Good morning.

European stocks and U.S. futures have turned positive in the past hour as bond yields and oil prices recede. The moves are really small, however, as investors wait on the first batch of corporate earnings and the latest inflation data, both due out in a few hours.

The rally in Bitcoin, meanwhile, is in trouble. The biggest cryptocurrency has been falling throughout the morning. Still, it’s one-week gains have been impressive.

In today’s essay, we have a Q3 earnings preview.

Before we get to that, let’s check in on the headlines moving markets.

Markets update

Asia

- The Asian markets are mostly lower with the Hang Seng, the worst of the bunch, down 1.4% in afternoon trading.

- Some good news for Tesla bulls: the EV maker set a new monthly high for the sale of China-built cars in September. TSLA closed up 1.7% yesterday.

- Speaking of records… China’s trade surplus with the U.S. hit a new record last month.

Europe

- The European bourses were rebounding somewhat, with the Stoxx Europe 600 up nearly 0.5% two hours into the trading session.

- Tech was one of the big gainers at the open, helped by SAP. Shares leaped 2.3% after the tech giant raised full-year guidance as its cloud business takes off.

- You may recall CureVac as the German biotech firm working on a COVID cure that then-president Donald Trump reportedly tried to buy in the spring of 2020. Yesterday, the company announced it was halting its first-gen COVID vaccine candidate, and its shares tanked.

U.S.

- U.S. futures are on the rise this morning. That’s after all three major averages fell for a third straight session. Yesterday’s outlier: the small-cap Russell 2000.

- In addition to bank earnings, we have the closely watched CPI report due out today before the bell. Economists forecast another surge in consumer prices, putting inflation at 5.3% on an annualized rate. This is the last big inflation reading ahead of the Fed’s next meeting.

- Shares in Apple are down 1.3% pre-market after Bloomberg reported it will cut production of its iPhone 13 by a whopping 10 million units as the global chips shortage intensifies.

Elsewhere

- Gold is a touch higher, trading above $1,760/ounce.

- The dollar is down.

- Crude has been steady over the past two days with Brent trading around $83/barrel.

- Bitcoin fell more than 4% in the past 24 hours to trade below $55,000.

***

Earnings season preview

At 7 a.m. ET today we get the unofficial kickoff to earnings season when JPMorgan Chase reports. The banks are a big bellwether for consumer strength (the housing market and trading, too), so plenty of attention will be paid to the first batch of Big Finance reports over the next few days.

Yesterday, we looked at the strong-dollar impact on Q3 earnings. The verdict: if the greenback continues to surge this could be a big headache for Corporate America in the coming quarters.

Today, let’s zoom in on what corporates are likely to be telling us about their near-term prospects. Wall Street is in agreement: this will be a big earnings season. “We believe it will be a make-or-break quarter with all eyes on margins and supply chain,” Savita Subramanian, BofA Securities equity and quantity strategist, wrote in an investor note yesterday.

BofA cautions that inflation, labor shortages and Delta-driven slowdowns will very likely appear in results, and, for some, impact forward-guidance. Why do they say that? Because that’s what companies have been warning of in recent weeks.

