This is the web version of The Ledger, Fortune’s weekly newsletter covering financial technology and cryptocurrency. Sign up here to get it free in your inbox.

It was close to inevitable. At any public event over the last five years or so, there’s been a good chance that some passionate convert would show up to declare that, regardless of the question at hand, Bitcoin was the answer.

Here’s that guy, during the protests and rioting happening across American cities right now, photographed by ProPublica reporter Jessica Huseman in Austin. (There were other That Guys.)

For those of us who have been involved with Bitcoin the longest, this sort of thing has become a running joke. There are compelling arguments that a decentralized, uncensorable, global financial infrastructure would fix long-running social problems. But, especially for those learning about Bitcoin for the first time, it can be tempting to throw “Bitcoin fixes this” around loosely, to say the least.

So let’s be clear: Bitcoin can’t fix what happened to George Floyd, a father and respected member of his community who was, according to an independent autopsy, asphyxiated by a police officer who knelt directly on the back of his neck for 8 minutes and 46 seconds. Bitcoin can’t fix the fact that that officer, Derek Chauvin, was still employed by the Minneapolis PD despite a history of complaints and fatal incidents.

Bitcoin can’t fix the three officers who stood by and did nothing as Floyd pleaded for his life, then went silent. And it can’t fix the militarized, indiscriminate police violence that is currently undermining many Americans’ trust in their friendly neighborhood peacekeeper.

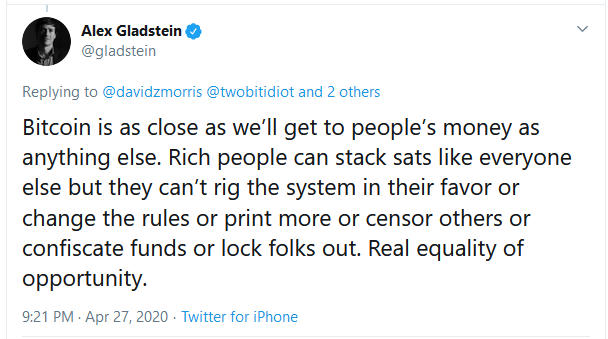

I got a refresher on one major argument for Bitcoin’s ability to fix deep social problems in an April conversation with Alex Gladstein, chief strategy officer of the Human Rights Foundation and, for the last couple of years, a passionate Bitcoin advocate.

Those who see Bitcoin as a tool of reform believe that because Bitcoin is fair, and can’t be manipulated by the powerful, a society that used it would be fair. It’s a compelling argument.

But the events of the past week highlight a key limitation: the massive weight of history. Any simply ‘fair’ system, financial or otherwise, at best preserves the status quo.

In the United States, the status quo is the result of centuries of legally-enshrined oppression of minorities, particularly Native and African Americans. Strictly on the financial side, policies like redlining and discriminatory elements of the New Deal have engineered a massive racial wealth gap. In 2016, the net worth of a typical white U.S. family was ten times the net worth of a typical black family. Perhaps Bitcoin could have mitigated state violence and theft if it had somehow existed two centuries ago, but it can’t reverse those effects.

America’s racial wealth gap reinforces and enables the police abuses being protested by those in the streets as I type this. Undermining people’s financial security leaves them fewer tools to fight back when authorities threaten their lives and freedom.

And no merely technological innovation can do much to stop the pernicious underlying cause of these and other tactics of oppression: racism. That demonic weed is nurtured by words, not code. It has been fed generously by demagogues, charlatans, and even great innovators throughout American history.

As long as that continues, Bitcoin won’t fix what really matters.

David Morris

DECENTRALIZED NEWS

Credits

Western Union makes a takeover offer for Moneygram ... Square CEO Jack Dorsey calls for police reform ... Citigroup CFO Mark Mason speaks out on George Floyd's death ... Challenger bank Starling raises 40 million pounds ... Varo Money raises $241M series D ... Bitcoin shows high correlation with gold ... China allocates $56.1 billion to buy loans to small businesses ... Big IPOs still flock to the world's oldest exchange ... U.S. legislation would audit Chinese firms seeking stock listings ... Cryptocurrency-fueled browser Brave reports 15 million monthly users.

Debits

U.S. puts $5 million bounty on Venezuela's cryptocurrency chief ... ATMs robbed across Philadelphia during uprising ... Kraken CEO says business owners should "do their own shooting" ... Cryptocurrency frauds and hacks total $1.3 billion so far in 2019 ... Complex exchange-traded notes wipe out retail investors ... Wealthy Lebanese favor luxury goods over banks to store savings ... Trump admin delays economic forecasts ... No-deal Brexit could force U.K. rates negative ... JPMorgan settles over inflated crypto-purchase fees ... "Blockchain journalism" startup Civil shuts down.

BUBBLE-O-METER

+1.5%

The rise in the Dow Jones Industrial Average between Monday's open and Tuesday's close, as markets continue a seemingly gravity-defying run. Since hitting bottom below 18,600 in March, the Dow has risen a stunning 38.4% as the worst-case coronavirus scenario was seemingly averted, and despite the outbreak of widespread civil unrest in the U.S. The Dow remains, however, well below the all-time high of 29,551.4 reached on February 12 of this year.

FOMO NO MO'

For weeks afterward, he recalled later, the bank’s money smelled like oranges.

From a timely profile of banker Amadeo Peter Giannini. In 1904, Giannini founded a small bank, the Bank of Italy, in San Francisco. Two years later, in 1906, an earthquake struck the city and started a series of deadly fires. Giannini saved his bank's gold and cash from the fire, spiriting them out of town in a fruit cart, which left the bills durably fragrant.

The important part came next, though. Once the fires were over, Giannini brought the capital back into San Francisco, set up a table by the waterfront, and started making loans. Giannini, the child of immigrants, made those loans not “to a favored few,” but “to all the people,” in his words. Those loans, risky as they might have seemed, helped rebuild San Francisco, and won Giannini the loyalty of his customers.

Giannini's focus on smaller borrowers neglected by big institutions is shared by many of today's fintechs, and might presage similar success. By 1921, the Bank of Italy had more depositors than any in America, and in time adopted a more appropriate name: Bank of America.

THE LEDGER'S LATEST

Americans are doing something surprising with their money right now - Jeff John Roberts

The Coronavirus Economy: Bankruptcy attorneys are learning to hit 'mute' - David Z. Morris

Why Andreessen Horowitz believes so deeply in 'crypto' - Robert Hackett

Kamala Harris and Andrew Yang lead call for monthly coronavirus stimulus payments - Rey Mashayeki

Charles Schwab launches fractional shares - Lucinda Shen

Leaked documents show what Goldman Sachs really thinks of Bitcoin - Jeff John Roberts

Here's where things stand on 'round 2' stimulus checks - Rey Mashayeki

The window to use PPP loans is closing, and big issues remain unresolved - Anne Sraders

Fortune Poll: Who supports and opposes round 2 of stimulus checks - Lance Lambert

MEMES AND MUMBLES

This edition of The Ledger was curated by David Z. Morris. Contact him at david.morris@fortune.com.