In the context of current economic headwinds, money managers and investors grapple with tough decisions about where to invest and how to maintain a diversified and well-performing portfolio. Companies in sectors experiencing “hyped” valuations are at a greater risk of losing value in a market correction. Meanwhile, early-stage venture investments in essential sectors such as healthcare and industrial production can provide shelter from stormy markets by focusing on disciplined capital formation, long-term value creation, and the potential for outsized returns.

Early-stage investors are more likely to be in a position to set attractive valuations that can achieve returns-driving ownership, regardless of market context. Venture investors who lead early rounds (typically seed) and set valuations can leverage that role to buffer themselves, their LPs, and their companies from unhealthy market swings.

Pitchbook analysis of seed-stage investing shows a remarkably consistent equity stake available to investors coming in at seed (typically first) financing rounds. This is consistent with our own experience at Genoa Ventures, where our mantra of “double-digit ownership with single-digit checks” has borne out consistently since its inception in 2018.

This longitudinal data supports the idea that early-stage investors are relatively buffered from extreme market-driven valuation swings.

An early-stage venture capital investor aiming to deliver returns to LPs on a typical seven-to-10-year VC timeframe must bring a long-term perspective to day-to-day investing decisions. Market conditions will inevitably go through rocky periods in the relatively long lifetime of a venture portfolio company or fund. By keeping in mind–and helping portfolio companies be aware– that storms are a matter of when, not if, we can take steps to prepare for times when waters become choppy.

An early-stage investor is intimately familiar with the art of doing more with less–creating value with scarce capital while threading the needle of early-stage valuation discipline. When investing in and supporting our portfolio companies, the emphasis needs to be on capital-efficient risk retirement and long-term value creation. This means encouraging our portfolio management teams to right-size financing rounds and focus spending on priority value-creating activities while keeping a close eye on cash position, operating runway, and cash-out dates.

It also means working with our companies to develop a range of financing options and contingency plans. An early-stage investor must bring a clear-eyed understanding of the risks associated with follow-on financing for portfolio companies. Capital may not always be available on ideal timelines or desirable terms. Letting a company’s valuation get ahead of its actual stage, while tempting in the short term, can derail its long-term capital journey.

