Well, I guess this is growing up.

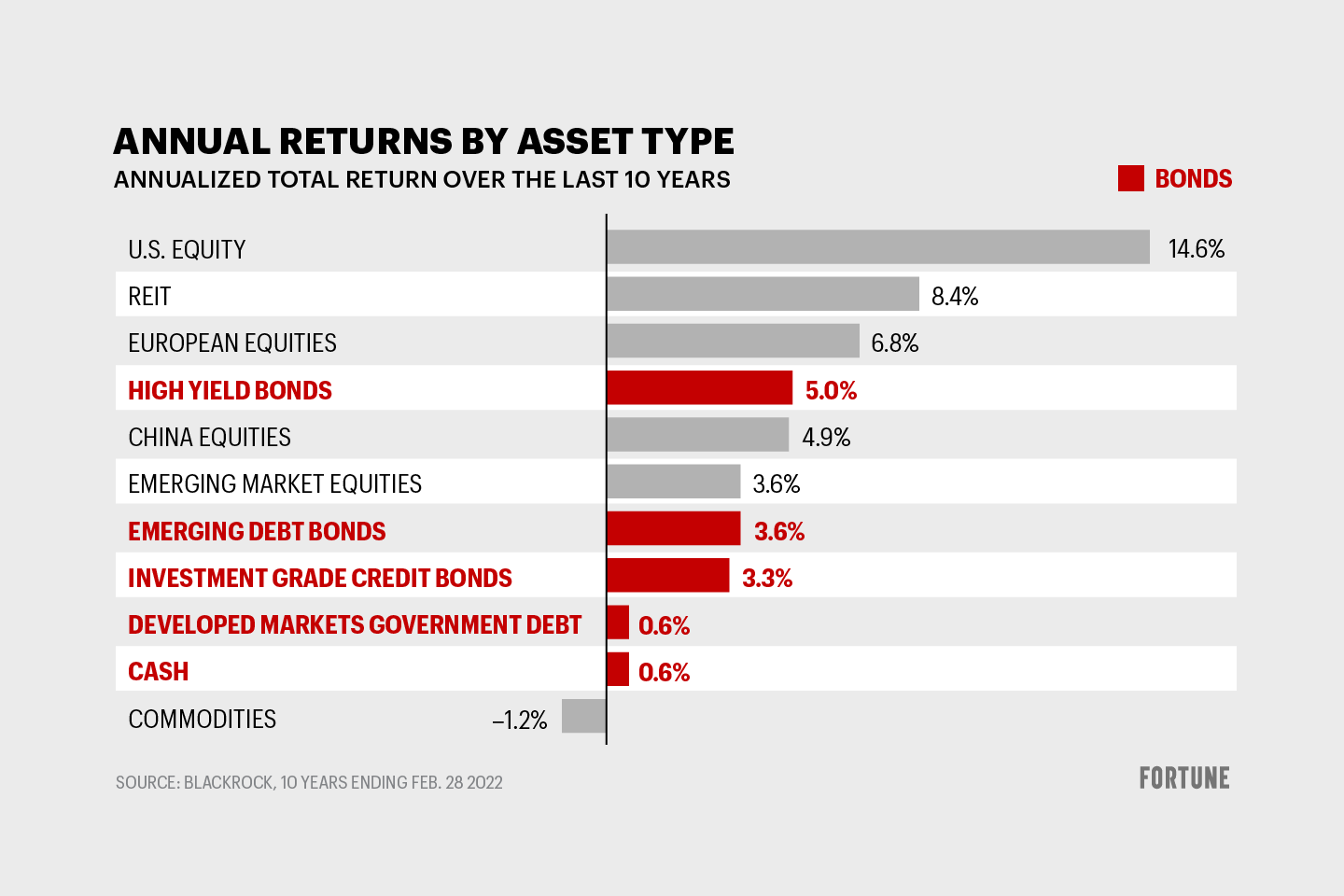

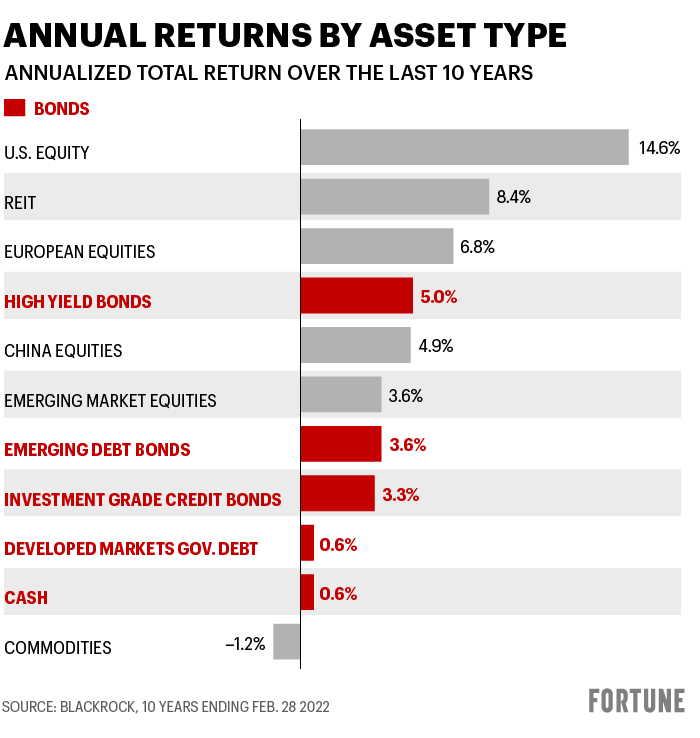

Inflation hasn’t been this bad in 40 years, and investment portfolios suddenly aren’t what they used to be. Enter the trusty standby of a diversified investment strategy: the bond. If you didn’t know much about bond investing before now, the worst inflation since the 1980s means it’s a good time to catch up.

The Russian invasion of Ukraine and rising inflation are impacting the stock market, which has been volatile since the new year. And while some hope the Fed raising interest rates will curb these rising prices, most investors need to come to terms with the fact that they won’t see the growth they’ve enjoyed in recent years.

While the bond market may seem confusing, the truth is bonds are simple debt instruments that can pay off for investors. Real grown-up investors who are prepared for inflation.

What are bonds?

Bonds are basically loans issued by a corporate or government entity when they need capital. The investor who purchases bonds is essentially lending money to this entity, the “issuer” of the bond. While it’s outstanding, the bond pays interest to the investor and the issuer is supposed to pay back the principal in full when the bond matures. (One of the many reasons markets are nervous right now is because one huge issuer, Russia, looks unlikely to pay back its bonds, in other words it might default.)

There are independent credit rating agencies that evaluate default risk of all bonds — the higher the rating, the lower the interest rate. You’ve likely heard of these firms: Moody’s, S&P, and Fitch are the big three.

Many bonds are publicly traded through exchanges, though you can purchase them from a broker.

A bond’s price and yield is what determines its value — the price is the amount it’s bought and sold for, and the yield is the expected annual return once the bond reaches maturity.

Should everyone own bonds?

Bonds aren’t right for everyone.

“Investors should only consider purchasing bonds after they have carefully considered their goals, timeframe, and especially their tolerance for risk,” says Kimberly Foss, CFP, president and founder of Empyrion Wealth Management. “Investors need to understand that even with government-guaranteed bonds, the value of the asset will fluctuate over time and could affect the amount of money they would receive if they sold the bond prior to maturity.”

In general, bonds can offer relative stability, but you need to take your age and risk tolerance into consideration when deciding how many to buy. For instance, if you’re older and nearing retirement, it might make sense to have more bonds in your portfolio.

Traditionally, the moderate risk profile of 60% in stocks and 40% in bonds has been considered appropriate, but Foss says that may no longer be the case. “In an environment of higher inflation and interest rates that are still historically low, those needing to achieve long-term growth that outpaces inflation may need to consider allocating more assets to equities, which have shown the most durable ability to outpace inflation,” Foss says.

