Something unexpected happened last year: Even as the economy was in the dumps with the jobless rate above double digits, the housing market went on a historic run. Since the onset of the pandemic, the median home price in the United States is up 24%.

But that hot housing market is finally starting to show signs of cooling.

“Things are still good, they’re just not frenzied anymore. Which, to be honest, frenzy in the housing market never really leads to good behavior,” Devyn Bachman, vice president of research at John Burns Real Estate Consulting, told Fortune.

As housing continues to shift slightly in buyers’ favor, there are six things buyers and sellers need to know about the market.

1. More homes are going on the market

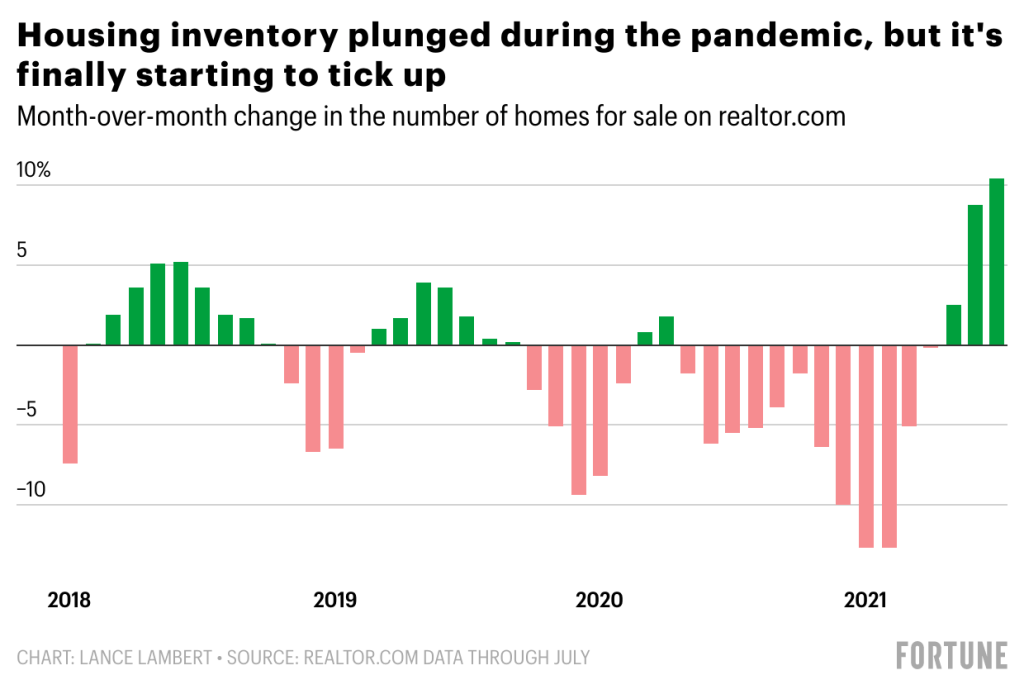

Between April 2020 and April 2021, the number of homes listed on Realtor.com fell 53% as buyers snapped up everything they could. Sometimes buyers were even forgoing final home inspections.

In recent months that has reversed, with inventory finally rising again. Since May, inventory has climbed 23%.

As Fortune reported last week, increased inventory is good news for homebuyers who’ve been pitted against one another in one of the most competitive housing markets in the country’s history. This steady uptick in inventory, Bachman said, is a clear sign that some of the crazy is beginning to leave the market. It has also coincided with a slowdown in home price appreciation.

2. Homebuyers are finally pushing back at record prices

CoreLogic, a real estate research firm, finds at one point this summer home prices appreciated 17% year over year. But in recent weeks, homebuyers are finally starting to balk at record prices.

“When you’re talking 17%, that is four times national income growth. That’s not sustainable, that’s not healthy,” Bachman said. This buyer pushback was inevitable and continues to spread across the nation, she added.

But the cooling in the market isn’t only a result of buyers’ fatigue. It’s also because seasonality is returning. Historically, the housing market cools in the summer and fall as buyers get absorbed into vacations and the return of school. But that didn’t happen last year as vacations were postponed, and many schools went online. This year, that seasonality returned in a big way.

“It’s seasonality on steroids this year, because you locked people in their homes for a year and half, and finally people took summer vacations,” Bachman said. That return of seasonality has given inventory some breathing room to finally rise.

3. Forecasts don’t predict home prices falling

While the market is cooling, it doesn’t mean we’re headed for a crash. In fact, forecasts don’t even show prices falling. CoreLogic forecasts a modest 3.2% home appreciation over the next 12 months. If that comes to fruition it would still mean relief for home shoppers—given prices jumped 17% in the past year.

“What we see is a more normalized pricing environment going forward, one that is not nearly as frenzied as what we’re seeing today. But by no means are we calling a pricing correction,” Bachman said.

4. International homebuyers are coming back

Amid the pandemic, international travel fell off a cliff. Subsequently, international homebuying also fell. That had a negative impact on international markets like Manhattan and San Francisco.

But in recent months more of those buyers, particularly from Europe, are expected to come back as international travel begins to recover, Anthony Hitt, CEO of Engel & Völkers Americas, told Fortune. He expects that to continue to aid in the recovery of luxury markets in big U.S. cosmopolitan areas.

5. Mortgage rates remain historically low

At the onset of the economic crisis, the Federal Reserve turned to one of its most powerful tools: lowering interest rates. For much of the past year, the average 30-year fixed mortgage rate has been below 3%—something that attracted a wave of homebuying and mortgage refinancing.

But the combination of an improved economy and rising inflation is increasing the odds that the Federal Reserve will begin to raise rates.

Freddie Mac forecasts that by the end of 2022 average mortgage rates will climb to 3.7%—up from its current 2.87%. Of course, any upward movement in mortgage rates puts negative pressure on the housing market.

6. Forbearance is set to end on Sept. 30

At the end of July, the foreclosure moratorium, which prevented foreclosures on federally backed mortgages, came to an end. Now, the mortgage forbearance program, which allows some borrowers to pause their payments, is set to begin to wind down on Sept. 30. In total, more than 1.7 million mortgage borrowers are still protected by the forbearance program. That’s 3.5% of U.S. mortgages.

What does the end of the forbearance program mean for the housing market? To answer that question, Fortune recently asked researchers at Home.LLC to run the numbers. Their forecast finds the end of the program could cause housing inventory to rise another 11% this year.

Dive into stories from Fortune’s print edition:

- Crypto traders anonymous: A new addiction takes hold for many as cryptocurrency goes mainstream

- How Toyota kept making cars when the chips were down

- Ethereum risks it all on going green

- NFTy 50: The most influential builders, creatives, and influencers in the NFT world

- The war to charge your electric car is powering up

Subscribe to Fortune Daily to get essential business stories straight to your inbox each morning.