Are you feeling a little underwhelmed by AI’s transformation of the economy? The so-called “fifth industrial revolution” is supposed to wipe out half or even all of white-collar work and yet adoption is kind of begrudging, even optional for many workers. For those who have started using it, it kind of feels like homework a lot of the time—it writes your emails for you, but it’s still wrong a lot of the time. Three and four decades ago, the computer revolution was similarly hyped, and yet for a lot of the time, it looked more like Pets.com than what turned into the iPhone.

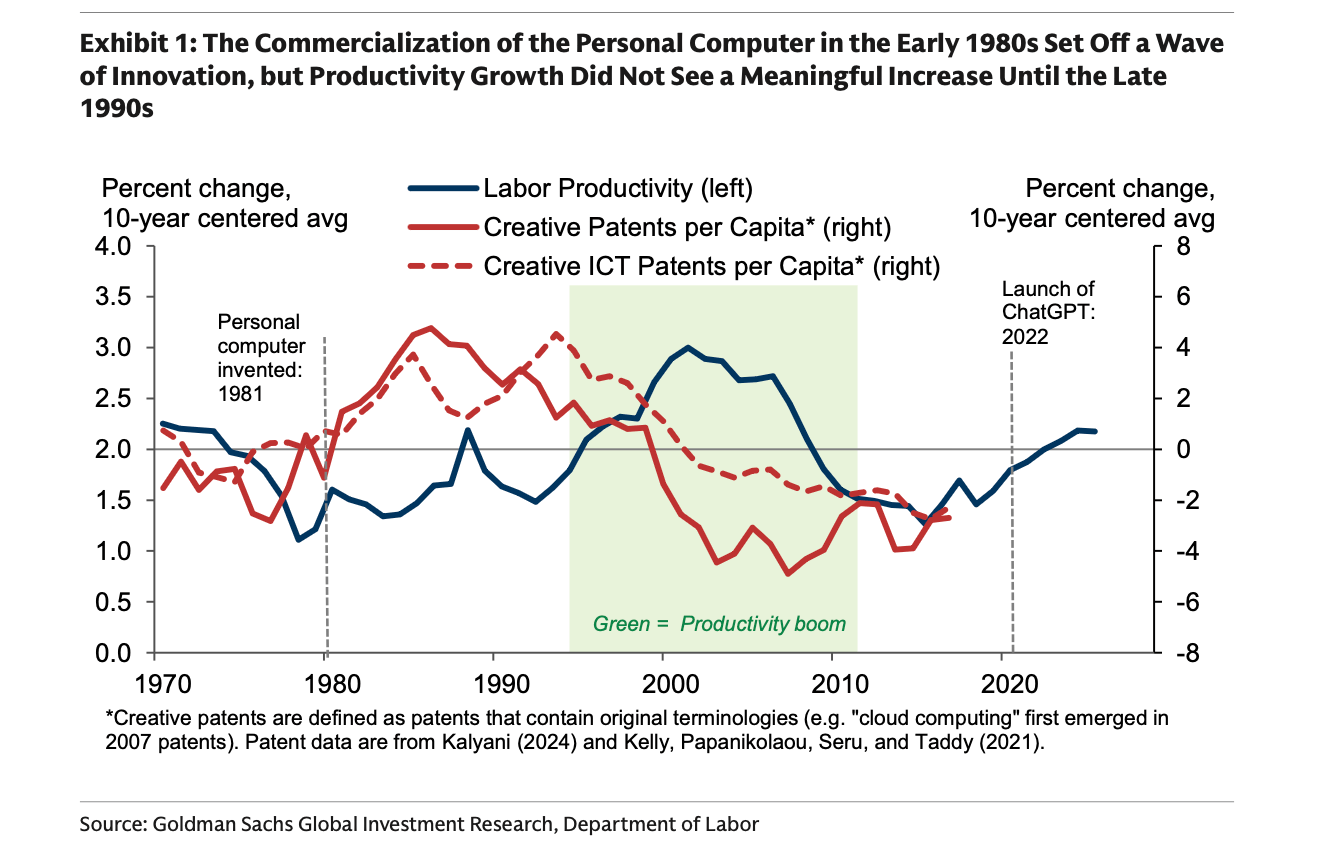

That’s the angle taken by Goldman Sachs’ Elsie Peng, who looked closely at the productivity uptick from the computing revolution in a research note for the bank earlier this month. The last time something this big came along, she wrote, things actually got measurably worse before they got better—for four years, by her reckoning. Then they flatlined for another four. Only in year eight did gains from computing become statistically significant. The productivity boom everyone associates with the personal computer didn’t actually show up in the macro data until 15 years after the PC was commercialized.

Goldman’s official view is still that AI will “meaningfully boost productivity growth over the next decade.” What Peng is arguing is that the AI boom’s boosters — and a lot of investors pricing that boom into equities — may be badly miscalibrated on timing. And the reason why, she finds, has less to do with the technology than with the humans being asked to use it.

