Past performance, it turns out, is no guarantee of future results. After years of comparing the performance of his Berkshire Hathaway to the S&P 500, Warren Buffett is seeing exactly that.

As of November 14, Berkshire Hathaway shares were up 8.3% year to date. Sounds pretty good—till you calculate the S&P 500 was up 23%.

Buffett has long used the S&P 500 as a benchmark for his efforts and those of his partner Charlie Munger. Buffett’s latest annual letter to shareholders, which came out in February 2019, starts with a comparative table of Berkshire Hathaway and S&P 500 performance since 1965.

But a current rout doesn’t mean the “Oracle of Omaha” has lost his touch. A Fortune analysis of performance since Jan. 2, 2008 found Buffett stays ahead in the long run. Plus, in the back-and-forth of who’s on top, investors can learn some important lessons.

The S&P 500 hurdle

Measuring the strength of any investment strategy needs a benchmark, and the S&P 500 index can be a taskmaster. One study looked at a 15-year period ending with 2016 and found the S&P 500 beat the bulk of funds: 92% of large-cap funds, 89.3% of mid-caps, and 85.5% of small-cap.

So-called passive funds passed a milestone in September 2019. For the first time, investors had more money in U.S. index funds and ETFs than actively managed mutual funds.

Most people probably can’t beat the market. But the fiscally ambitious try. Buffett and company often succeed, using the S&P as a touchstone to test their strategies.

