Strolling into your local Rite Aid, there’s not much that separates the store from those of its biggest competitors, CVS and Walgreens. All the standard chain-pharmacy building blocks are there: rows of shampoo and painkillers, a snack aisle filled with brightly colored bags of potato chips, the “seasonal” section, stocked with plastic pumpkins or maybe pastel Easter baskets, and, of course, the pharmacy counter, usually tucked away near the back.

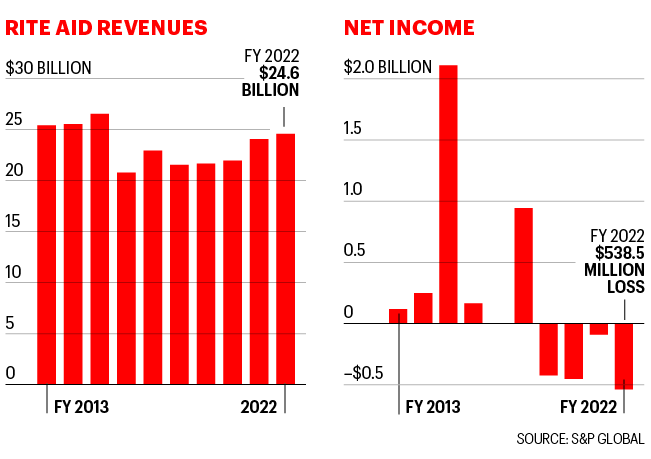

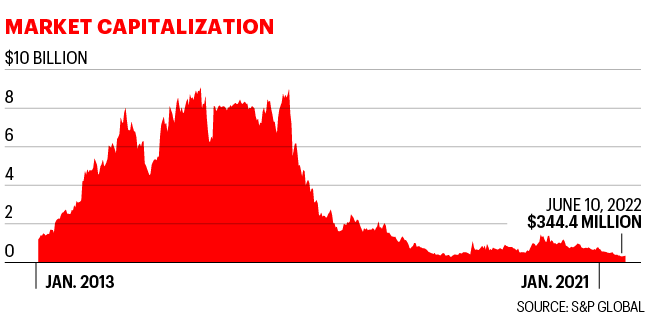

But broaden the picture and that facade of similarity crumbles. Rite Aid, which was once the largest pharmacy chain in the country, is now just a minnow in the Big Pharmacy pond. The company lost more than $539 million last year and is struggling to hold on to a market cap of about $350 million (on par with comparatively tiny, struggling consumer products maker The Honest Co). Meanwhile, CVS has grown into the fourth largest U.S. company by revenue on the Fortune 500, bringing in $8 billion in profit last year on revenue of $292 billion (nearly 12 times as much as Rite Aid’s). CVS’s market cap: nearly $122 billion. Walgreens, while not quite as massive, still dwarfs Rite Aid, with nearly $150 billion in 2021 revenue and $2.5 billion in profit.

Rite Aid’s financial difficulties are far deeper and more perilous than simply looking puny compared with its competitors. The company is also dragging around $3 billion in debt—one reason that an April Deutsche Bank research note warned that the company was in danger of hitting a “dramatic negative inflection point” where it no longer has the funds to invest in the business. What happens if it reaches that point? A downward spiral that could potentially end in bankruptcy, taking shares from their current $6 or so all the way down to zero.

Avoiding such doomsday scenarios is job one for CEO Heyward Donigan, who has led the chain since 2019. But simply keeping the company limping along isn’t enough, she says. Building Rite Aid back into a growing, sustainable business means leaving the rivalry for national supremacy to CVS and Walgreens. Donigan’s turnaround plan is focused on expanding and increasing dominance in the markets where Rite Aid remains a strong competitor—including New York City, Los Angeles, and its hometown of Philadelphia. The CEO also wants Rite Aid to make much greater use of its 6,400 pharmacists to provide vaccinations, treatment advice, and health services. Also on the health care front, she hopes to use the company’s small pharmacy benefits business to go after midsize employers the industry’s larger players ignore.

Executing on this plan hasn’t gone quite as Donigan hoped—in part because the turnaround she envisioned, unveiled with fanfare in New York on March 16, 2020, had to take a back seat to the pandemic. Providing vaccination jabs and swabbing noses added about $500 million in revenue last year, but it also meant some aspects of Donigan’s strategy have been on the back burner.

