When it comes to being first, Coinbase has racked up an impressive list of achievements.

It was among the first cryptocurrency startups in the country when it launched a decade ago. It went on to become the first crypto unicorn, nabbing a $1.6 billion valuation in 2017. It was the first crypto exchange company to list on Nasdaq in 2021. And it was probably the first stop for your cousin, third-grade teacher, and maybe even your grandma when wading into the wild waters of crypto. It certainly was the first company in history to spend millions bouncing a QR code around the screen during a Super Bowl ad, a gambit that resulted in more than 20 million visitors jamming up the site.

Oh, and as of this year, Coinbase is the first crypto company to join the Fortune 500.

Being first has its benefits: Coinbase is now the largest crypto exchange in the U.S. by trading volume. Its cofounder and largest shareholder, Brian Armstrong, commands a net worth teetering just under $3 billion. The venture capitalists who backed the company early on, like Andreessen Horowitz and Union Square Ventures, have seen dazzling returns from their bets, with some going on to stand up crypto-dedicated funds in hopes of finding the next Coinbase.

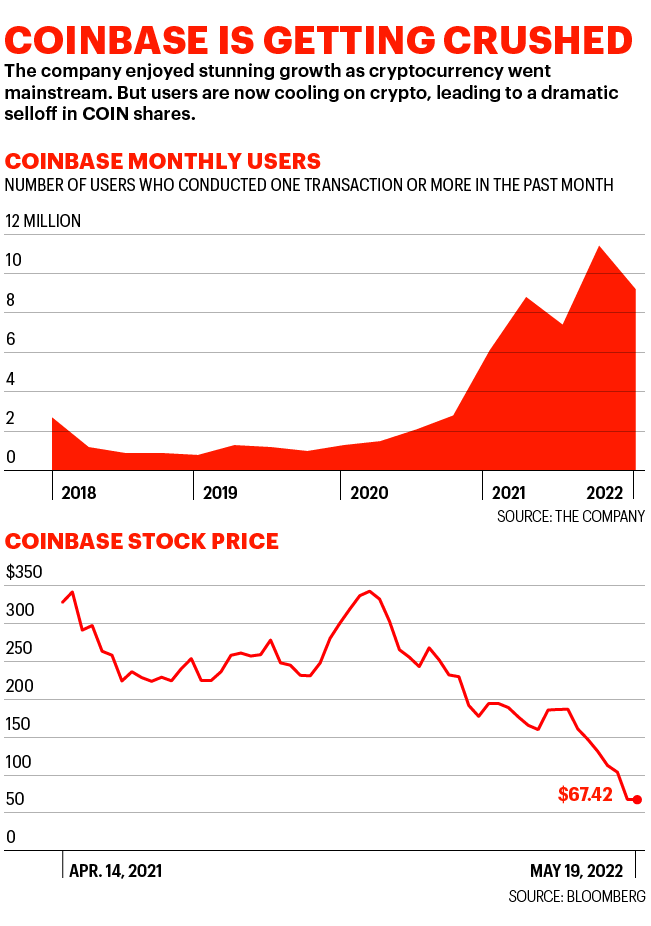

But Coinbase’s latest first—its first-quarter earnings for 2022—was quite a different story. In mid-May the company shocked Wall Street by announcing that its once voluminous profits had plunged to a $430 million loss. Monthly transacting users, the holy grail for measuring customer activity, fell from 11.4 million in the final three months of 2021 to 9.2 million, and the company expects that to fall further in the second quarter. The stock has plunged 73% year to date, from a high of $252 to around $67.

It is all together a stunning reversal for a company accustomed to being, well, first.

As of this year, Coinbase is the first crypto company to join the Fortune 500.