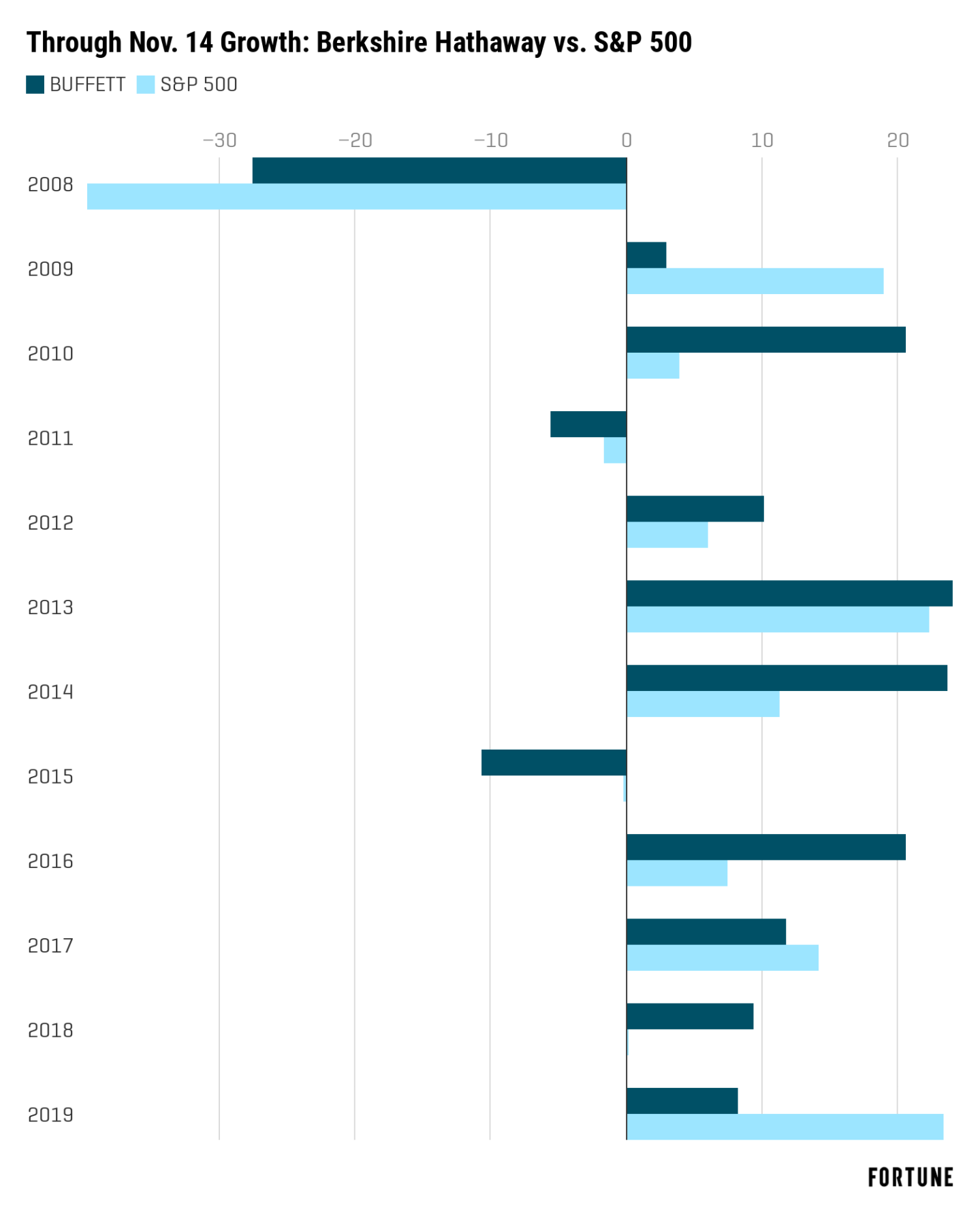

Buffett vs. S&P 500 since the Great Recession

Instead of going back to 1965, consider the performance from 2008—the full start of the Great Recession—through 2018.

During this period, Berkshire Hathaway outperformed the S&P index in eight years, or almost 73% of the time.

Fortune also analyzed the performance of both through Nov. 14 of each year. (When the date fell on a weekend, Fortune chose the next weekday the markets were open.) From 2008 through 2018, there was only one year, in 2017, when Buffett trailed the S&P 500 on Nov. 14 but was able to outdo the index by year’s end.

5 factors weighed on Berkshire’s 2019 performance

As the chart below shows, while Buffett has had a good 2019, the S&P 500 has had a great year through mid-November.

Several factors are contributing to the gap in performance:

Focus on cash

“Buffett maintains a huge cash position—nearly $130 billion—which represents [roughly] a quarter of the entire market cap of Berkshire Hathaway,” says Tim Bain, president and chief investment officer at Spark Asset Management. Cash isn’t appreciating in value as fast as stocks, but that doesn’t deter Buffett, who will leave it parked rather than invest it in a way he deems unwise.

Distaste for tech

“Berkshire has been slow in investing in tech, and high growth companies as the investors’ appetite for risk and ultra-low interest rates have pushed the markets up in the last decade,” says Stoyan Panayotov, founder of Babylon Wealth Management.

One bad bet

Then there’s Kraft Heinz. It is one of Berkshire Hathaway’s largest holdings, and it “lost 25% of its value in February,” says Matt Ahrens, chief investment officer at Integrity Advisory.

Lagging financials

“One of his largest concentrations is in the financial sector—largely banks and insurance companies—and, until recently, those sectors have been out of favor,” says Robert Johnson, professor of finance at Heider College of Business of Creighton University and a 35-year-long Berkshire shareholder. That slowed performance. Many of Buffett’s holdings in this sector “are selling at a discount of almost 50% to the market.”

Book value

The fifth, and more complicated, factor is Buffett’s long-held emphasis on Berkshire’s book value—the bottom-line worth of the company, determined by subtracting liabilities from assets. With low interest rates, the asset values as calculated by book value don’t grow quickly enough for investors, who want growth. Book value has fallen out of favor, as a result, and investors don’t want to pay as much for Berkshire shares. Berkshire’s reliance on book value—and investors cooling on the metric—is a big reason the S&P 500 has grown faster than Berkshire shares, notes Tony Scherrer, director of research and portfolio manager at Smead Capital Management.

