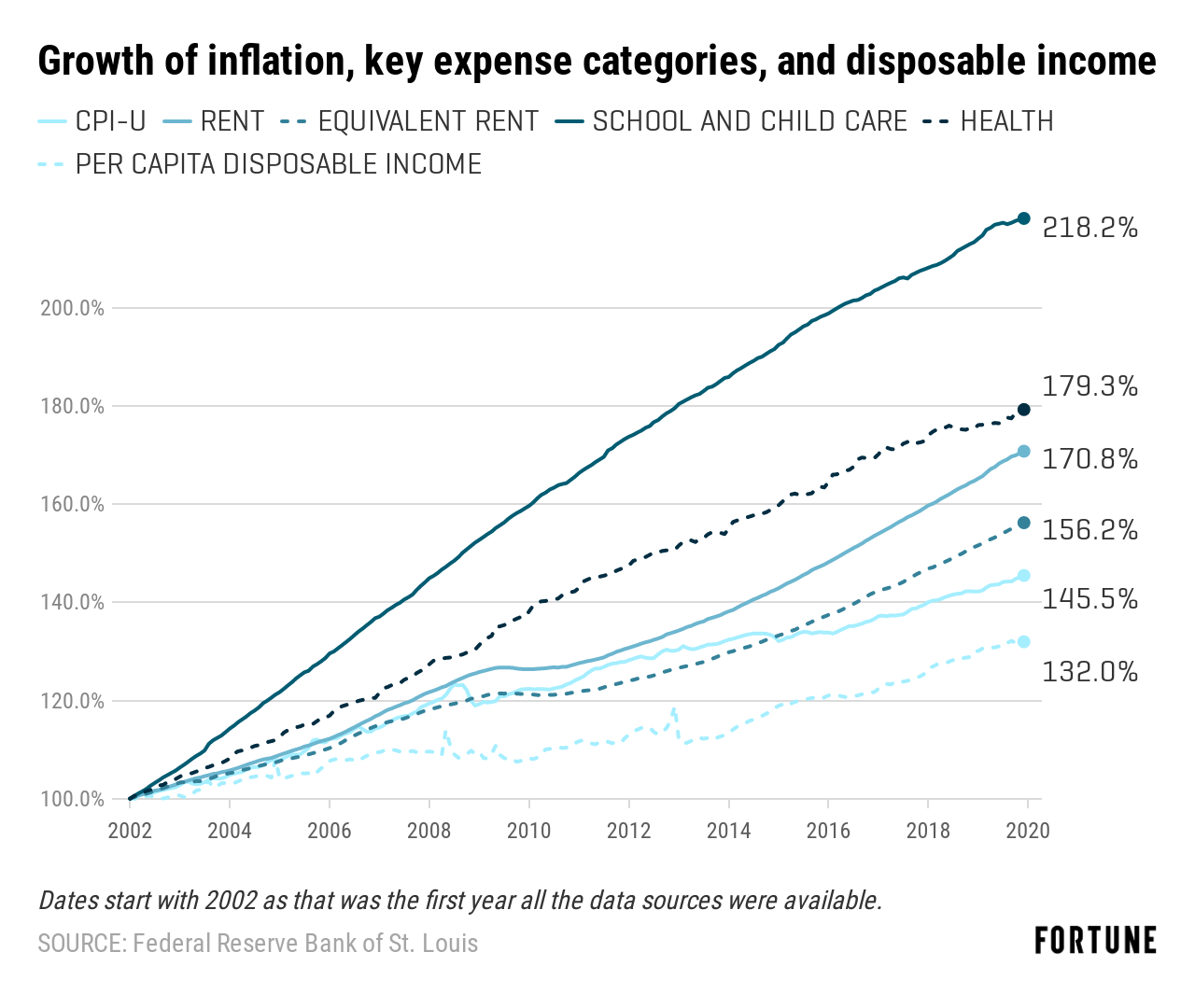

But a Fortune analysis of inflation data and price changes in critical areas vital to consumers suggests that, for many, rising prices in a variety of categories are making everything from rent to college and healthcare seem out of reach for many consumers. A recent Bankrate survey showed that 57% of U.S. adults did not expect their personal financial situation to improve this year.

So why the disconnect?

To dig deeper, you have to look at how inflation is calculated. And what the government measures, versus what the average person paying for housing, healthcare, school and childcare (categories that have grown anywhere from 18% to 65% faster than disposable income) experiences, are two very different things.

First, a bit of background. Inflation is the measure of how prices and wages grow over time. The faster they rise, the higher the level of inflation. To determine the general inflation rate—known as the CPI-U, or consumer price index for all urban consumers—the government tracks the cost of a market basket of goods and services, based on surveys of what consumers buy at any given time.

