When the business world woke up on Jan. 21 and heard about the White House’s overnight announcement — that General Electric CEO Jeffrey Immelt would become chief of the Council on Jobs and Competitiveness — the buzz quickly focused on just one question: Was he leaving GE? Was the long-standing speculation that he was seeking a way out — a “graceful exit,” as a blogger had put it — proving true? No, was the answer. But the fact that everyone asked the same question that morning is a message, the world’s grim verdict on Immelt’s tenure so far: not good.

It’s been almost 10 years since Immelt took the helm from the legendary Jack Welch, and this anniversary year invites particular scrutiny. GE (GE), like the economy, is just emerging from some hellacious years; in the depths of the financial crisis, the stock fell briefly to its lowest level since 1991. This year is also the midpoint of Immelt’s presumed two-decade term as chief, an extraordinary stretch of runway; the average big-company CEO gets just 6.3 years, says Booz & Co. Like Welch, he got the job at age 45 so that, like Welch, he’d have 20 years to put his stamp on one of the world’s most admired companies.

So how has he done?

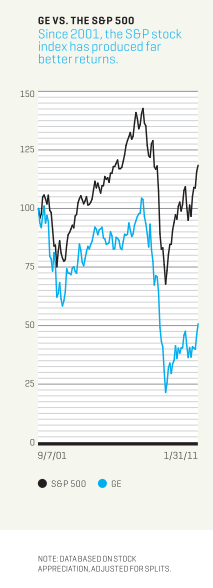

Plenty have called for his head. A “disaster” is the description used by MarketWatch columnist Brett Arends, Seeking Alpha columnist Steven Towns, and many stock market bloggers. But no major shareholder has attacked Immelt publicly. No proxy advisory firm has told clients to vote against him as a director. The board is officially mum, but people close to the directors say he still has their confidence. Director A.G. Lafley, Procter & Gamble’s (PG) former CEO, is showing his support in the sincerest way: SEC filings show that in January he bought 25,000 shares of GE. Still, Immelt’s record isn’t one that anybody, not even this board, would want. When he got the job on Sept. 7, 2001, GE stock was $40 a share. Almost 10 years later, it’s around $20. The company’s credit rating was AAA, the best, awarded to only a handful of enterprises; no more. It was the most valuable company on earth, commanding the highest market capitalization. Today it’s about No. 8 (its rank varies day by day), just behind Royal Dutch Shell.

For years GE stood consistently at or near the top of Fortune’s Most Admired Companies list. It’s No. 16 in the latest ranking and hasn’t been No. 1 since 2007. In Universum’s ranking of the companies where business students most want to work, it’s No. 27, down from No. 8 just three years ago. That loss of stature could hurt GE for years. “I had never realized what an advantage it is to be the most admired corporation in the world,” says Nicholas Heymann, an analyst at Sterne Agee and a former GE employee who has covered the company for decades, “and to attract the best and brightest people in the world.”

A record of decline, mistakes, and wealth destruction? Yes. A slam-dunk case for throwing the bum out? Not exactly. The difficulty in judging Immelt is that, observed today and gauged by the standards of normal companies, GE looks pretty good. To be among the 10 most valuable companies on earth, among the 20 most admired, and among the 30 most desired employers — most companies would kill for that. Since bottoming on March 4, 2009, the stock has more than tripled. Last year the company earned $11.6 billion of profit, probably ranking in the top 25 globally. Immelt has made some smart divestitures, such as selling GE Plastics to Saudi Basic Industries for $11.6 billion in 2007. GE got out of subprime mortgages in 2007 (at a deep loss, but hanging on would have been far worse) and exited insurance before that sector cratered. Though the company’s mammoth GE Capital unit suffered huge reversals in the financial crisis, it never lost a dime. GE didn’t have a losing year or a losing quarter.

You could even argue that the stock’s miserable run under Immelt isn’t nearly as bad as it looks because the price was irrationally high when he got the job. At $40, it was still coming down off its bubble market peak of $60. Number crunching by the EVA Dimensions consulting firm shows that the $40 price meant that investors were expecting GE’s economic profit (earnings after a capital charge) to increase by some $3 billion a year for 10 years and then hold at that level; the company’s economic profit would now be about $40 billion a year and expected to stay there forever. Such an expectation was nuts. The highest economic profit ever achieved (excluding super-major oil companies, whose numbers were briefly skewed by oil price spikes) was Microsoft’s (MSFT) $15 billion in 2007. At GE last year the figure was $3.9 billion. If the stock had been priced more sanely — $20 would have been realistic, even without knowing that 9/11, a financial crisis, and a recession lay in the future — and one then considers the dividends GE has paid to investors, Immelt’s performance vs. the market looks respectable.