To make matters worse, while customers are pulling back, competitors are circling. Sam Bankman-Fried’s FTX has been building out a one-stop shop for crypto trading in the U.S. and now is turning toward stocks. The American offshoot of Binance, the world’s largest crypto exchange, has moved in to the U.S. with a low-fee trading platform. Even Robinhood is mounting a challenge, announcing in May a plan to let users hold and custody their own crypto and NFTs (non-fungible tokens). And as the economic picture darkens, one thing is clear: Coinbase is hardly the kind of diversified industrial company or many-armed services business built to weather a downturn. The company’s wildly profitable money-spinning machine works only when customers are obsessively trading crypto. That’s where nearly 90% of Coinbase revenues come from. But the past six months have seen Bitcoin fall 46%. Ether has plunged 53%. So-called stablecoins like Tether, which are intended to make it easier to use crypto for transactions and lending, have lost their pegs to the dollar before recovering. And sketchier offerings like Terra, an algorithmic stablecoin, and its token, Luna, have been effectively wiped out. It has been a bloodbath for crypto—and for Coinbase.

As investors size up the company now, they’re asking some vital questions: Will crypto rebound? And if it does, how mainstream can it go, and what piece of that pie will Coinbase hang on to? The company has been asked and has answered those questions before—most recently during the 2018 crypto winter, when some predicted the company’s demise. As COO Emilie Choi put it during the company’s earnings call: “We’re in a strong position. We have a solid balance sheet and we’ve been through several market downturns before, and we’ve emerged stronger every time.” Armstrong went on to paraphrase the famous Warren Buffett motto, no matter that the Oracle is a notorious crypto skeptic: “We’re greedy,” he said, “when others are fearful.”

It was around the winter holidays, back in 2010, that Armstrong first learned about Bitcoin. Sitting in his parents’ home, the San Jose native came across a mysterious white paper about it online by Satoshi Nakamoto. A single Bitcoin cost less than $1 at the time. “When I saw the Bitcoin white paper, my thought was, ‘Wow, this is kind of like the next internet,’ ” Armstrong, who declined to comment for this story, recalled in 2021 on a podcast. “What if this could build a financial system that’s more free, more global?”

Armstrong was hooked. In late 2011, when he was spending his days working as an engineer at Airbnb, he’d retreat home at night and devote the final four to five hours of the day to coding on what would become Coinbase. “I couldn’t help myself,” he later said. Then known as BitBank, the startup’s original idea was to provide Bitcoin owners a safe way to store the crypto that they bought so that they would not have to remember the 64-character private key that provides access to it. It was a model designed to open up the niche crypto markets to the masses. But Armstrong quickly discovered a bigger problem: Few users needed a safe way to store Bitcoin because they did not have an easy way to buy it. So, in late 2012, Armstrong, along with his cofounder, onetime Goldman Sachs trader Fred Ehrsam, launched a “buy Bitcoin” feature on Coinbase.

The product was a hit, with users drawn to the sleek nature of the app that made crypto investing more like buying or selling a stock than wrestling with an arcane new blockchain technology. Coinbase had more than 650,000 consumer Bitcoin wallets by December 2013. Venture capitalists quickly became intrigued, pouring $30 million of funding into Coinbase in 2013 through a Series A in May and a Series B in December. Its investors were some of the most high-profile names on Sand Hill Road, including Andreessen Horowitz, which is Coinbase’s third largest shareholder today, according to S&P Global Market Intelligence data. “Bitcoin is the first plausible proposal for an economic protocol for the internet,” Andreessen Horowitz’s Chris Dixon wrote in a blog post about the investment. “But to proliferate widely, Bitcoin needs a killer app the same way HTTP had web browsers and SMTP had email clients.” Coinbase had the potential to become just that. The company made the early and prescient decision to cooperate with regulators rather than wrangle with them and focus on marketing itself to the masses as the reliable and secure crypto exchange. And then, in 2017, came the $100 million Series D that made Coinbase the first crypto unicorn. It was a banner moment for Coinbase and, by extension, the crypto markets, which had been ripping higher throughout the year.

But then 2018 hit.

While Coinbase had been through plenty of crypto winters before, 2018 was on a new stage. Choi, a longtime LinkedIn executive, first met Armstrong in 2017. He pitched her on a vision of a new financial and technological frontier, one built on blockchain technology that could help increase economic freedom in the world. Choi says she had shivers down her spine.

