The coronavirus has brought the world’s two largest economies to their knees, as two grim statistics released this past week attest.

On Thursday, the U.S. Labor Department reported that the number of Americans filing for unemployment benefits in the last four weeks topped 22 million—more jobs than the U.S. economy has created in the last nine years. On Friday, China’s National Bureau of Statistics announced that between January and March, that nation’s economy shrank 6.8%, the sharpest quarterly contraction since the tumult of Mao’s Cultural Revolution.

And yet, just as some patients infected with the virus get back on their feet more rapidly than others, the U.S. and Chinese economies likely will recover at different rates. Going into the crisis, the U.S. economy was strong—growth was steady, consumer confidence was high, unemployment neared all-time lows—while China’s economy was slowing. President Donald Trump has promised that the U.S. economy will take off “like a rocketship” once the virus is contained.

Many economists, however, expect slow to negative growth in the U.S. through the rest of this year, even as China bounces back in the second half.

“I think clearly the U.S. has a tougher time because it reacted later [to the outbreak] than China and had a less comprehensive lockdown,” says Arthur Kroeber, an economist at GaveKal Dragonomics.

Among private economists, there is a growing consensus that China’s economy will turn the corner in the current quarter. Few are predicting a V-shaped recovery in which growth snaps back as suddenly as it disappeared. But some think the country could gradually return to a pre-crisis growth rate of close to 6% in the last three months of the year.

Andy Rothman, an investment strategist at Matthews Asia argues March data from China—which show slower declines in retail sales, electricity consumption, and fixed asset investment and a sharp uptick in auto sales compared to January and February—signal China already is “on the road to recovery.”

Another sign of China’s brighter outlook: French luxury giant LVMH says sales in Louis Vuitton’s mainland stores jumped 50% the last three weeks compared to the same period a year ago. L’Oreal chief executive officer Jean-Paul Agon said Thursday that sales in China turned positive in March and will likely gain 5% to 10% this month.

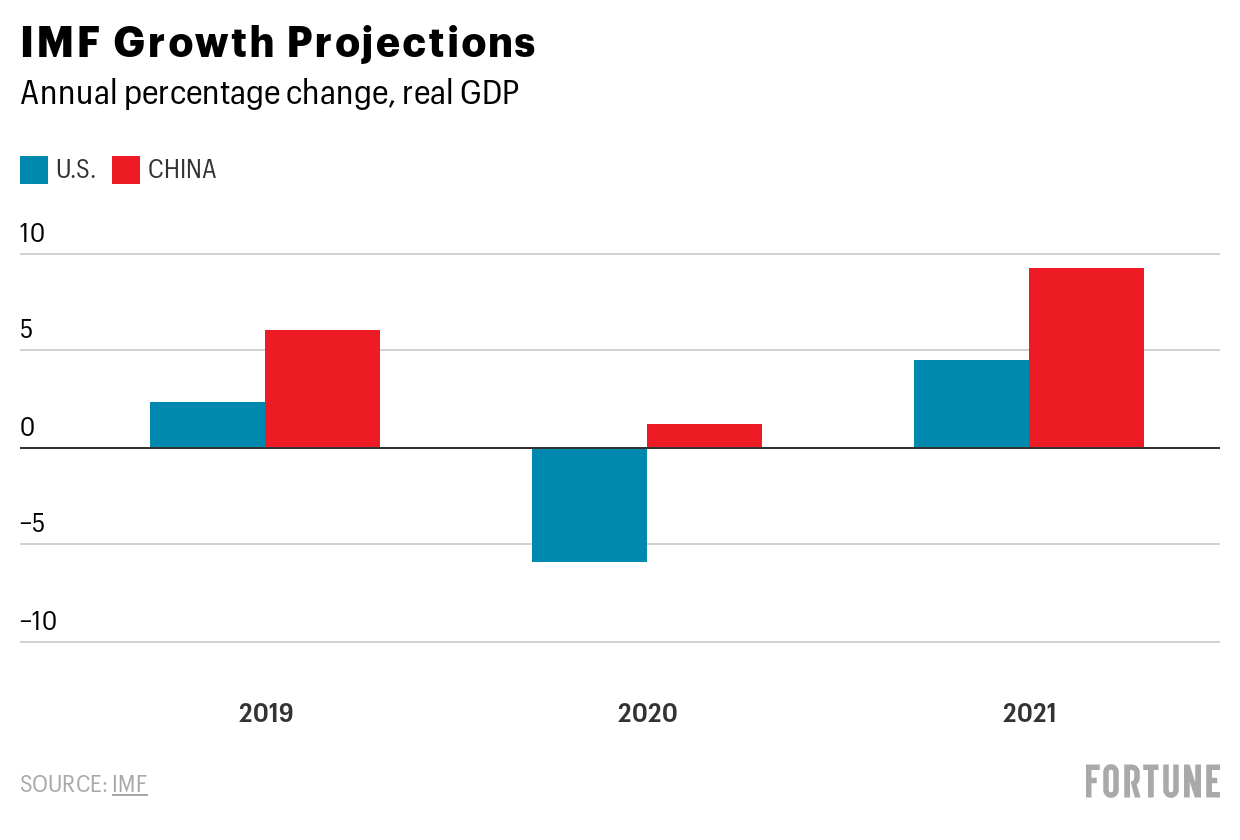

On April 15, the International Monetary Fund forecasted China’s GDP for 2020 would rise by 1.2% over last year, then gain 9.2% in 2021. The Fund predicted the U.S. economy will contract by 5.9% in 2020 before rising 4.7% in 2021. Rothman says he considers the IMF’s projections for both economies “too high, but I agree with the overall trend.”