But still — after 10 years it’s tough to make excuses based on the hand you were dealt (and Immelt has never publicly done so). GE is not a normal company. It’s one of the treasures of American industry, the company founded by Thomas Edison and a management academy whose former employees run top companies worldwide. Even if GE looks good by normal standards, it is much less than it was, and its decline is bad news for employees, suppliers, customers, and communities. So the question of how the company under Immelt got to its current state is big. And answering it is important.

Allocating capital

Welch used to say that GE’s CEO has only two jobs: allocating capital — deciding where and how much to invest — and evaluating people. Ask a wide range of expert GE observers — current and former managers, other top-tier CEOs, Wall Street analysts — to identify Immelt’s wrong turns, and they focus on exactly those two categories.

When the question is posed to analyst Nicholas Heymann, the first words out of his mouth are “capital allocation.” As several analysts point out, that task becomes especially critical if the CEO is pouring boatloads of new capital into the business. When Immelt became chief, GE had about $42 billion of capital invested in it, an amount that had grown only slightly over the previous few years (data from EVA Dimensions). Just three years later, the amount had tripled to $126 billion. By 2009 it had almost quadrupled to more than $163 billion. Those numbers include GE’s debt, equity, and capital from other sources, such as retained earnings, plus the equity portion of GE’s investment in its giant affiliate, GE Capital. They don’t include the amounts that GE Capital borrowed on its own, which also ballooned. GE Capital had $240 billion of what it calls “borrowings from others” in 2001, the year Immelt became CEO. By 2008 that amount had increased to over $500 billion.

There’s nothing wrong with putting new capital into a business. In fact, as long as the return on that capital is greater than the cost of capital, it’s a great strategy for creating value. The danger is that if anything goes wrong — if the return on capital falls even a little below the cost — the value destruction can be immense because so much capital is in play. Even if that doesn’t happen, which it hasn’t so far at GE, the risk that it could happen dampens investors’ enthusiasm for the stock.

Immelt put much of that new capital into buying businesses. Unlike most companies, GE is an ever-changing portfolio, and the essence of strategy there is deciding which businesses to be in. Like all new GE chiefs, Immelt remade the portfolio, expanding aggressively into industries of the future — green energy, water, health care. Most of those investments have not yet produced knockout returns. He made a major acquisition in 2004, buying 80% of Universal (movies, TV shows, theme parks) from Vivendi for $5.9 billion and combining it with GE’s NBC unit. Then he bailed out of the whole thing, selling a controlling stake to Comcast in a deal that closed in January.

Though spending big on acquisitions, Immelt was putting much more into GE Capital, the multipart business that was producing 40% of GE’s profit when Immelt took over and would soon produce even more.

For a while it all seemed to work. GE stock rose steadily from early 2003 until the autumn of 2007. Then, at the earliest signs of the wheels coming off the financial system, Immelt’s heavy move into GE Capital turned against him. When the investing world decided it hated everything financial, nothing could save GE stock. GE Capital’s profit plunged and is still nowhere near recovering; commercial real estate loans, the black hole, lost $1.5 billion in 2009, $1.8 billion last year, and will lose hundreds of millions this year. At the most acute moment of the crisis, Immelt had to ask Warren Buffett for $3 billion, on which GE must pay a hefty 10% dividend; that rescue package can’t be repaid before this autumn, after which GE would have to pay Buffett a 10% premium to close out the investment.

Immelt says he learned his lesson and doesn’t want GE Capital to be such a big part of GE; it should provide about 30% to 40% of the company’s total profit, he has said. The company can point with pride to GE Capital’s much reduced share of total GE profit today (about 25% last year), but that’s making a virtue of necessity. The real issue, now as always, is capital allocation, and GE Capital still carries almost a half-trillion dollars of debt, supported by equity from the parent. We’ll know the importance of GE Capital has actually shrunk when the capital devoted to it meaningfully retreats.

