- America’s national debt has topped $38 trillion, and economists warn it could reach $39 trillion within months as borrowing accelerates. The bigger concern is the debt-to-GDP ratio, projected by the CBO to hit 156% by 2055, reflecting spending that far outpaces growth. In a statement to Fortune, Maya MacGuineas of the Committee for a Responsible Federal Budget called the milestone “appalling,” criticizing Washington for ignoring the crisis. Michael Peterson of the Peter G. Peterson Foundation warned that “budgeting-by-crisis” is unsustainable. President Trump has suggested unconventional fixes—like selling “Gold Cards” to wealthy immigrants—which economists have labeled peculiar but a step in the right direction.

America’s debt burden has hit $38 trillion. In fact, at the time of writing, it is $19 billion over that mark. Economists are warning that spectators won’t have to wait long until debt hits the $39 trillion mark as the rate of debt accumulation is increasing with every passing day.

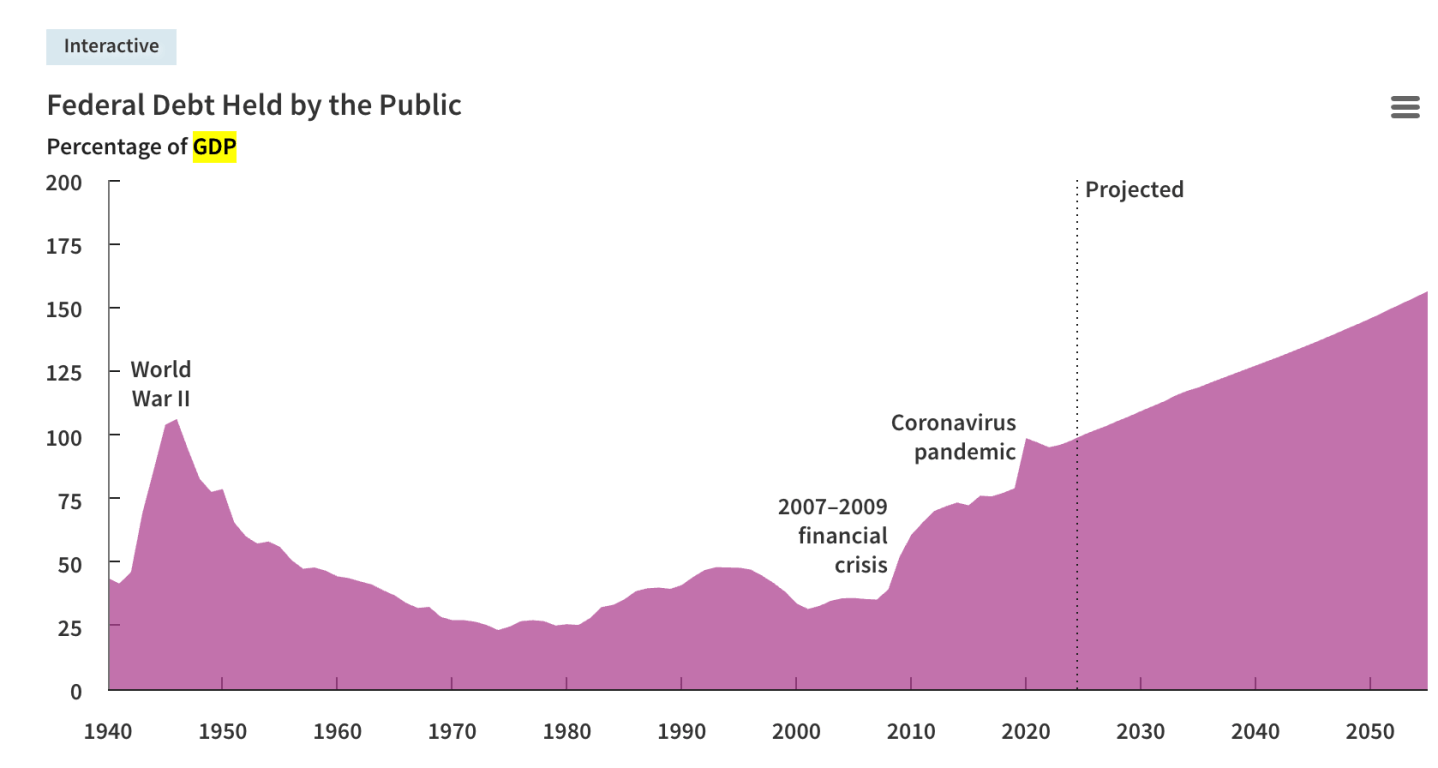

Experts across the economy have been warning for years that America‘s fiscal trajectory is not stable. They point not to the volume of debt, but rather the levels the U.S. is adding to its debt obligations in relation to how quickly its economy is growing, known as the debt-to-GDP ratio. At present, that balance sits at around 125% according to Treasury data, but is expected to hit 156% by 2055, according to the Congressional Budget Office (CBO).

Moreover, economists and policy advisors are concerned by the approach politicians have taken to national debt, saying Washington is not pulling back its spending enough to begin rebalancing the books.

