Europe is paying a steep price for its botched COVID vaccination rollout. The reminders are everywhere.

During Easter week, when Rome is usually teeming with tourists and pilgrims, there was no in-person dining in the city’s famed trattorias—there weren’t any pilgrims or tourists, for that matter. Frustrations boiled over from there. Earlier this week, a violent clash with police broke out during a protest in the Rome city center. On hand were restaurant owners and hoteliers demanding the blanket closures be lifted as the losses on their businesses pile up under lockdown.

In France, it’s a similar story. Stir-crazy Parisians are going to desperate measures to meet for an aperitif, risking massive fines. Spring festivals, meanwhile, across Germany have been canceled, or are in doubt.

For the second straight year, Europeans are emerging from the winter cold with all kinds of restrictions on their social life. Rising COVID cases during much of February and March across the eurozone had led to wave upon wave of school and business closures that look to drag on for much if not all of April. The impositions aren’t quite as strenuous as Lockdown 1.0 a year ago, but they’re all the more frustrating when viewed in context to the successful vaccination campaigns underway across the English Channel, in Great Britain, or across the Atlantic, in the United States.

As of April 12, Germany, France, and Italy had given COVID vaccinations to roughly 15% of the population—a rate that significantly trails the U.S. and Britain.

Supply constraints, political overreach, and confusion among the public have meddled with the continent’s best efforts to keep from falling so far behind its trading partners, Britain, and the U.S.

According to Holger Schmieding, chief economist at Berenberg Bank, the shutdowns across the eurozone in February and March probably resulted in a 4% hit to the bloc’s GDP. Going forward, he adds, “each extra month of lockdowns thus reduces annual 2021 GDP by some 0.3%.”

The European Union is a massive economy, accounting for about 15 percent of global trade. To say Europe’s economic stumbles are a drag on the global economy is no understatement.

Here’s how the bloc’s stuttered rollout of vaccines could impact the markets and the economy abroad.

Economic growth

Last summer, economists began running the numbers and liked what they saw in Europe. The eurozone economy, they said, was ripe for a significant rebound in the year ahead on hopes that a €750 billion ($890 billion) recovery plan would prove to be a stimulative jolt to the trading bloc.

Back then, the consensus forecast was for the eurozone to produce a stronger growth rate than that of the U.S. in 2021. The fortunes of the trading giants, however, began to diverge 10 days before Christmas when the U.S. got the jump on vaccinations. It hasn’t looked back. The U.S. economic outlook continues to improve—trillions in stimulus spending and trillions more promised to fix roads and bridges does wonders for turbocharging growth.

According to Berenberg’s latest forecast, the U.S. economy is growing at such a blazing pace it will return to pre-pandemic levels as soon as this quarter. The eurozone won’t hit that milestone until Q1, 2022.

The International Monetary Fund concurs. The eurozone, says IMF chief economist Gita Gopinath, is “a couple of months behind the U.S. in terms of the recovery,” and, therefore, it cannot be counted on in quite the same way to propel global growth until later in the year, at best.

Stocks

If the growth story is the bad news, the glass-half-full assessment can be seen in equities. That’s because any slowdown in the European economic engine will likely be short-lived, Berenberg’s Schmieding says. Sure enough, investors have been piling back into European stocks at a ferocious clip since early March. After Easter, the benchmark Stoxx Europe 600 hit an all-time high, erasing all pandemic-era losses.

