Good morning, CFO Daily readers. Kevin Kelleher here filling in for Sheryl.

CFOs have two common levers to pull when returning cash to shareholders: paying out quarterly dividends and repurchasing shares in the public market through buybacks. Both can present challenges when market selloffs signal a recession may be coming.

During the bull market of 2021, companies were generous with their largesse. Buybacks from S&P 500 companies rose 95% to a record $972 billion in the 12 months through March 2022. Dividends are also being paid at a near record pace: Net dividends for U.S. common stocks reached $70 billion in the 12 months through March.

But so far in 2022, the challenges are hitting fast. The S&P 500 Index is down 13% so far this year. Tech companies with high valuations like Netflix and Amazon saw double-digit declines in a single day after reporting disappointing earnings. But other, non-tech stocks did too, including Walmart and Under Amour.

As for a recession, while economists surveyed by Bloomberg foresee only a 30% chance of one in the coming 12 months, that’s double the odds they predicted three months ago. And keep in mind that before the last recession officially hit in February 2020, economists were predicting a mere 27% chance of one happening. Economists, like most of us, have clearer vision in hindsight.

Recessions, of course, can mean lower profits if not losses. And that can make it tougher for CFOs to decide how much capital to reinvest in core operations versus how much to return to shareholders through dividends and buybacks. Paying too generously to shareholders today can mean skimping on investments needed to share profits with shareholders tomorrow.

“The ability of a company to sustainably and substantially grow their dividend over a business cycle is an indicator of quality,” says Nick Getaz, a portfolio manager at Franklin Equity Group. “But in order to return those dividends tomorrow, you have to be investing today.”

In other words, if you’re wondering whether Wall Street would rather you keep offering dividends and buybacks today, or invest in future profits (and therefore future dividends and buybacks) the answer is: Yes.

So is there any room for flexibility? Both buybacks and dividends can signal managerial optimism about a company’s operations. Buybacks, though, are more suited to act as a release valve for excess capital in good times. And they offer more flexibility in execution: While companies tend to announce buyback plans well in advance, the actual repurchases can be timed with a bit more surgical precision.

Dividends, by contrast, work more like a regular cash bonus rewarding shareholders for loyalty. Aside from the occasional one-time dividend payment, most dividend policies are designed for the long haul. “A dividend, for all intents and purposes, is a commitment and an ability to live up to that commitment,” says Matt Quinlan, who along with Getaz is a portfolio manager at Franklin Equity Group.

With that in mind, it’s not surprising that companies would be more willing to cut buybacks than dividends. During the Great Recession, quarterly dividends paid by S&P 500 companies fell around 30% between mid-2007 and mid-2009, while money spent on buybacks dropped about 85%.

That pattern is likely to play out again if a recession becomes reality. As tempting as buybacks may appear after a stock has lost a third or more of its value, CFOs face the same dilemma that any investor does wondering if they’re buying at a market bottom or catching the proverbial falling knife. Yes, buybacks can shore up an oversold stock or boost a sagging EPS figure, but they are more likely to be effective once investors have established a consensus that markets have hit bottom.

Attempts to time financial markets with dividend policies, however, are more perilous.

“Unless there’s a material change in their business, most CFOs won’t want to reduce their dividends during a downturn,” says Anthony Saglimbene, global market strategist at Ameriprise Financial. “If your company is struggling right now, one of the last things you want to do is cut your dividend because it’s a sign to investors that something’s not right with your business.”

The slow-and-steady, even-keeled policy most companies take toward dividends is one reason investors turn to high dividend-yield companies in tougher times. For now, many companies that can increase dividends are doing so. Last week, Lowe’s raised its dividend 31%. Applied Materials boosted its dividend by 9% in April. Walmart inched up its dividend this year despite higher costs from inflation.

Saglimbene, Getaz, and Quinlan all expect companies to keep boosting dividends moderately in the near term despite the selloff in stocks this spring. If history is a guide, companies will pump the brakes on buybacks first. Only if a weak stock market transitions into a sluggish economy will CFOs start to pare back dividend growth–and even then in a cautious way.

“Given that the economy’s looking like it is slowing, the dividend growth could be slower than it’s been in the last 12 months,” says Franklin’s Quinlan. “Companies that are performing well will keep growing dividends, but those dividend increases may be smaller than they were a year ago.”

See you tomorrow.

Kevin Kelleher

kpkelleher@gmail.com

Big deal

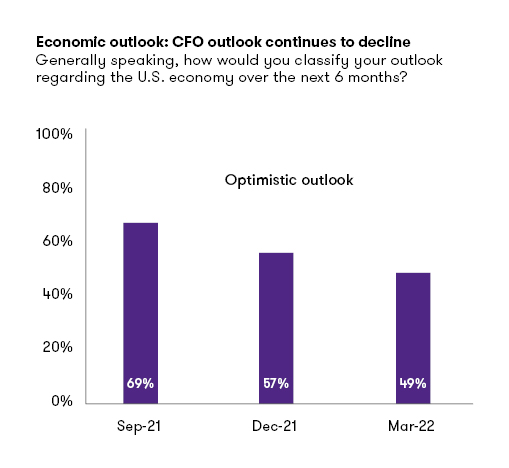

More CFOs are seeing clouds gather on the economic horizon, thanks to inflation, tight labor markets, and the specter of recession. A quarterly survey of CFOs by Grant Thornton found only 49% of CFOs surveyed in March felt optimistic about the economy over the coming six months, down from 69% last September.

“Concerns about a possible recession coupled with the challenge of dealing with spiraling costs are definitely shaping strategy,” Enzo Santilli, a managing partner at Grant Thornton said in a statement. Half of CFOs surveyed said they plan to raise prices in response to inflation, while 60% plan to boost compensation budgets. Cybersecurity and supply chain disruptions also remain top concerns.

Going deeper

Hourly wages in the U.S. fell 2.4% last year, while median compensation for Fortune 500 CEOs jumped 30% to $16 million. Fortune crunched numbers to compare CEO pay to stock performance. CEOs at Altice, Warner Bros. Discovery, and Biogen emerged as having the highest pay relative to stock performance, while Moderna's Stéphane Bancel topped the list of the most underpaid CEOs.

Leaderboard

Gregory J. Peterson will retire from his position as CFO at Southwest Gas Holdings (NYSE: SWX) after 26 years of service. Peterson has served as CFO since 2018 and had previously worked as controller and chief accounting officer at the company. Southwest Gas has initiated the process of finding a successor. He will depart no later than October 2022 and plans to help in the search and transition processes.

Ron Shelton was named CFO at Navitas Semiconductor (Nasdaq: NVTS), a maker of gallium nitride integrated-circuit chips based in El Segundo, Calif. Shelton had previously served as CFO at Adesto Technologies, a provider of application-specific semiconductors for IoT devices. Before that, Shelton was CFO at GigOptix, Cirrus Logic, and other chipmakers. Todd Glickman, who had served as interim CFO, will continue his role as senior vice president of finance at Navitas.

Overheard

“The nasty selloff in the equity market seems to have brought the perma-bears out of hibernation. By some accounts, only two outcomes are plausible: mild or major recession. Our base case remains an extended period of weak growth, and we think any recession is likely to be mild.”

—Research note from a team of BofA Merrill Lynch economists led by Ethan Harris. The note, as reported by Fortune, pushed back against ultra-bearish recession predictions from other voices on Wall Street.