“We were so excited to just get down to business—rebrand the company and launch our ‘better for you’ merchandise and redo the exteriors and free up our pharmacists to do all these clinical interventions,” Donigan recalls. “Then poof [the pandemic hits], all of a sudden the pharmacy volumes go through the roof, and we can’t free up our pharmacists to do other clinical interventions because they were so busy doing the COVID testing and giving the COVID shots,” she tells Fortune in a recent interview via Zoom.

Despite the myriad challenges, Rite Aid is showing signs of life. A few days after that April Deutsche Bank note, the company announced better than expected fourth-quarter results. Donigan has also pushed Rite Aid’s debt payments due out from 2022 to 2025, taking the prospect of an imminent bankruptcy off the table. She predicts that if her plan works, the company will return to profitability—or at least stop the bleeding—within three years.

Donigan has a message for the Deutsche Bank analyst who penned that doomsday note and anyone else who doubts the company’s comeback plan: “We’ve been the underdog, I love being the underdog.”

Missing the boat on the health care transformation

Rite Aid, which began life in 1962 as Thrift D Discount Center in Scranton, wasn’t always an also-ran. In 1987, it was briefly the nation’s largest drugstore chain by store count and remained a viable contender in a three-way arms race with CVS and Walgreens for the next two-plus decades. During that time, the story of the industry was one of scale and consolidation, with all the big players hungrily gobbling up small chains and independent pharmacies. In 2006, Rite Aid made what now looks like a critical overstep in its bid for growth, spending $3 billion to acquire the Eckerd and Brooks chains. The deal, which forced the company to take on substantial debt, might have been a less consequential mistake, had the industry not almost immediately begun a dramatic shift.

Until the mid-aughts, the drugstore business had been largely that: companies competed as retailers, aiming to sell the most lotion, candy bars, prescription and OTC drugs to the most people. But in 2006, CVS changed the paradigm with the $21 billion purchase of pharmacy benefit manager Caremark. Pharmacy benefit managers—or PBMs—function as a type of go-between, negotiating how patients pay for drugs, what insurers owe drugmakers, and how much pharmacies are reimbursed. Owning Caremark, the biggest PBM in the U.S., automatically made CVS a major health player, and spurred millions of Americans to get their scripts filled at its stores.

Since then, both CVS and Walgreens have set their sights on moving deeper into health care. They invested billions in branded health clinics; CVS now operates 1,100 MinuteClinics, while Walgreens says it will get to 1,000 VillageMD locations by 2027. And in 2018, CVS, which had rebranded as CVS Health four years earlier, merged with insurance giant Aetna to become one of the most powerful health care companies in the U.S. “When you look at that pivot, Walgreens and CVS have focused much more on turning their businesses and stores into health oases,” says Neil Saunders, managing director at research firm GlobalData.

Rite Aid has also made some inroads in health care, albeit more modest ones, including buying its own PBM, now called Elixir, for $2 billion in 2015 and making a short-lived effort to run its own line of clinics. (That business, called RediClinic, lost money and was shuttered at the start of the pandemic.) But going all in on the space—or making big investments of any kind—was off the table, owing in large part to Rite Aid’s unwieldy debt, which peaked in 2008 at $7 billion. The company suffered numerous cash crunches, and in the early 2010s was repeatedly threatened with delisting from the NYSE as its stock slipped under $1.

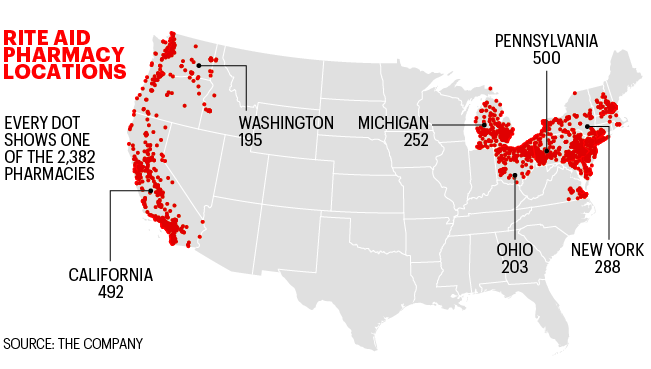

An M&A escape hatch looked like the most likely exit from the mess the company had created, and in 2015, Walgreens made its move, with a $9.4 billion acquisition offer. The deal was ultimately thwarted by antitrust regulators, but Walgreens was permitted to buy 2,000 Rite Aid locations. That gave Rite Aid a much needed $4.8 billion cash injection but reduced its store count by 40%, and blew a big gaping hole into its store map, stripping Rite Aid of its status as a national chain. A decade ago, Rite Aid was in 38 states; today that number is just 17, with a concentration in California, New York, and Pennsylvania, and complete absence in big states like Texas, Illinois, and Florida.

