Six years ago, Liz Babb and her husband, Angelo Aloisio, retired financial services executives and new empty nesters, sold their place in San Francisco and moved to the woods. They bought a 1970s house on a steep slope in Portola Valley, an enclave of forested canyons minutes from Silicon Valley’s center that boasts a bohemian history, a reputation for moneyed discretion, and jaw-dropping views. It was an iconic—if, by local standards, modest—northern California dream home: wood construction, picture windows, multiple decks, and, everywhere, trees.

Lush vegetation blanketed the property: oaks, redwoods, and all manner of shrubs and bushes. They enveloped the house, but not only that. Soaring through the center of the structure—rising from the dirt, through the first-level floor, up three stories, and out the roof—stood a massive oak, its trunk encased by interior glass and its branches and leaves canopied over the house. “We were ready for our rural adventure,” said Babb, an avid hiker. When she first saw the shelter-magazine-worthy aerie, she recalled, “I fell in love with it.”

In August 2020, love turned to fear. A lightning storm struck hills stretching between Portola Valley and the Pacific Ocean—hills, that, like much of California and the West, are parched from years of drought. The bolts set the hills aflame. By the time five weeks later that firefighters extinguished what had come to be called the CZU Lightning Complex fires, the inferno had scorched some 86,500 acres and destroyed about 1,500 buildings. The blaze came within about eight miles of Portola Valley. The smoke plume turned the skies above the town a putrid, pallid orange. More permanently, the fire altered Babb’s view of her world. The ecology “has changed,” she said. “We’re a tinderbox here.”

Last November, fear turned to fatalism. Babb got a letter from Safeco, the company that had insured her homes for more than 15 years. Safeco informed her it was going to drop her homeowners policy in January; it had concluded her house in the trees was too severe a fire risk. For the next several weeks, Babb searched for another insurer, but other carriers, too, saw her house as a firetrap. Finally, days before their policy was to expire, she signed up for the California FAIR Plan, a last-resort fire-insurance pool that California established following urban riots in Los Angeles in the 1960s for people unable to get coverage through the regular market. Still, she will pay $8,000 annually for her full complement of homeowners insurance, about $7,000 of it for fire. That’s four times what she paid a year ago.

Babb and Aloisio, like many of their neighbors, can afford the expense. But even their rarefied ZIP code offers a window into the economic fallout from wildfires—recurring disasters that are intensifying in part owing to climate change. Here as elsewhere in California and across the American West, a surge of decisions by insurers not to renew the fire policies of property owners in combustible locations is spurring political fights and stoking fears of sinking property values. More consequentially, it is exacerbating societal inequities in ways that foreshadow dilemmas that will become more common in a warming world.

Over the past two years, insurance companies worried about wildfire risk have ditched perhaps as many as 500 of Portola Valley’s approximately 1,800 houses, estimates Jeff Aalfs, a town council member. And that’s just the start, figures Jeremy Dennis, the town manager. “Over time, I would expect the majority of people to have an issue,” Dennis told me one recent morning, as we sat at a picnic table outside Portola Valley’s handsome, wood-sided, LEED Platinum–certified town hall. Towering over us was a circle of 100-foot-tall redwoods, known as a fairy ring. Nearby, a group of locals prepared for an outdoor chair-yoga class.

A wider degree of uninsurability would make Portola Valley even more exclusive. Because mortgage lenders typically require fire insurance, the only people with the wherewithal to live in what insurers deemed a fire-prone no-go zone would be those affluent enough to pay cash for their houses and to shoulder the risk of watching that investment flame out. What dislocates Portola Valley, moreover, is likely to threaten the very viability of less affluent California communities, where the average homeowner has much less in the bank. “The state is suddenly going to have millions more houses that can’t get insurance,” said Dennis, who himself lost his fire coverage for a cabin he owns in Arnold, a mountainous town between San Francisco and Lake Tahoe. “We’re just one city among hundreds that has this issue.”