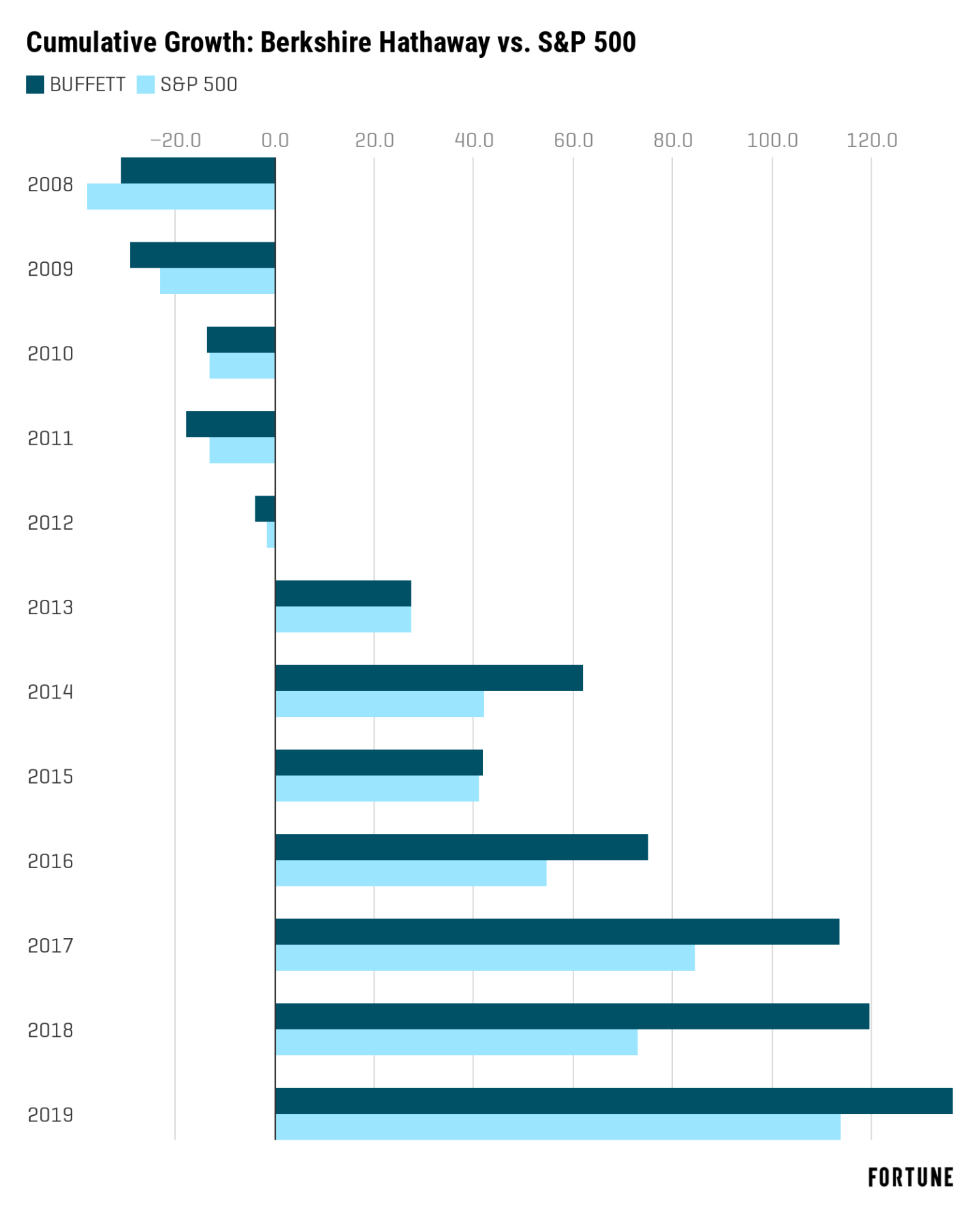

Still, 2019 is only one year and looking at such a short period is an act of misdirection. The question ultimately comes down to who does better in the long run. Here is another chart that shows cumulative multi-year growth from Jan. 2, 2018 through the end of each year (for 2019, it’s through mid-November)—in other words, the collection of all the gains and losses between 2008 and a given year.

Even with some down years, Berkshire Hathaway shares have seen significantly greater growth in the long run than the S&P 500. From 2008 through 2018, the company saw cumulative growth of 119.7%, versus 73.2% for the S&P 500. And even with the boost the S&P has seen so far this year, the growth from 2008 through mid-November of 2019 is 114%. For Berkshire, it’s 136.4%.

And, the smart money has learned never to count Buffett out.

“In the last Barron’s issue in 1999, Andrew Bary wrote a cover story entitled ‘What’s Wrong Warren?'” Johnson says. “The article contended that Buffett’s lack of expertise in technology stocks was leading to his demise. We all know what happened: The dot com bubble burst and Berkshire was well positioned.”

The bottom line, according to Johnson? Don’t bet against the Oracle of Omaha.

More must-read stories from Fortune:

—The S&P 500 may be due for a 25% correction, according to historical data

—The 2020 tax brackets are out. What is your rate?

—How “VSCO Girls” are killing makeup sales

—What is “quantitative easing”—and why is everybody so worked up about it?

—A.I. vs. the wolves of Wall Street

Don’t miss the daily Term Sheet, Fortune’s newsletter on deals and dealmakers.