The crisis has wiped out millions of jobs in both countries, but the employment toll appears to be much greater in the U.S. China said its urban jobless rate, which has remained about 5% for years, rose to a record 6.2% in February. (It should be noted that those figures don’t capture the plight of the millions of migrant laborers unable to return to work after China’s Lunar New Year because of nationwide quarantines and factory closures.) Goldman Sachs expects the U.S. jobless rate to exceed 15% this year, up from just 3.5% at the end of 2019. The Congressional Budget Office projects unemployment to remain at 9% through 2021.

One reason it’s easier for China to jumpstart growth versus the U.S. is that a higher percentage of Chinese workers are employed in the manufacturing sector, which accounts for about 40% of China’s GDP compared to about 11% in the U.S. “It’s much easier to restart factories than to get consumers back in the habit of going out and spending,” says Kroeber.

For leaders in both nations, the timing and trajectory of recovery pose political challenges. China’s ruling Communist Party had set an official growth target of 6% for 2020. It will be impossible for President Xi Jinping, who has asserted increasing authority over China’s economy since he came to power in 2013, to completely disavow responsibility for failure to achieve that threshold. The first quarter’s sharp decline also may force the party to abandon its pledge to double annual GDP between 2010 and 2020.

At least Xi doesn’t need to worry about re-election. For Trump, the risk is that, come voting day in November, America will be mired in a recession even as China, where the virus originated, is visibly on the mend.

If the U.S. economy flounders while China’s comes back strong, there will be geopolitical implications as well. Divergent recoveries will place greater strain on an already frayed U.S.-China relationship and undermine U.S. claims to global leadership. In recent weeks the two countries have squabbled over who’s to blame for the pandemic and jostled for influence over the World Health Organization.

Trump has called China “secretive” and sought to highlight Beijing’s failure to acknowledge the outbreak early in January when reports of the illness first surfaced in Wuhan. Chinese diplomats retorted that as China imposed an unprecedented lockdown to contain the disease, the U.S. “wasted precious time” it should have used to prepare.

However belated, China’s draconian quarantine of 60 million people in Wuhan and surrounding Hubei province appears to have succeeded in flattening the curve of new infections at a much earlier stage than in the U.S. In Wuhan, a strictly enforced lockdown lasted from January 23 to April 8. But in much of the rest of the country, restrictions were eased as early as mid-February. Rothman, in a note to clients, observes that “across most of China, life began slowly returning to normal in the second half of March.”

By mid-April, the 15-day average of new infections per day in China had dropped to around 50, down from nearly 4,000 at the peak of the outbreak in mid-February. In the U.S., the 15-day average for the period ending April 15 showed signs of slowing, but exceeded 30,000. By early Sunday, China had reported roughly 84,000 total infections with 4,700 deaths, while the U.S. had some 735,000 cases with 39,000 deaths.

So far Xi has shown no inclination to repeat the kind of massive stimulus measures his predecessors used to bolster growth after the Global Financial Crisis. Policies China has announced in response to the pandemic account for only about 3% of GDP, according to Bloomberg Economics, compared to 10% and 20% for Washington and Tokyo, respectively. That earlier spending spree pushed China’s debt-to-GDP ratio to more than 300%.

But even without such budget-busting, China remains the “world’s best consumer story,” according to Rothman, and likely to remain an attractive designation for multinationals and global investors.

More coronavirus coverage from Fortune:

—Saving a city: How Seattle’s corporate giants banded together to flatten the curve

—How Fortune 500 companies are utilizing their resources and expertise during the pandemic

—Inside the surreal “Mask Economy”: Price-gouging, bidding wars, and armed guards

—Researchers working on “contact tracing” say they welcome Apple and Google’s help

—How every sector of the S&P 500 has been impacted by the coronavirus selloff

—If you’ve been a little busy lately, here’s what’s going on with the 2020 election

—Looking for a travel refund? Here’s what airlines, hotels, and theme parks are offering

—PODCAST: COVID-19 might have upended the concept of the best companies of the year

—VIDEO: 401(k) withdrawal penalties waived for anyone hurt by COVID-19

Subscribe to Fortune’s forthcoming Eastworld newsletter for expert insight on what’s dominating business in Asia.