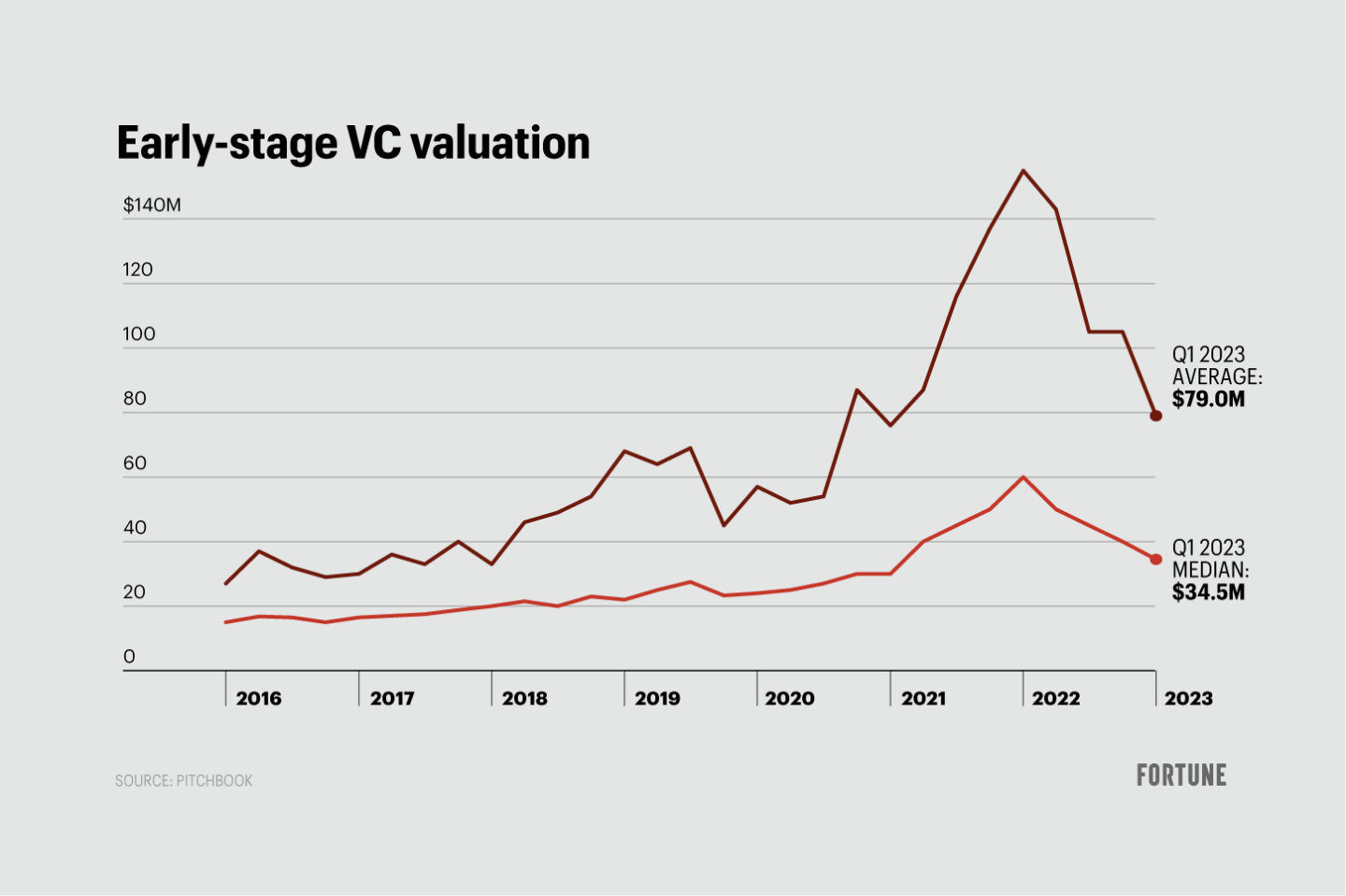

Upward valuation pressures peaked in 2021. Specific sub-sectors or trendy investment themes experiencing a high level of “hype” and competition for deals make headlines and run the risk of valuation inflation. However, average valuations tend to be driven by outlier values in a small proportion of deals. Meanwhile, the vast majority of early-stage deals not currently in the spotlight anchor the more consistent median values of the asset class, priced more appropriately for risk.

Essential industries such as healthcare, agrifood, and bio-based production can offer some attractive early-stage opportunities for investors with longer investing horizons. Deal competition is lower on average in these sectors–so startups tend to garner lower initial valuations and early-stage value inflections than their technology and retail counterparts.

While these companies typically do not benefit from hype cycles that can lift valuations, their focus on developing products that address unmet human needs can result in real, tangible value creation as they retire risks and hit milestones. The need for more and better medicines and food, and the basic research that fuels these innovations, never ceases. Some businesses in these essential sectors, such as research and development (R&D) tools companies, have journeys that are relatively less capital intensive, meaning they can better manage their cash needs to adjust to market environments.

Mergers and acquisition (M&A) opportunities, the more typical exit option for product-centric startups in these industries, are available for innovations that can impact top lines and expand strategic options for larger acquirers. With lower early-stage valuations, capital efficiency, and robust exit options, such investments may not be as subject to the valuation swings of uncertain markets and can provide shelter in a diverse portfolio.

By contrast, some sectors may be more subject to boom-and-bust market dynamics, even for early-stage investors. For example, startups that depend on consumer sentiment and discretionary spending are likely to be harder hit in market downturns than those offering essential goods and services. Seed-stage pitches that are more story than substance may play well during a bull run, but those same companies can struggle to raise follow-on capital at attractive valuations when bear-market investors begin to prioritize concrete milestones and performance indicators.

The risks we know we are up against every day as early-stage investors–product and market risks, financing risk, externalities over time–meaning we’re always attending to the priorities that we hear other investors now emphasizing: runway, milestones, quality, and access to capital.

Success in an early-stage investing strategy requires us to maintain a very high bar in selecting exceptional portfolio companies and to focus on the fundamentals of company-building and value creation. We can weather the storm by taking a long-term perspective that transcends temporary disruptions.

Jenny Rooke, Ph.D., is the founder and managing director of Genoa Ventures.

The opinions expressed in Fortune.com commentary pieces are solely the views of their authors and do not necessarily reflect the opinions and beliefs of Fortune.

More must-read commentary published by Fortune:

- The return to the office could be the real reason for the slump in productivity. Here’s the data to prove it

- Overconfident tech CEOs have overpaid for ‘box tickers’ and ‘taskmasters.’ Here’s why the real ‘creators’ will survive the mass layoffs

- How the Russian economy self-immolated in the year since Putin invaded Ukraine

- I am a DoorDash driver who’s been elected to the Colorado State House. Food delivery companies are gamifying your tips and making it harder for drivers to earn a living wage. Here’s what you can do about it