Private equity fundraising is on the rise. So are private equity deal prices (or at least deal multiples).

The temptation, judging by several recent articles, is to assert causation. Private equity firms are raising more money, so they are under more pressure to deploy capital. The fund size dog wags the deal size dog, likely resulting in disappointing returns. No wonder certain large institutional investors — like the California Public Employees’ Retirement System (CalPERS) — are cutting their allocations to private equity.

But the numbers don’t really back up this argument.

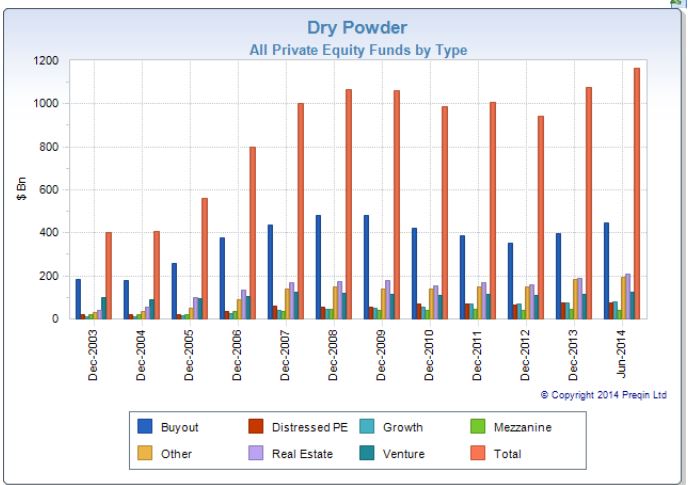

First, let me stipulate that private equity “dry powder” (i.e., undeployed fund capital) is currently at an all-time high of around $1.17 trillion, according to Preqin. This includes not only buyout dry powder ($442b), but also things like real estate private equity ($210b) and venture capital ($126b):

This is around 12% more dry powder than the private equity market has had, on average, over the past seven years, and an 8% increase from just this past December. At the same time, however, private equity investment is not growing at anywhere near the same rate.

For example, private equity deal volume in 2014 (by dollars) currently is on pace to virtually mirror 2013. It also would come in around 12% below 2005 deal volume, despite there being 19% more dry powder. And as whopping 65% below 2006 deal dollar volume, when the dry powder-kegs were $100 billion or so lighter.

In other words, available private equity dollars do not directly translate into private equity deals. Remember, these funds typically have at least five years to deploy initial capital commitments. There is no immediate rush, particularly in the midst of bull public markets that have raised prices across the board (something private equity firms can sometimes combat, at least theoretically, by using cheap leverage). Buyout execs pay a lot of lip service to lessons learned from the financial crisis, but the reality is that massive take-privates — particularly ones that involve multiple sponsors — have become a rarity.

As for those institutional allocation decisions, a lot of it seems to be more about reverse denominator effect than about future ROI concerns. For example, a 14% target private equity allocation at CalPERS today would represent around $41 billion in real dollars. Just two years ago, that same 14% target allocation would have been worth $33 billion. Many of these big institutions got stuck in a reverse denominator effect during the financial crisis, and are prudently resetting allocations so that they don’t risk a repeat situation.

Moreover, many allocations were formulated based on pre-crisis fundraising environments that were much busier than even today’s revived market (i.e., there isn’t enough supply to satisfy demand). CalPERS, for instance, was well short of its 14% allocation even before lowering it — suggesting that its rejiggering was as much about reflecting reality as it was return objectives.

To be sure, none of this is to asset that returns from the 2014 vintage of private equity funds will outperform. Indeed, history shows that the best ROI comes from funds raised when the overall economy and financial markets are sluggish. But all of the hand-wringing over fundraising and deal volume seems to be… well, overwrought.

Sign up for Dan Primack’s daily email newsletter on deals and deal-makers: GetTermSheet.com