When another takeover attempt was blocked by Rite Aid investors in 2018—this one from the then privately held grocer Albertsons—the company was left with just one option for survival: fix its core business and go it alone.

Where does Rite Aid go from here?

Donigan’s background provides a hint at the company’s current priorities. She came to Rite Aid in 2019 without any significant retail experience, a somewhat unusual state of affairs for a CEO lately overseeing around 2,400 stores. But she knew how to navigate debt; notably, she’d served on the board of specialty hospital operator Kindred Healthcare, where she helped oversee a successful refinancing. And she had spent 25 years in and around health care, most recently as the chief executive of Sapphire Digital, a website that enables consumers to compare and choose health care plans.

Her vision for Rite Aid’s future includes becoming more involved in customers’ health—though in a more modest way than CVS and Walgreens are pursuing. While the biggest chains are opening stand-alone clinics and employing physician assistants in a bid to become primary care providers, Donigan wants to double down on the white coats she already employs: pharmacists. Pharmacy services account for 74% of Rite Aid’s revenues (versus just 33% at CVS), and Donigan wants to grow that piece of the pie and broaden health services, calling on its pharmacists to do more clinical consultations, coming out from behind the counter to, say, advise a customer on how to treat a skin condition.

To Donigan, the fact that her competitors are focused on clinic-based care rather than the pharmacy opens up an opportunity. “We are the only company in America that is a full-service pharmacy that is focused on being a full-service pharmacy and that has the assets to be a full-service pharmacy,” she says.

The pandemic led regulators to expand the types of services pharmacists may provide, including administering vaccines to kids as young as three. Donigan hopes to capitalize on the new rules and says she wants Rite Aid pharmacists to move to spending 80% of their time interacting with customers. (It’s currently closer to 20%, she says.) Getting there won’t be easy, she allows, and will likely require some technology investments to free pharmacists up from the many admin tasks that keep them hidden away in the back, not to mention making a big shift in how they and customers see their role.

Some analysts see potential in this strategy, noting that consumers tend to stick to existing habits—like going to the drugstore rather than a health clinic—and may already have a long relationship with their pharmacist. Having a well-established connection “drives a better customer experience and increases stickiness,” says Fitch Ratings senior director David Silverman.

Another prong of Donigan’s health care–centric plan is Rite Aid’s PBM, Elixir. Compared with its rivals, Elixir is tiny: Caremark, Express Scripts, and OptumRx together control 80% of the PBM market, leaving Elixir and dozens of others scrapping over the remaining 20%. But the PBM has carved its own niche by focusing on midsize employers with less than 1,000 staff, a market that bigger players find too small to bother with. And Elixir is not just a PBM; its other services include a mail-based pharmacy, an insurance offering for seniors, and a discount program for fertility drugs. Down the line, Donigan hints at leveraging whatever growth she can wring out of these programs to pay down more of Rite Aid’s debt, either via partnerships or even a possible sale. “Someone’s going to be interested in investing in one of these businesses,” she says.

And though Rite Aid, like all major pharmacy players, is moving away from retail—a low margin business where companies like Target and Walmart are gobbling up market share thanks to more appealing stores and better prices, according to GlobalData’s Saunders—she does see the advantages of growing into new markets. To that end, she has her eyes out for smaller, independent pharmacies struggling to operate in an industry where economies of scale matter. One such example: Bartell, a Seattle chain of 67 stores that Rite Aid snapped up 2020. (Rite Aid, like CVS and Walgreens, is closing dozens of stores in its top markets when locations have become too rundown or too saturated.)

Not everyone on Wall Street is quite as skeptical of the company’s turnaround plans as Deutsche Bank, but even those who think Donigan can put Rite Aid back on track expect the process to, as J.P. Morgan managing director Lisa Gill put it in a recent report, “take time and likely be bumpy.” Donigan is unfazed. “It’s very motivating for us to show the world that we can do this and that we are doing this.”