There are trade-offs when it comes to having more stability in your portfolio versus wanting higher returns. Investors who seek higher returns may do better investing less in bonds and more in stocks, or assets.

Bonds aren’t good vehicles for building wealth, especially for someone with a longer time horizon, argues Robert R. Johnson, professor of finance at the Heider College of Business, at Creighton University.

“Over the very long term, a diversified portfolio of stocks outperforms a diversified portfolio of bonds by a wide margin,” he says. “Investors can invest in dividend paying stocks since they increase, whereas with bonds, the holder only receives the promised interest payment and principal back.”

What are different types of bonds?

The three main types of bonds are corporate bonds, municipal bonds, and U.S. Treasuries. While they’re all issued by various entities and have different maturity dates, they basically work the same way: Investors are able to assess the credit risk, receive a steady income from the interest, and the principal is paid back upon maturity.

However, there are some types of bonds that vary slightly, including:

- Convertible bonds: Think of this type of bond as a hybrid security in that they have both aspects of bonds and stocks. You may keep your initial investment in bonds, Foss explains, but then convert to a certain number of shares of the issuer’s stock, depending on the terms of the bond. Convertible bonds tend to fluctuate more compared to regular bonds, and by converting to stocks, there is the potential you could earn more money.

- Treasury Inflation-Protected Securities: Also referred to as TIPS, this type of bond is issued by the U.S. government with a fixed interest rate which many inventors hope to use to keep up with, or beat, the rate of inflation. Where it differs from other types of bonds is that the face value, or principal amount, may adjust to reflect the rise of inflation, or even deflation, so the principal amount of the bond increases, and vice versa, based on the Consumer Price Index. However, even if the face value of the bond goes down, the bondholder will never receive less than what they originally paid for.

- I-Bonds: These Treasury bonds pay interest in two ways. First, bondholders receive a fixed interest rate, then another that will vary based on the current inflation rate, or the Consumer Price Index. The variable rate is adjusted semi-annually (May and November). Individual investors can cash them out after 12 months — you won’t be paid while the bond is in your possession. The interest earned isn’t taxable until the bond matures or until the investor sells, though some exceptions apply (like if you use proceeds toward qualifying educational expenses).

Are bonds a good way to protect my money when inflation is high?

Investors should have a plan to put their money in assets that typically outperform the market, especially during times of high inflation. In any case, you want to make sure your portfolio is well-diversified, but increasing certain types of securities, like bonds, may be a good choice when inflation hits.

A common way investors usually hedge against inflation is by purchasing TIPS, since the principal is adjusted based on inflation. This makes them a valuable investment for anyone looking to ensure the fixed-income portion of their portfolio matches with rising inflation.

If the value of your TIPS increases because of inflation, the gain will be considered taxable income, says Johnson, even if you won’t receive the money until maturity. Although they can be a good hedge against inflation, you may have to pay more in taxes depending on your financial situation.

What does it mean if the Fed is selling bonds?

If the Fed is selling bonds, it could be a sign interest rates are going up. That being said, the Fed sells bonds all the time to help control the money supply and how much money is in circulation — to prevent high inflation rates, it could sell less or more depending on the state of the economy, according to Foss.

In general, when the Fed sells bonds, it could influence interest rates, including rates for bonds, which ultimately could mean the bonds in your portfolio may go up in value, though it will depend on other factors as well.

What are some good bond funds or ETFs?

As always with investing, what’s considered “good” to one investor might not be right for another. It’s important to assess your financial goals, age, and other factors like your risk tolerance to determine how much of your portfolio you should allocate to bonds, and what types to purchase.

In many cases, bond ETFs are a good choice since you can diversify your portfolio across different kinds of bonds. For those who can meet the minimum purchase requirements for government bonds, it may be worth considering since they offer as much stability as corporate issued ones.

It’s important to do your research to understand your risk tolerance. Like other types of investments, it’s helpful to have a plan for your bonds, so if you decide to sell before the reach maturity you understand the financial consequences. Finding the right resources like a trusted financial advisor, even if you just hire them for a one-off meeting, will help you make an informed decision to help you reach your investment goals.