Bitcoin was trading at nearly $20,000 in December 2017, but by the time Choi was through the onboarding process in March, it was closer to $10,000. It slid to $3,200 one year after Choi signed on. “My naive self was not prepared for this at all,” Choi recalls thinking during a video call with Fortune in early May. “I had no idea about the volatility that I was about to face.”

It was a learning moment for Coinbase. Throughout the market’s boom in 2017, the company had run into several issues—some as basic as whether the website could handle growing traffic, others more complicated, like a flash crash in the price of Ethereum. So when the burst of activity finally subsided, Coinbase got to work. “Things operate differently during peacetime than wartime,” Armstrong once said, according to Kings of Crypto, by former Fortune reporter Jeff John Roberts.

The company did not conduct any sweeping layoffs; rather, it doubled its headcount in the year leading up to September 2018, Fortune reported at the time. Of course, it helped that the interest from investors was still strong. A little over a year after the 2017 fundraise, Coinbase raised new funding that valued it at $8 billion.

Some execs departed; others, like Choi, stayed. “Having pushed through and navigated through that now, we’re so much stronger as a company,” Choi says. “We learned how to do the ups and downs together.”

Coinbase is certainly much larger now. Think of it as a startup, but in a suit. While anyone used to be able to bug Armstrong in the hallway with an idea or a decision, with nearly 5,000 employees that’s no longer realistic. Coinbase became a remote-first company at the outset of the COVID-19 pandemic and ditched an official headquarters. It’s more corporate now, too: It adopted RAPID, the framework born out of management consulting firm Bain & Company, to help speed up decision-making. In a blog post from October, Choi says such a framework helps in determining whether to exit a certain market, for instance.

That said, vestiges of the defiant, norm-breaking culture of crypto certainly remain. Armstrong, for instance, remains prone to dropping shade on the company’s critics on Twitter. In 2021, when the Securities and Exchange Commission effectively forced Coinbase’s hand to stop the rollout of an upcoming lending product, Armstrong tweeted that there was “some really sketchy behavior coming out of the SEC.” And then there was Coinbase’s decision in 2020 to adopt an “apolitical culture,” which Choi cites as one of the best moves the company has ever made. Choi says that Coinbase’s culture, as one former executive used to put it, is like a mullet: “Business in the front, crypto in the back.” It’s the business side of things, however, that has some analysts questioning the company’s future.

It can be an intimidating experience for investors not bilingual in the languages of Corporatese and Cryptonian to listen in on a Coinbase earnings call. But the reality is that for all the talk of dapps and NFTs and opex, Coinbase’s business is relatively simple as it exists today. The company earns about 87% of its revenues from collecting a fee from each transaction. In the first quarter, it collected about 7% of its revenues from fees related to customers staking their crypto through the platform (a process by which users contribute to the operations of a blockchain’s network and earn rewards). Another 3% came from custodial fees collected by the company in return for storing customers’ crypto tokens offline. But analysts see such companion businesses as just that, companions.

Trading is the moneymaker, and there’s the rub. When markets are on the rise, Coinbase’s model works brilliantly. In 2021, Coinbase brought in $6.49 billion in transaction fees from its individual investor client base, up 524% from 2020 and 1,399% from 2019. Institutional investors, meanwhile, paid out $346.3 million in transaction fees to Coinbase. That represented a 519% jump from 2020 and a 1,051% spike from 2019.

No wonder investors were rattled by Q1 of 2022. Revenues? Down 35% year over year. Expenses? Up 111.6% from the same period of 2021, thanks, at least in part, to Coinbase’s recent hiring spree that saw its headcount go from 1,249 employees at year-end 2020 to 3,730 at the end of 2021 to now 4,900. And profits? A net loss per share of $1.98. It did not matter that months earlier Coinbase had warned that a slowdown was afoot. Shares plunged 26% the day after the earnings report, and the count of shares shorted jumped 43.5% in the month leading up to May 16, according to data provider S3 Partners. “Yesterday was COIN’s day of reckoning,” Mizuho senior analyst Dan Dolev wrote later that week.