Even for the world’s biggest economy, the debt mountain that America has accumulated is eye-watering. The problem isn’t the $38 trillion itself. In fact, the trading of government debt is the basis of the bond market, a pillar of the global economy. Rather, it’s the interest being paid to service it. As of September the U.S. spent $1.21 trillion to maintain the debt—17% of total federal spending in fiscal year 2025. That interest rate is also increasing over time. Just a couple of years ago, in 2021, the rate of repayment by the U.S. government was, on average, 1.61%. Now it’s 3.36%.

The likes of JPMorgan CEO Jamie Dimon, Bridgewater Associates founder Ray Dalio, and Citadel CEO Ken Griffin have all sounded the alarm from the private sector on government debt, and public committees are ramping up their warnings on Capitol Hill about the future of America’s finances.

Maya MacGuineas, president of the Committee for a Responsible Federal Budget (CRFB) and longtime advocate for responsible budgeting, expressed profound concern over the latest figures in a statement shared with Fortune. “It’s tough to decide what the most appalling part is of today’s announcement from the Treasury,” MacGuineas said: “that we surpassed an unprecedented $38 trillion in gross national debt; that we’ll likely hit the next milestone in just a matter of months; or that we are getting this news amid a government shutdown with seemingly no end in sight.”

Her statement underscored not just the size of the debt, but also the dysfunction surrounding it. The $38 trillion figure refers to gross national debt—the cumulative total of all federal borrowing, including debt held by government accounts and the public. Even by economists’ preferred metric, debt held by the public, MacGuineas argued that the situation is just as bad, with that figure “already as large as our entire economy, beyond any point outside of a world war.”

To her point, gross debt is currently around 123% of GDP and crossed the 100% threshold in late 2012, per federal data. The Congressional Budget Office projected in March 2025 that “federal debt held by the public, boosted by sustained deficits, will grow far beyond any previously recorded level over the next 30 years.”

The remarks from the CRFB head echoed those of another nonpartisan watchdog dedicated to fiscal sustainability, the Peter G. Peterson Foundation. In a previous statement to Fortune, foundation CEO Michael A. Peterson described the $38 trillion debt figure, and the speed at which it is accelerating, as “no way for a great nation like America to run its finances.” The foundation’s calculations underscored the acceleration of the debt issue. “If it seems like we are adding debt faster than ever, that’s because we are. We passed $37 trillion just two months ago, and the pace we’re on is twice as fast as the rate of growth since 2000.”

For MacGuineas, one of the greatest dangers is not simply the debt itself, but the growing sense of complacency surrounding it. “The reality is that we’re becoming distressingly numb to our own dysfunction,” she said. “We fail to pass budgets, we blow past deadlines, we ignore fiscal safeguards, and we haggle over fractions of a budget while leaving the largest drivers untouched.”

Proposals to tackle the debt

Both Republican and Democratic administrations have added to borrowing.

The Trump administration has shown an awareness of the issue and a readiness to address it. Indeed, Dalio has said he has seen a “greater realization” from the current administration about the perils of America’s fiscal environment.

According to the Congressional Budget Office, President Trump’s One Big Beautiful Bill Act (OBBBA) will add $3.4 trillion to national debt by 2034. That number is the net of a decrease in spending of $1.1 trillion and a decrease in revenues of $4.5 trillion. The White House has repeatedly argued that the revenues expected to be generated by tariffs, estimated by the CBO at $3.3 trillion over the next decade, will effectively balance the books.

The CBO has calculated that President Trump’s tariffs regime has the potential to reduce deficits by $4 trillion over the next decade. Some Wall Street analysts agree that tariffs are relevant on this subject. For instance, Apollo Global Management chief economist Torsten Slok said in September that the $350 billion in tariff revenue being generated each year was “very significant,” while J.P. Morgan Asset Management’s chief global strategist, David Kelly, wrote earlier this week that America was “going broke slowly.”

The ratings agency S&P Global reaffirmed the U.S. credit rating, saying that “broad revenue buoyancy, including robust tariff income, will offset any fiscal slippage from tax cuts and spending increases.” Still, the U.S. doesn’t have a top credit rating at any of the three major ratings agencies, with two downgrades occurring in 2025.

Trump has suggested some unusual methods to rebalance the books. For example, he has touted a “Gold Card” plan, a visa policy which would charge rich immigrants $5 million for a green card “plus a route to citizenship.”

“A million cards would be worth $5 trillion, and if you sell 10 million of the cards that’s a total of $50 trillion. Well, we have $35 trillion in debt, so that would be nice,” Trump said.

He noted that he would have $15 trillion “left over” if he managed to sell 10 million cards, adding: “It may be earmarked for deficit reduction, but it actually could be more money than that.” While the math doesn’t necessarily add up (the majority of millionaires already live in the U.S., and the volume of foreigners with a net worth of at least $5 million may be harder to drum up), it nonetheless suggests a willingness to begin addressing the issue.

Indeed, while Trump’s tariff plans have proved unpopular with foreign governments, economists nonetheless welcome the “peculiar” methods to increase America’s income. As Wharton professor Joao Gomes previously told Fortune: “You can also not deny that [Trump and his administration] bring strange forms of revenue that do change the debt picture.”