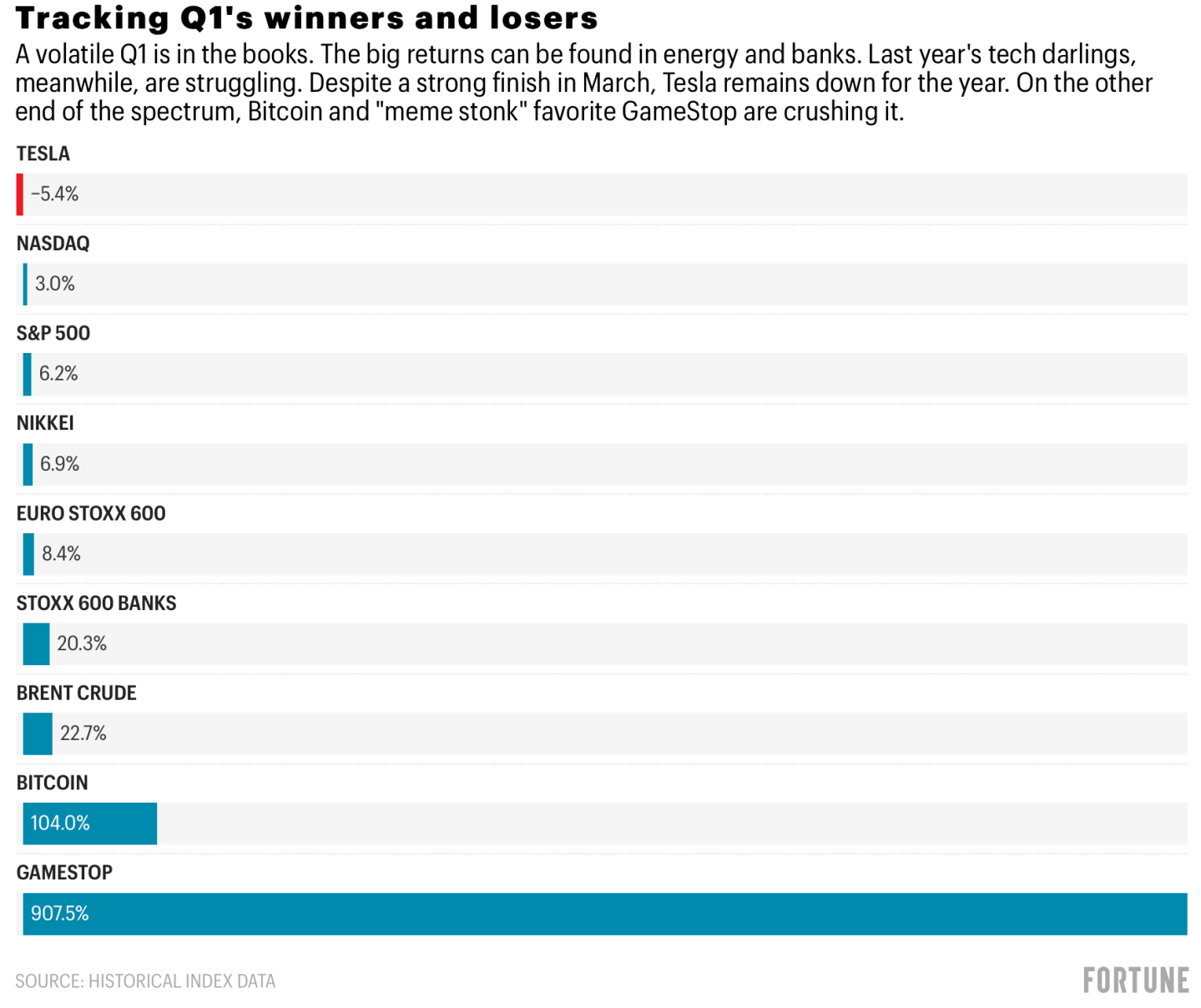

The whole of the first quarter was pretty stellar for European stocks. “In a major reversal from 2020, it was European indices which saw the largest advances,” Deutsche Bank investment strategist Jim Reid and research analyst Henry Allen wrote in an investor note on April 1. “Over Q1, the DAX (+9.4%), the FTSE MIB (+11.3%) and the STOXX 600 (+8.4%) all saw solid gains in total return terms, while banks led the way thanks to higher yields, with the STOXX 600 Banks up +20.3% over the quarter.”

Alas, European stocks have been flat since investors came back from the Easter break. One reason? All eyes are on the EU’s improving, yet still underperforming, vaccination numbers.

FX

With the Biden administration in a spending mood, 2021 was supposed to be a bad year for the dollar. And then Europe happened. The greenback just notched its best quarter since 2018. So far this year, the dollar has appreciated 4% versus the euro, a huge jump in foreign-exchange (FX) terms. The reason: Investors have lost faith in Europe’s vaccination campaign, sending traders increasingly to the safe-haven dollar. The British pound has also gained on the euro during the same period.

Moody’s for one doesn’t see dollar strength as a blip. Capital flows will continue to favor U.S. dollar assets throughout the year and into 2022, the ratings agency says.

“We expect the U.S. economy this year to outperform other developed markets, such as the euro area, because its economy will reopen earlier on account of its speedy vaccine rollout and because of its massive fiscal response,” Moody’s said in an April 12 investor note. “The European Central Bank (ECB) and the Bank of Japan will likely maintain an accommodative policy stance for much longer than the Federal Reserve, giving the dollar the potential for additional appreciation.”

BofA Securities is also bearish on the euro. Last week it slapped a new year-end price target on the dollar-euro FX rate of $1.15 = €1.

A strong dollar is bad news for multinationals and exporters—particularly if they’re exporting to countries hobbled by lockdowns. If the dump-the-euro trade continues, watch for an increasing number of Fortune 500 firms to warn about the “currency effects” hit on profits.

Interest rates

Bond yields have been going up just about everywhere in the developed world since the start of the year as investors bet on growth and, with that, inflation. That will impact monetary policy, and, the thinking goes, a rate hike could pour cold water on the stocks rally.

Right now, investors are betting the Fed will grow incrementally more hawkish as prices rise—a move meant to put the brakes on an overheating American economy. They’re banking on U.S. interest rate hikes in 2023. That’s still a long way off, but at least investors can agree on a general path to tightening rates.

No such visibility exists in Europe. Growth and inflation are still hard to pin down in the eurozone, and that’s likely to keep the European Central Bank in limbo for some time, investors grumble.

“The ECB continues missing its inflation target, and inflation expectations suggest that the target will remain beyond reach for the foreseeable future. And yet, the ECB is failing to explain how they define ‘favorable,’ what ‘financing conditions’ they target, and what are their red lines,” BofA Securities analysts wrote in a recent note. A big reason for that? Yep, uncertainty around the vaccine rollout.

A gap on monetary policy between the Fed and ECB is nothing new. Europe has been the land of negative rates for years, creating a brutal environment for the continent’s biggest lenders. But should that gulf widen, it could add further rocket fuel to the dollar, which again would be bad news for American multinationals and exporters, and, ultimately, the trade gap between the U.S. and Europe.

Travel and tourism

Successful vaccine drives are particularly critical to economies that depend on tourism for growth. That’s true everywhere in the world. But the eurozone as a whole is far more dependent on tourism receipts than its trading partners—even more so in Europe’s sunny South, as the BofA Securities chart below shows.

BofA Securities analysts reckon that the eurozone will have to triple its vaccination pace to fully reopen to overseas tourists by July. If it overshoots by a factor of one on that goal, it could even reopen a month earlier, by June.

In other words, it has to overperform on vaccine jabs to save the summer. If it doesn’t, get ready for more street protests.