The J-curve nobody mentions

The PC was commercialized in 1981. By the early 1980s, investment in information and communications technology was rising sharply across most industries. And yet the productivity trend was flat until the late 1990s.

Peng’s industry-panel analysis finds that the productivity impact followed what she calls a J-curve: a modest drag for the first four years, statistically significant gains only after eight, and a peak impact of roughly 0.6 percentage points in year 12. If ChatGPT’s 2022 launch is the equivalent of the PC’s 1981 debut, that J-curve puts the productivity payoff arriving around 2030 at the earliest, and peaking around 2034.

Three forces created the lag the first time. Key components such as semiconductors and telecom equipment remained expensive throughout the 1980s, only falling after regulatory interventions and increased competition opened previously concentrated markets in the 1990s. Many applications—especially the internet—generated value only after adoption reached a critical mass, which took years. But the biggest bottleneck was something less visible: the massive reorganization effort required to actually use the technology.

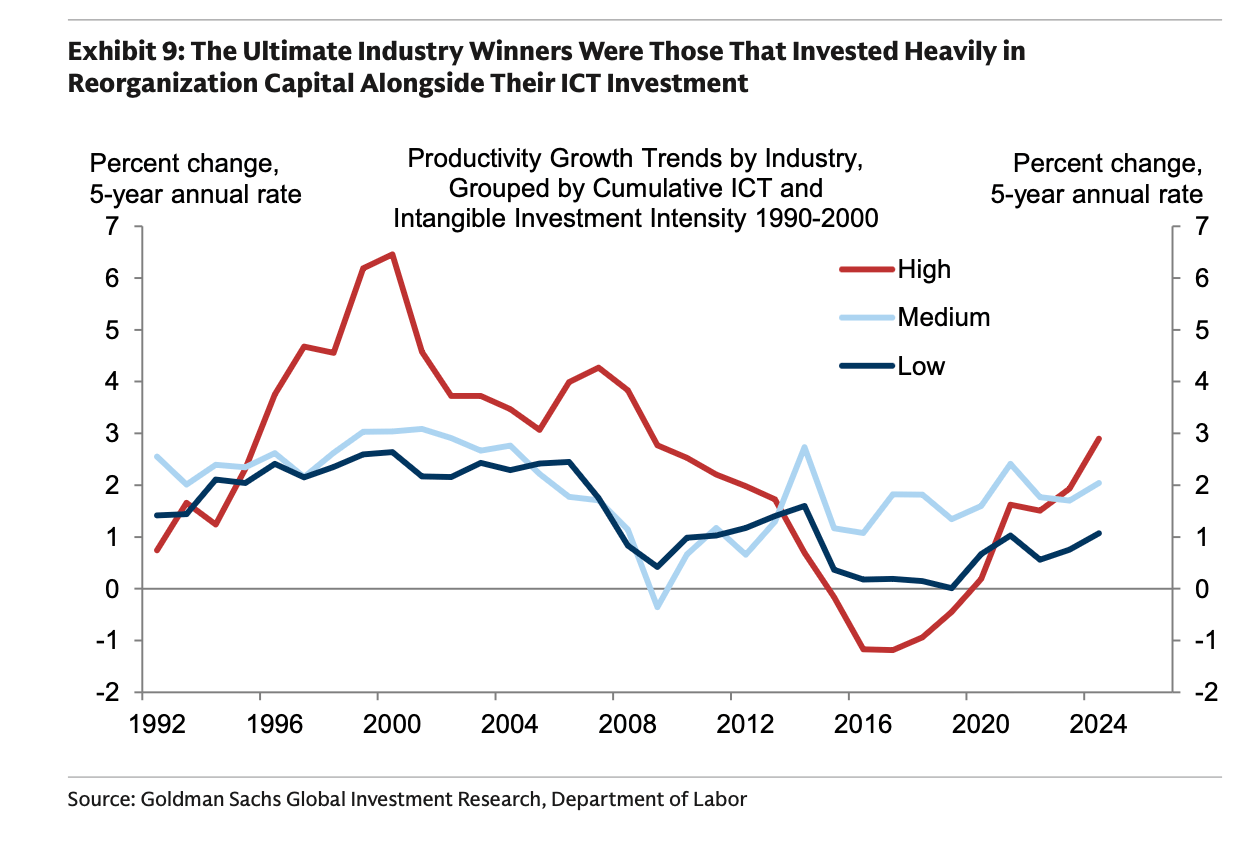

Goldman estimates that each dollar of ICT hardware investment required at least $1.70 of complementary “intangible” investment—software, data systems, and the hardest category to measure, organizational overhaul. Critically, that reorganization spending didn’t ramp up until the mid-1990s, a full decade after PCs hit desks. The industries that ultimately got the most out of ICT weren’t those that adopted earliest or spent the most on hardware, but the ones that invested most heavily in redesigning how work actually happened.

