Some time ago, at the height of the Great Recession, I asked a senior central banker what impact he thought the financial crisis of 2008–09 would have on the future of monetary policymaking. Back then, Ben Bernanke and his colleagues at the Fed were on the defensive, their reputations in tatters. For the second time in a decade they had missed the formation of an asset price bubble, which eventually burst and dragged the economy into a recession. Surely things would now be done differently, I suggested. Rather than obsessing over inflation, which they’d been doing for decades, central bankers would start to focus on more pressing problems, such as preventing bubbles and raising living standards.

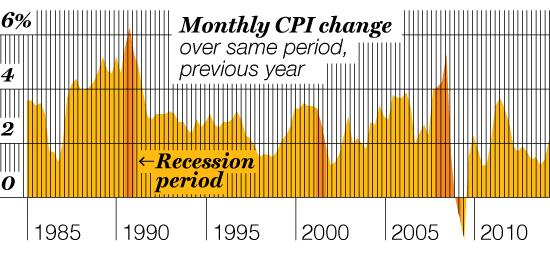

My interviewee smiled. “I think we’ll end up giving inflation targeting one more go and supplement it with stiffer regulation,” he said. “If it fails again, then you might see a big change.” That skepticism turned out to be well-grounded. According to the latest CPI figures, inflation is running at the terrifying rate of 2%—precisely the same rate it was at a year ago. But some Fed policymakers and a legion of Fed watchers are consumed with the supposed threat of higher inflation.

When Janet Yellen, Bernanke’s successor, spoke at the annual Fed conference in Jackson Hole, Wyo., a few weeks back, analysts and journalists dissected her speech for indications that she, too, was getting worried about rising prices and might therefore be prompted to start raising interest rates more quickly than Wall Street was expecting. Some observers claimed to have seen signs of hawkish tendencies emerging in the Fed chair: At one point in her speech, she cited a research paper that implied wage inflation might start to pick up from here. Other analysts highlighted Yellen’s more dovish statements, in which she pointed out that the labor market still hadn’t fully recovered from the Great Recession.

The confusion was understandable. With economic indicators sending mixed messages about how fast the economy was picking up, Yellen was deliberately speaking out of both sides of her mouth. She’s made clear all along that her main emphasis is boosting job growth and repairing the damage done by the slump. But with the Fed committed to keeping inflation from rising above 2%, and with some of her hawkish colleagues on the Federal Open Market Committee already dissenting from her policies, Yellen evidently felt it necessary to maintain the Fed’s inflation-fighting credibility by hinting at the possibility of an early rate rise.

But where exactly is the inflation threat? Thanks to Moore’s law, the flood of cheap imports from China and elsewhere, and the decline of trade unions, it has largely disappeared. The last time the U.S. economy experienced a scary wage-price spiral was during the late 1970s—two generations ago. Since 2010 the Fed’s favored measure of inflation—the PCE (personal consumption expenditures) deflator—has risen at an annual rate of 1.7%. This time last year, some analysts were fretting about deflation.

The latest inflation scare makes no sense. Median incomes have stagnated for decades, and we could actually do with a bit more wage inflation. Despite the recent pickup in hiring, wages are still rising more slowly than productivity. Unit labor costs are declining, and corporate profits are surging. But that means firms could afford to pay higher wages without passing along all the increase in costs to consumers. We might get a bit more price inflation, but it would be worth it. There is nothing in economic theory, or economic history, to suggest that a period of, say, 3% inflation is harmful to an economy.

As a first-rate academic economist, Yellen knows all this well. But she and her colleagues are trapped inside an inflation-

targeting framework that was designed to deal with the problems of the 1970s and 1980s. Since then we’ve been through two entire economic cycles with no sign of rampaging inflation. The Fed is still fighting the last war.

John Cassidy is a Fortune contributor and a New Yorker staff writer.

This story is from the September 22, 2014 issue of Fortune.