Last week, the S&P 500 charged to the 109th record high of the current bull market, now in it’s seventh year.

But the steady upward march of stock prices hasn’t calmed the skepticism of some investors, who have pointed to uncertainty in geopolitics, relatively sluggish economic growth, and unprecedented central bank stimulus as reasons why we shouldn’t assume that rising stock prices means that everything’s a-okay with the economy.

But a recent spate of big-bank earnings releases give us reason doubt the haters. If you look at the financials of four of the largest American banks, Wells Fargo, JPMorgan Chase, Citigroup, and Bank of America, they all show higher lending today than three months ago.

This is hugely important for the continued health of the U.S. economy, as there is a strong correlation between growth in bank lending and economic growth. In fact, one can argue that changes in lending by private banks is more important to the real economy than policy changes at the Federal Reserve. That’s because all Federal Reserve policy works through big banks before it makes it way to the broader economy.

Take for instance, the aggregate lending growth by the four largest banks from March through June. Collectively, they added close to $53 billion in new money to the economy, or more than the Federal Reserve was buying in government bonds per month at the height of its quantitative easing program. The difference, of course, is when the Fed was buying huge amount of government bonds from the banks, there was no guarantee that this money would find its way into the hands of the broad public. When big banks lend, on the other hand, that money is going to real people and business and is getting spent in the real economy.

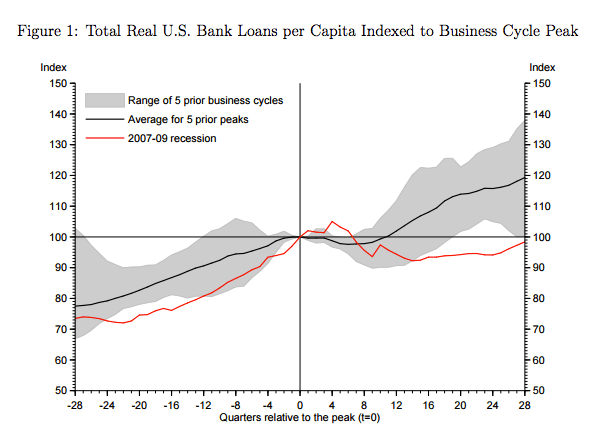

In fact, weak bank lending is one reason economists believe the recovery following the Great Recession was so weak. The following chart, from a recent working paper by economists at the Hoover Institution, shows the difference in bank lending habits following the Great Recession compared with those following other recessions:

The authors of the paper argue that increased regulatory burden caused by Dodd-Frank reforms is at least partially to blame for muted bank lending following the recession. But this dynamic is also the reason given by many economists, including former Fed Chair Ben Bernanke, for defending the hugely unpopular Troubled Asset Relief Program, popularly known as the bank bailouts. If the banks weren’t bailed out, and thus were unable to continue to lend money to keep the economy growing, the U.S. economy would have been sent into a downward spiral much like that which we saw during the Great Depression.

So fret all you want about the coming U.S. recession, but as long as we continue to see big banks lending more, it’s likely not right around the corner.