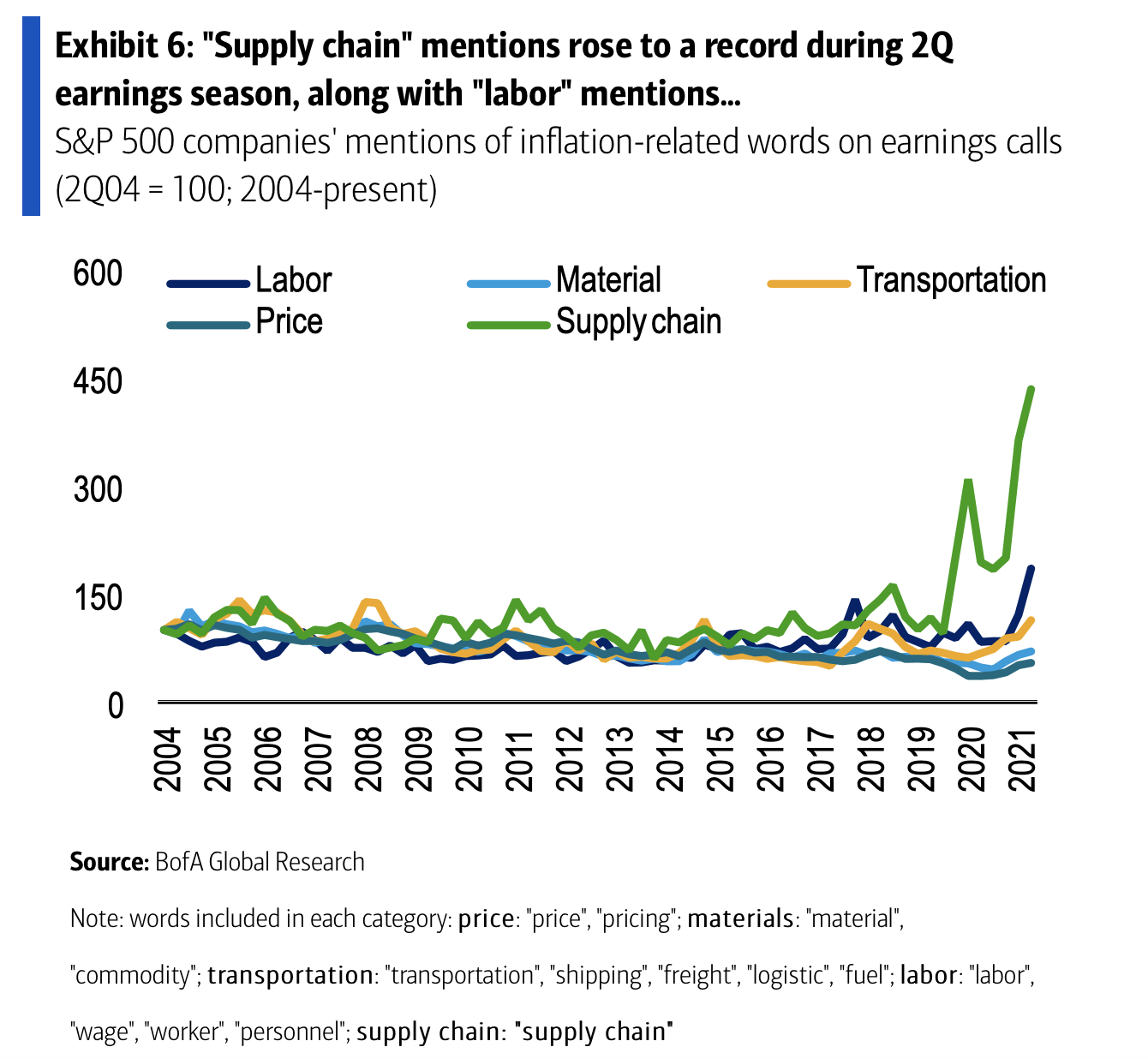

Take supply chains. CFOs grumbled about supply supply chain disruptions so often last quarter that had you challenged your pal to a drinking game—chug a root beer every time the words are mentioned in an analyst call—you’d be really sick of root beer right now. Thank goodness you didn’t do anything that foolish. Just look at how many supply chain mentions (labor, too) there were last quarter, according to this BofA tally. Hundreds!

Add it all up, and analysts predict margin growth will fall this quarter, but then stabilize. BofA isn’t buying this somewhat rosy picture. “We expect current headwinds to last well into 2022,” Subramanian’s team writes, “and see risk to consensus numbers.”

Why such a downer? “Supply chain is in the limelight, but wages, China issues, and soaring commodity prices also pose risks to earnings,” they write. As such, “we believe 2022 EPS will be revised lower.”

I’ve mentioned here before in this space that BofA’s Subramanian is less bullish on equities than many of her peers. Her call in early September that stocks would essentially flat-line looks particularly prescient. And so her take ahead of the Q3 earnings season will be closely watched.

***

Bernhard Warner

@BernhardWarner

Bernhard.Warner@Fortune.com

As always, you can write to bullsheet@fortune.com or reply to this email with suggestions and feedback.

Today's reads

Oatly learns that it’s not easy being ‘green’—Fortune

Pandemic unemployment is cutting into stock market returns for women—Fortune

As Bike Thefts Jump, Delivery Workers Band Together for Safety—The New York Times

IMF Cuts Global Growth Forecast Amid Supply-Chain Disruptions, Pandemic Pressures—Wall Street Journal

Market candy

Quote of the day

Consumers are shopping faster and paying less attention to pricing as a decision factor...Consumers seem to be looking at prices a little bit differently than before.

That's PepsiCo CEO Ramon Laguarta arguing on an analyst call that inflationary pressures aren't the bogeyman economists and the financial press make it out to be. Do you agree, dear consumer? Before you answer that, here's the full story, courtesy of Fortune's Shawn Tully.

This is the web version of Bull Sheet, a no-nonsense daily newsletter on what’s happening in the markets. Sign up to get it delivered free to your inbox.