Wise capital allocation is also about deciding where to take capital out. Immelt waited too long to sell NBC Universal, which was valued at $30 billion in his deal with Comcast; earlier in the decade analysts had estimated the business was worth $40 billion or more. Immelt clearly waited too long to try unloading the lighting and appliance businesses and as a result still hasn’t shed them; plans for auctions or spinoffs got bulldozed by the recession.

People evaluation

The other main category of Immelt criticism — people evaluation — is impossible to quantify but comes through loud and clear. For GE, even more than for most companies, it’s critically important. When Immelt was asked soon after becoming CEO to name GE’s core competency, he immediately responded, “Evaluating people.” It was exactly the same answer Welch had given to the same question years earlier. Because GE’s businesses change over time, the company realized long ago that its most important product is excellent managers, and it has developed the world’s most rigorous and emulated processes for producing them.

Some insiders and CEOs of other companies believe that Welch’s stringently demanding criteria and processes have been eased and that the change is hurting performance. Most famously, Welch’s requirement that the worst-performing 10% of employees be moved out every year has been rescinded. In addition, several sources say that GE’s strict accountability for delivering results has weakened. “He changed the performance evaluation criteria,” says the CEO of a major company, who doesn’t want to be identified because of his firm’s relationships with GE. “It’s now too qualitative. There’s not enough attention to the bottom line.” GE strongly disagrees. “Everything we do is still about performance,” says a spokesman. “We still identify people who underperform and take action to help them improve or move them out. The focus on people and investment in people have only increased.”

Any hit to GE’s awesome people advantage would be a major long-term problem. Only a couple of high-level stars have left: David Calhoun became CEO of Nielsen in 2006, and Joseph Hogan in 2008 became CEO of the Swiss company ABB, a GE competitor. We don’t hear much about other GE executives below the CEO largely because no succession race is on. But Wall Street is worried that good executives could depart because pay at the top is heavily stock-based. “The biggest risk at this point is that people start to leave,” says Heymann of Sterne Agee. “They’ve heard the word mañana too many times.” He believes that’s one reason the company increased its dividend twice last year, which helped push the stock up.

Getting the stock up further, Immelt’s most pressing financial priority, won’t be quick or easy. His strategy is to refocus GE on its huge industrial businesses, investing much more heavily in R&D than was done under Welch. It’s a long-term strategy, a ground war that by its nature will take years to prove successful.

Another weight on the stock is Immelt’s own reduced credibility. It suffered massively in early 2008 when he announced that GE’s first-quarter earnings were solidly on target, then revealed just 18 days later that GE had missed its targets — at a company famous for never, ever missing its targets. That’s when Welch controversially said on GE’s own CNBC that he’d “get a gun out and shoot [Immelt] if he doesn’t make what he promised now.” Many observers have criticized Immelt for being too optimistic through the crisis. “Jeff has gotten himself into a bit of trouble over the years and lost credibility because he’s a marketer and is always at the upper end of the range,” says a former GE executive. Investors have long memories. That’s why Morgan Stanley analyst Scott R. Davis was still telling clients last fall, “Management credibility will take time to correct.”

The competition heats up

A further challenge for the future: GE is no longer as competitively dominant as it used to be. Munich-based Siemens (SI) in particular has risen to challenge GE in virtually every business and is performing strongly. Its stock has more than doubled during Immelt’s tenure (see chart below). It holds a multidecade headstart in China, a market GE is counting on for future growth. It’s also run by a former GE executive, Peter Löscher, who brought with him intimate knowledge of GE’s plans, methods, and weaknesses.

Meeting all those challenges is a major operational job for Immelt. As a former executive observes, “He’s got a ton of work to get that behemoth machine back on track and producing.” But he also faces a more ephemeral task that’s at least as important.

When GE watchers talk about what has happened to the company, they use many different words to name something the company has lost: “the halo,” “the luster,” “the golden image.” The accepted notion that GE somehow stood above ordinary companies gave it a powerful advantage with all its constituencies. That’s gone, a symbol of GE’s overall experience since the boom ended in 2007. Times of tumult are when the competitive order shifts in ways that last for years. Some companies come through the trauma stronger, others weaker. GE has come out weaker. We cannot know whether the board will conclude that Immelt has learned from experience and is GE’s best leader for the future. But judged rigorously on what he has delivered — the GE way — he has not made a strong case for 10 more years.

Also on Fortune.com:

Obama and business, frenemies forever?

{kind=link}