Good morning,

Well, I’ll say this for Tyson’s Monday earnings call—you don’t hear that everyday.

CFO John R. Tyson, who was arrested last week, participated in the company’s earnings call, his first as finance chief, on Monday. “I’m embarrassed and I want to let you know that I take full responsibility for my actions,” Tyson said. “I just want to apologize to our investors as I have to our employees. This was an incident inconsistent with our company values as well as my personal values. I just wanted you guys to hear this directly from me and that I’m committed to making sure this never happens again.”

“Our independent board of directors are overseeing a thorough review of this matter,” Tyson Foods, Inc. CEO and President Donnie King said. Tyson is the son of the company’s chairman John H. Tyson.

After addressing the elephant in the room, the call moved on to more typical topics in the Q&A portion. One analyst pressed the executives about the result of automation and headcount. The company has made progress in deboning chicken, and pack-out automation across all businesses, King said. “The automation piece specifically is progressing faster than what we had planned.” He added, “We are eliminating difficult jobs and reassigning people to open positions throughout the company.” King didn’t say how much of the workforce would be reduced.

Automation is a component of the Tyson Foods productivity program (along with digital and operational and functional excellence) which aims to deliver more than $1 billion in recurring annual savings by the end of 2024. It’s now ahead of schedule, King said. The company is expected to reach its goal by the end of fiscal 2023, he said.

“We invested $1.9 billion in our business in the past fiscal year, focused primarily on new capacity and automation objectives,” Tyson said on the call.

Automation in the food and consumer goods industry is making gains, according to research by the Association for Advancing Automation released in August. Fifty-nine percent of the 12,305 robots sold in Q2 2022 came from automotive industry orders. The remaining orders from non-automotive companies were largely in the food and consumer goods industry, which saw a 13% increase in unit orders over the same period, April through June, in 2021, according to the association.

With automation comes a need to upskill and re-skill workers who require reassignment. A July McKinsey report recommends offering experiences and apprenticeships, not courses.

Tyson Foods is also aiming to relocate 1,100 corporate employees to its headquarters in Springdale, Ark. coming from offices in downtown Chicago, its Downers Grove suburb, and Dakota Dunes, S.D. beginning early next year. But it’s not clear how many employees will remain with the company and move to Springdale.

King noted that Monday was the deadline employees were given to make a decision. “We want you to remain a part of Tyson Foods,” King said the employees were told. “And quite frankly, I’ve been out recruiting people as other leaders have to come to Northwest Arkansas and we’ve had a lot of success.” For the people who aren’t able to relocate, “We will try to create an opportunity where they can stay with the company long enough so that their replacement could be hired and trained so we don’t have an interruption to business continuity.”

The company’s earnings report showed that consumers are willing to pay up for chicken. For the company’s fourth quarter, the average price of Tyson Foods chicken increased 18.2%. Chicken sales increased from $3.87 billion to $4.62 billion as volume rose 1.1%. Meanwhile, the average beef prices dropped 8.2%, and sales fell from $5.01 billion to $4.86 billion as volume rose 5.1%. The company’s top line beat estimates, but the bottom line fell short.

Regarding executive changes in finance, last month, Stewart Glendinning, CFO since 2017, became group president of prepared foods. Tyson succeeded him as CFO. Before joining the company in 2019, Tyson held roles in investment banking, private equity, and venture capital, including at J.P. Morgan.

Robert Moskow, an analyst at Credit Suisse, questioned how the “organization is responding culturally” to the “reshuffling” of leadership, which breaks from Tyson Foods’s norm of “putting people into the CFO role who have 20 plus years of experience in the finance track,” for example.

At Tyson Foods “our succession planning process is very robust,” King said. He also added, “I’m perfectly comfortable with the people we put in place.”

See you tomorrow.

Sheryl Estrada

sheryl.estrada@fortune.com

Sign up here to receive CFO Daily weekday mornings in your inbox.