“The majority of that basket is going to be housing expenses” like mortgage or rent, food, and clothing, said Rebecca Neumann, an economics professor at the University of Wisconsin-Milwaukee. Other parts include such items as childcare, transportation costs, college, and health care.

The CPI-U is a complex composite. Some prices change more slowly and others, far quicker. The graph below compares the percentage growth rates of housing (both rent and a rent-equivalent for home owners), school and childcare, health, CPI-U, and per capita disposable income (average income after taxes across all people).

Economists, government officials, public policy advocates, investors, and businesses often discuss the CPI-U as a single measure of inflation—and for good reasons, as it is a way of discussing average changes in the overall economy. But there is a serious limitation. The calculated number doesn’t apply evenly across all categories of goods and services, in all places, or for all people.

“We’re not back in the 70s where you see pricing increases every day,” said Neumann. “But we have this steady [trend of] prices going up, and more in some categories than another.”

As the graph shows, the price increases in some of the most critical categories of expenses quickly outstrip inflation and, more so, the rate at which average disposable income grows. In addition, disposable income is not distributed evenly across the population; those who have lower take home pay will see an even bigger gap between income and expenses.

Individual inflation

While inflation is frequently treated as a hard and fast number, your ‘personal’ rate of inflation can vary greatly depending on which goods and services you’re spending your money on and where you live.

Part of an individual rate depends on location. Even one measure, like the CPI-U, doesn’t apply accurately across all geographic regions and demographics. The Bureau of Labor Statistics has a list of CPIs for different states as well as specific cities. Someone in a rural area may find different inflation rates because their likely market basket won’t completely match that of an urban dweller.

Where people are in their lives also has a big impact as types of incurred expenses can change. Someone dealing with college costs, daycare for young kids, or a health crisis will have a higher personal inflation rate because those fast-rising categories now have a heavier personal impact than the CPI-U would show.

There are also technical aspects of defining inflation that can make a general number virtually meaningless for many. The CPI-U is only one of three consumer price index versions. There is a CPI-W for urban wage earners and clerical workers. Both depend on survey data that is two to three years old.

The third is the C-CPI-U, or chained CPI for all urban consumers. It incorporates more recent information and also looks at relative prices and substitution of one good for another.

“You substitute other things you wouldn’t have bought when prices were different,” like maybe buying cheaper brands of clothing or swapping a chicken quarter for a steak, said Chester Spatt, a professor of finance at the Tepper School of Business at Carnegie Mellon University.

Substitution lets people decrease what they spend so the C-CPI-U inflation rate is lower than the CPI-U. The difference between the two measures of inflation has lead some politicians to support use of C-CPI-U when calculating automatic changes in government programs. The switch lowers government expenses.

For example, the 2017 tax overhaul changed how the IRS calculates automatic increases in tax brackets due to inflation. As goods and services get more expensive, a dollar doesn’t go as far as it once did. Brackets become higher to take that into account.

Adjustments used to be based on CPI-U. Now they use C-CPI-U, which is smaller so brackets grow more slowly. A greater portion of someone’s income can fall into higher brackets than would have been true using CPI-U, meaning more taxes are due.

There are also inconsistencies between economic theory and individual lives. Over time, CPI measurements have increased focus on the quality of goods and services.

“The quality of most goods, like technology goods, has improved,” said Steven Sheffrin, a professor of economics and affiliated professor of law at Tulane University. The differences in capabilities between a laptop computer or smartphone from the mid-2000s and 2020 are substantial. “If the good today is better and the price is the same, the good is actually cheaper,” he said.

But a word processor or browser might show no improvement that is obvious to the owner. This year’s model of smartphone likely has a better camera than one from two years ago, but you still pay today’s prices even if you can’t see, or don’t care, about the difference. From the consumer’s viewpoint, the product may not seem any cheaper.

The upshot of individual inflation and madly racing price growth in key areas is that personal finances become even more of a challenge.

How does a family plan for college costs when they can’t predict the gap between what they can save, the increase in prices, and the amount a school’s financial aid department expects as a contribution? How can an individual deal with an unexpected illness that far surpasses the support health insurance offers?

Those are equations that no government metric seems to be able to accurately solve.

More must-read stories from Fortune:

—All of your questions on filing taxes in 2020, answered

—The health of the economy in nine charts

—Global companies enter lockdown mode as coronavirus rocks China

—Bull market advice for investing in today’s market

—WATCH: Biggest investing opportunities and risks for 2020

Subscribe to Fortune’s Bull Sheet for no-nonsense finance news and analysis daily.