Is the American middle-class dream dead? The so-called economic recovery, in progress since 2009, has produced little in the way of real wage growth for most Americans. Fewer have jobs, and the median income of those who do is 4.4% lower than when the recession supposedly ended.

Meanwhile the stock market has doubled and the S&P 500 has set new highs, crossing 1,900 for the first time in May.

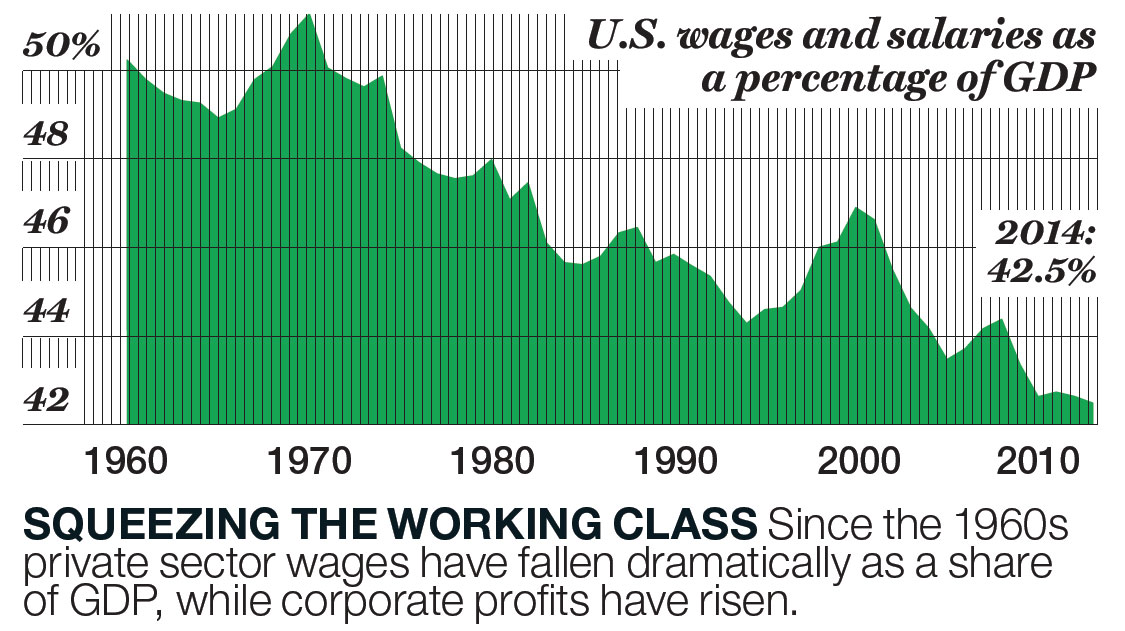

Those reaping the benefits of outsize capital gains and dividends will tell you that it’s not their fault — that this triumph of capital over labor is the inevitable outcome of globalization and technology. Democrats, always adept at identifying the right issues and offering the wrong solutions, want to address the problem through income redistribution in the form of higher tax rates. But before we raise tax rates (again), perhaps we should tackle the policies that are hurting working families in the first place.

Prior to the crisis, both parties embraced globalization as a positive for our economy, without facing up to the inevitable negatives for our workforce. They “financialized” our economy, trying to make up for declining real wages with easy credit, and relying on asset inflation (tech stocks, housing) to generate growth. Even after the financial crisis proved the folly of that model, we are still trying to use it to restart our economy.

The Fed can open the monetary spigot, but it can’t force the economy to drink. Structural reforms are necessary to stimulate real economic demand and bring home more and better-paying jobs. We will never compete with Bangladesh in labor costs (and shouldn’t), but there are other ways to attract job-producing enterprises: modern infrastructure, a well-trained workforce, a fair, efficient tax code, and (ahem) effective political leadership.

Yet making our economy more competitive is the last thing on Washington’s mind. With elections six months away, the White House is pressing the wedge issues of its party faithful, while Republicans stir up their red-meat eaters by launching another inquiry into Benghazi (yawn). Meanwhile America’s competitive edge is becoming as dull as the last Spider-Man movie.

Look at the skills gap. Our young people lag behind most developed countries in math and science, yet we lead pretty much everyone in education spending. But Washington still focuses on how much we spend, not how we spend it. For instance, why not offer a break on student-loan repayments for kids who want to become machinists and technicians? On immigration policy we lead with our hearts, not our heads, giving priority to immigrants with family relations over job-producing Ph.D.s.

Our decaying infrastructure is a national disgrace, routinely imposing costly disruptions in communication, power, and transit. With financing costs at historic lows, why aren’t we making long-term investments in modernizing our infrastructure and, in the process, creating good-paying skilled jobs?

Our personal and corporate tax codes are riddled with special breaks that distort economic activity. Capital-gains breaks favor investors over workers. Debt subsidies encourage leverage. Uncompetitive corporate rates provide incentives to do business overseas. So IBM (IBM) gooses its share price by issuing debt to pay for dividends and share buybacks. Pfizer (PFE) pursues AstraZeneca because it can pay lower U.K. corporate rates. These days executives seem more interested in pursuing profits through tax arbitrage than producing stuff that people want to buy.

Education and immigration reform need not cost money. Much infrastructure repair can pay for itself through tolls. And tax reform, if done right, can raise revenue. These are all fiscally responsible measures that have bipartisan support. They will make our economy more competitive and reverse the decline of the middle class. President Obama needs to decide if he is the “Yes, we can” or the “It’s too hard” President. And Congress needs to work with him to get the job done.

Fortune contributor Sheila Bair is former chair of the FDIC.

This story is from the June 16, 2014 issue of Fortune.