Big deal

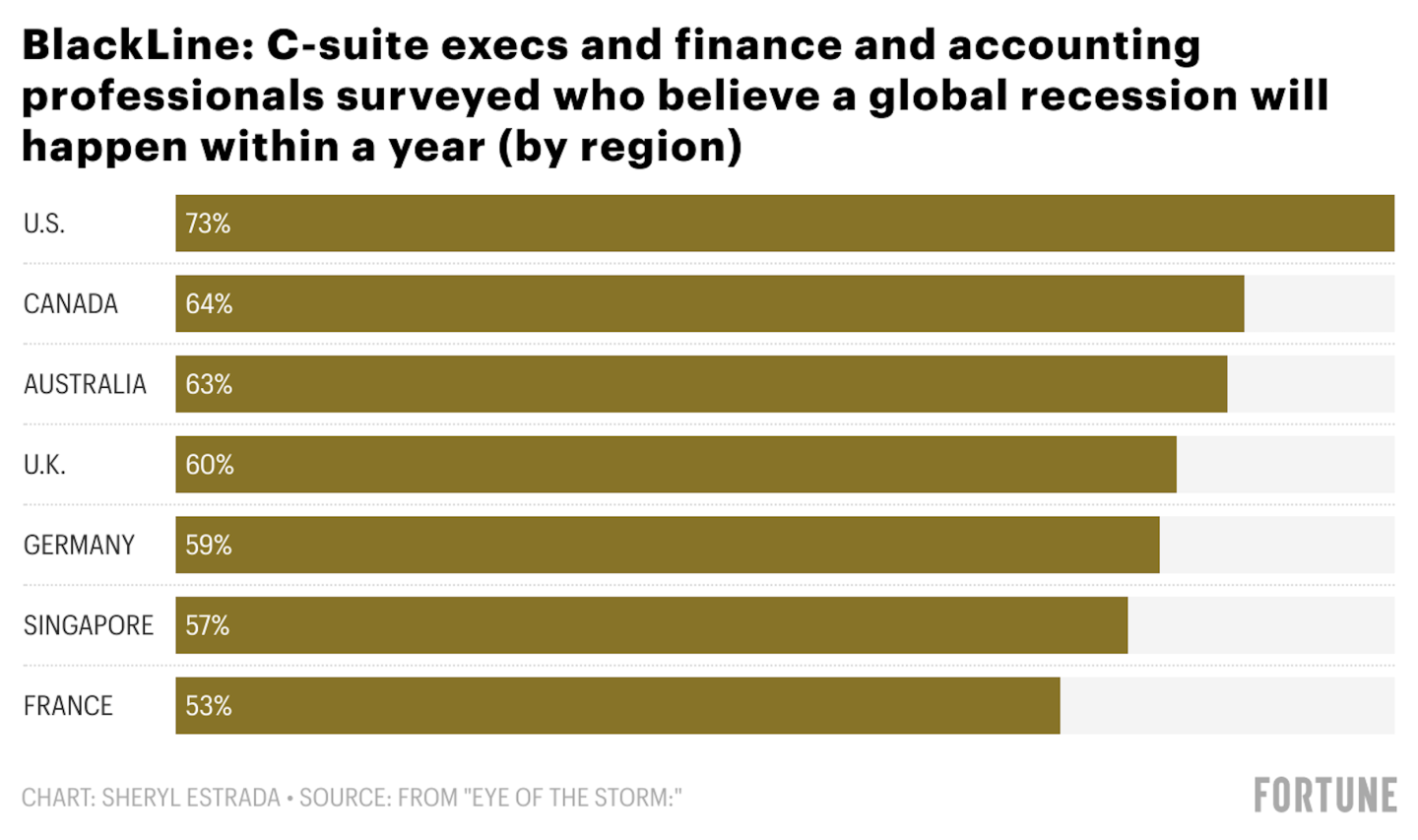

A global survey of C-suite executives and finance and accounting professionals commissioned by BlackLine, Inc. (Nasdaq: BL) released today finds organizations globally are anticipating growing pressure and scrutiny over company financials as a result of ongoing economic uncertainty. Some key findings: In the U.S., 73% of respondents expect a global recession will happen within a year. Overall, nearly all (95%) respondents expect rising interest rates to have an impact on the way their business operates. For example, 43% of respondents said they're concerned that rising interest rates will result in more of their customers paying late (rising to 55% among CEOs), according to the report. Sixty-two percent of respondents agreed that understanding cash flow in real-time is going to become more important. However, 98% said they could be more confident in the visibility they currently have over cash flow. On behalf of BlackLine, between July 29 and Aug. 18, Censuswide surveyed survey of 1,483 business leaders and finance and accounting professionals in the U.S., Canada, U.K., France, Germany, Australia, and Singapore.

Going deeper

"The rise and fall of FTX and Sam Bankman-Fried: The 30-year-old who built a $30 billion empire—then burned it down in 48 hours," a new Fortune feature story, delves into the demise of the crypto exchange founder. Sam Bankman-Fried, who was seen as a benevolent and stabilizing force in crypto, has left his supporters and enemies with unanswered questions.

Leaderboard

Andrew Murphy was promoted to CFO at Duos Technologies, Inc., a subsidiary of Duos Technologies Group, Inc. (Nasdaq: DUOT), effective Nov. 15. Former CFO Adrian Goldfarb will take on a position within Duos's newly formed Industry Advisory Group. Since 2020, Murphy has served as VP of finance at Duos. Before joining Duos, Murphy held progressively senior finance roles within APR Energy, spending nearly five years working in the finance and investor relations teams during the company's time listed on the London Stock Exchange. Before his time with APR, Murphy worked in corporate and public accounting with a focus on tax and business services.

John Stelben was appointed CFO at eHealth, Inc. (Nasdaq: EHTH), a private online health insurance marketplace, effective immediately. Stelben succeeds Christine Janofsky, who is leaving her role at eHealth. Stelben brings more than 25 years of health insurance experience. His most recent experience was at Aetna where he held roles including CFO of governance services. Stelben was also CFO of integrations during various Aetna transactions. Before that, Stelben had multiple senior financial roles at Coventry Health Care, Inc., including interim CFO.

Overheard

“We have made large strides in growing our fan base, expanding our business partnerships, and creating relationships with our community leaders, and we have a great deal of opportunity in front of us.”

—Caroline O’Connor on her promotion on Monday to the president of business operations at The Miami Marlins. It's now the first pro sports team to have women operating the entirety of the team’s day-to-day business, CNBC reported. O'Connor joins the Marlins' Kim Ng, who became the first female general manager in Major League Baseball history when she was hired in 2020.

This is the web version of CFO Daily, a newsletter on the trends and individuals shaping corporate finance. Sign up to get it delivered free to your inbox.