The gap is repeating—and the people problem is worse

Here’s where the historical parallel bites. Goldman’s data shows that AI hardware investment is already rising faster than the ICT buildout did at the equivalent stage. That’s the good news for the bulls. The bad news: investment in reorganizing work processes appears to be moving more slowly than it did in the 1990s ICT cycle. Goldman acknowledges that some of that spending may not be captured in official statistics—an Atlanta Fed survey implies roughly $280 billion in AI-related intangible spending in 2026—but even accounting for measurement gaps, the reorganization side of the ledger is lagging the hardware side by a wider margin than last time.

The workforce seems to be voting with their feet on this reorganization that may someday lead to the AI productivity promised land: they’re resisting.

An April survey of 2,400 knowledge workers by AI firm Writer and Workplace Intelligence—both firms with commercial stakes in AI adoption, so take the numbers with appropriate skepticism — found 29% of employees admit to actively sabotaging their company’s AI strategy. Among Gen Z workers, that figure was 44%, up from 41% a year earlier. A separate WalkMe survey of executives and employees across 14 countries, conducted the same month, found that more than 54% of workers had bypassed their company’s AI tools in the past 30 days to do the work manually instead. The survey commissioners found that a “Fear of Becoming Obsolete” is driving much of this active and passive, and even passive aggressive resistance. Similarly, The Economist reported that AI usage among U.S. workers, after an early spike, actually dipped as initial enthusiasm faded.

Harvard Business School researchers have documented a phenomenon they call “symbolic adoption“: rather than openly refusing AI tools—which brings on a risk of getting fired—employees comply on the surface while quietly undermining the technology behind the scenes. The motive isn’t mysterious. Among self-described AI saboteurs in the Writer survey, 30% say they don’t want AI to take their job; 26% say the technology has diminished their sense of value or creativity at work. Those aren’t irrational responses, given that 69% of executives in the same survey say their companies are already conducting AI-related layoffs.

What the data already shows

In my own reporting on AI’s labor market effects, I’ve watched this dynamic play out in the numbers. Stanford’s Erik Brynjolfsson and ADP Research have begun tracking 4.6 million workers across more than 730 occupations through the Canaries Dashboard. What they find isn’t a calm aggregate labor market. It’s employment for workers aged 22 to 25 in AI-exposed occupations shrinking more than 4% annually, invisible at the headline level and only visible once you cut by age and task exposure.

Goldman’s sector rankings suggest information, professional services, insurance, and finance are best positioned for early productivity gains—the same white-collar industries where the sabotage surveys find the highest rates of resistance. If the reorganization lag is being compounded by organized friction rather than just cost and complexity, the 8-to-12-year timeline Goldman extracted from the ICT era may turn out to be optimistic.

That pattern is consistent with the J-curve that Peng identified. In the early phase, technology disrupts faster than it creates. Productivity gains are suppressed not because the technology doesn’t work, but because the humans haven’t reorganized around it—and in this cycle, a meaningful share of them are actively resisting.

The Economist didn’t report that AI usage dipped because the tools got worse. It dipped because adoption is hard, and adoption of technology that workers associate with their own displacement is harder still. To that point, experts in neuroscience and AI think that the difficulty of old dogs learning new tricks is significantly underappreciated. Joshua Wöhle, the CEO of Mindstone, a firm that provides AI upskilling services and retraining services, previously told Fortune that in his experience, “most people hate learning. They’d avoid it if they can.” Similarly, the neuroscientist Vivienne Ming has talked to Fortune about how she sees a difference between “well-posed and ill-posed problems,” and most education and work is unfortunately geared toward the former.

This particular ill-posed problem could be a very big problem for financial markets, Apollo Global Management Chief Economist Torsten Slok has been arguing, since AI “has been the one thing holding up both the economy and markets.” With so much money riding on so few names, he wrote earlier this month on his Daily Spark blog, “a slower payoff wouldn’t just be a sector problem, it would risk tipping the economy into recession and the S&P 500 into a correction.”

What Goldman is actually saying

To be sure, Goldman is not saying that AI is a mirage. The micro-level productivity gains from AI in specific applications are well-documented. The question is when and whether they show up in the macro data—the kind of broad-based productivity acceleration that would justify current equity valuations and the scale of infrastructure investment underway.

The historical record says: later than you think. The human resistance data says: probably later than Goldman’s own model assumed. And the reorganization gap says: the bottleneck isn’t the hardware, it never was. It’s the messy, expensive, politically fraught work of getting organizations and the people in them to actually change how they work.

That’s what took a decade the last time. There’s no obvious reason to expect it to happen faster, and some evidence it may happen slower.