$6.49 billion

transaction fees Coinbase brought in from its individual investor client base in 2021, up 524% from 2020 and 1,399% from 2019

The stock’s struggles are not expected to ease up anytime soon, either. While Goldman Sachs analyst Will Nance called Coinbase “the blue-chip way to gain exposure to the crypto native ecosystem” in a May note, the fact remains that most investors cannot seemingly be persuaded to touch growth and risk-oriented stocks right now. And without crypto prices or volatility going back on the upswing, profitability is unlikely to return anytime soon, Nance wrote.

Over the long run, the fear is that Coinbase’s “best days are behind it,” Dolev says. Between new competition and high fees (at roughly 1.3% of each transaction Coinbase’s fees are sometimes double that of competitors), Dolev warns that the company could be on a trajectory not unlike that of TD Ameritrade and E*Trade. Those companies relied heavily on commission fees until they were forced to go to $0—and soon after were acquired by larger competitors.

“We’re not modeling bankruptcy,” Dolev tells Fortune. “But if the crypto ice age continues, I think it’s going to be very difficult for their P&L.”

The company’s balance sheet is relatively strong: As of March 31 it had some $6 billion in cash and cash equivalents with another $1.3 billion held in crypto assets (though the value of those would be far lower today). And while the company currently tallies about $3.4 billion in long-term debt, the nearest maturity date on any of that is in 2026.

That leaves Coinbase at a crossroads many a fledgling Fortune 500 company has faced. The engine that powered its growth is quickly turning into a commodity business, and to find growth it must diversify. Coinbase has talked about the need to do so for years, and especially since going public in 2021. Looking forward, Choi thinks Coinbase’s trading business will be akin to advertising at Meta or Alphabet: something that funds and powers the next wave of innovations.

What that next generation will look like is still a work in progress. In the near term, Coinbase is pulling back on some of its most aggressive strategies for 2022 with winter setting in. The company does not plan to triple its headcount this year any longer, for instance. Coinbase is reportedly going on a two-week–long hiring freeze and cutting the amount of money it is spending on Amazon Web Services, while it works to accelerate its core businesses of trading, staking, and custody. “Discipline and prioritization have always been important values at Coinbase, and it is no surprise that they are now more than ever,” chief product officer Surojit Chatterjee wrote in a tweet after the report was released.

But Coinbase does ultimately still want to become an on-ramp to more than just crypto. The company has its eyes set on Web3 in particular, the buzzwordy blockchain-built version of the internet that Chatterjee defines as being a world online where users can read, write, and own their own information and data rather than some faceless corporate giant. So, to do that, Coinbase has been building out newer product lines like an NFT market that was recently rolled out in beta. Coinbase is undoubtedly facing stiff competition on the NFT side, especially considering its slow start versus industry leader OpenSea. But Coinbase hopes to carve out a more unique approach to NFTs than just digital art, with music and real estate standing out as two potential areas, executives say.

Chatterjee sees the company’s Wallet becoming a way for Web3 users to store different tokens they collect from participating in different DeFi protocols, decentralized social media platforms, or otherwise. The company is also building out Coinbase Cloud, which will provide developers APIs and blockchain infrastructure to launch crypto projects. Coinbase Ventures, the company’s VC leg, backed 37 firms in the first quarter—about 20 of which were in fintech—making it the most active corporate VC around, according to CB Insights.

Coinbase certainly still has its bulls. Ehrsam gobbled up more than 5 million shares in the company’s stock in May, and Cathie Wood’s ARK Invest bought about 550,000 shares the day after its first-quarter earnings report. “There is an entirely new economy being built on the blockchain,” notes Devin Ryan, the director of fintech research at Citizens Financial–owned JMP Securities, who has a $250 price target on the stock. “There’s not many firms that have a better view of where the puck is going than Coinbase.” How those ambitions square with the current market reality depends in large part on how deep—and how long—the crypto winter is. And of course, which crypto company monetizes Web3, you guessed it, first.

This article appears in the June/July 2022 issue of Fortune with the headline, “The crypto winter is coming for Coinbase.”

Coinbase Global ranks No. 437 on the 2022 Fortune 500. See the full list here.