This year will be remembered as the one when climate-induced disasters—floods in China and Germany, hurricanes in New York and Louisiana, wildfires in Greece and across the American West—reset the global outlook. Millions of people who either didn’t grasp the intensifying risk of climate-induced catastrophe or ignored it are confronting a new reality—one not just psychological but also, and more immediately, economic. Policymakers in Washington and other global capitals continue to dither about whether to impose a serious price on carbon emissions—a seemingly endless debate that in November will top the agenda of yet another United Nations climate conference, in Glasgow. But industries from automakers to oil producers to consumer products manufacturers to insurance firms are concluding that they no longer have the luxury to wait. Indeed, in responding to climate change, the capitalists are leading the politicians.

No sector feels more keenly than insurance the imperative to integrate climate risk into its economics. As vast tracts of the planet flood and burn, it has billions of dollars at stake. Consulting firm Milliman, relying on data from the National Association of Insurance Commissioners, reports that from 2016 to 2019, insurers forked over $37 billion for wildfire losses in California, a sum that exceeded the $32 billion in premiums they had taken in. Payouts for 2020 and 2021, years of even bigger wildfires, could well end up higher.

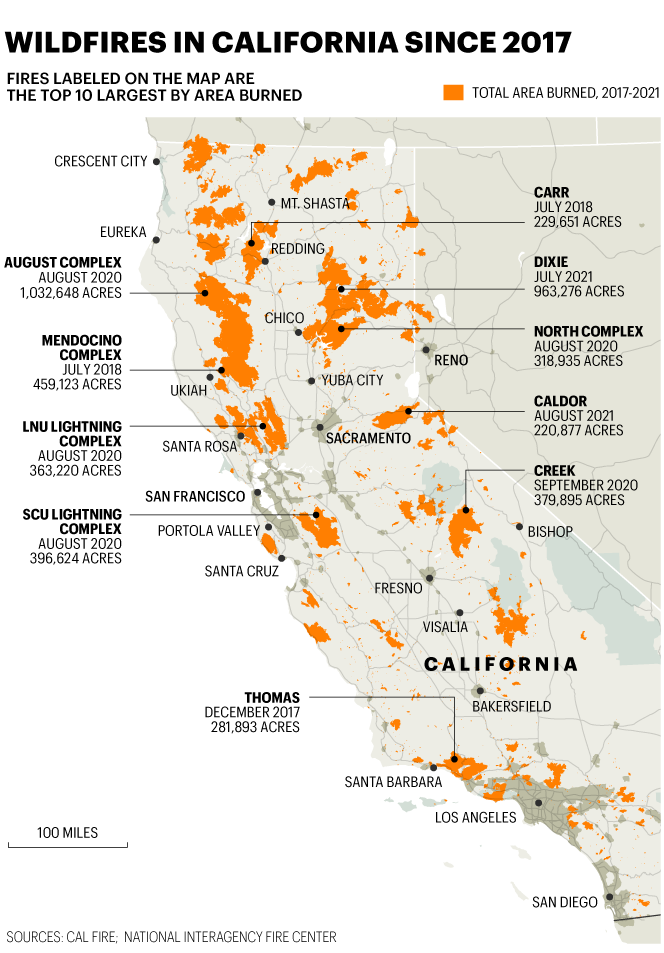

While fires have plagued much of the West in recent years, California is the unquestioned epicenter of the fire-insurance crisis. The state is currently in the fifth year of a stretch of historically destructive conflagrations: The eight biggest wildfires in California history, in terms of acreage burned, have taken place since 2017, according to Cal Fire, the state’s wildfire-fighting agency. As development has pushed more people into former wilderness, and as severe drought and higher winds—both linked to global warming—have extended wildfire’s reach, the stakes in lives and property have soared. California wildfires have consumed at least 11,000 homes and other structures in the past five years—impacting homeowners from hardscrabble towns in the Sierra Nevada mountains to exurbs ringing Los Angeles, from vineyards in the Napa and Sonoma valleys to ski resorts overlooking Lake Tahoe, from beach towns to hilly enclaves such as Portola Valley.

Facing this onslaught, the insurance industry is starting to change what it sells and to whom. In the process, it is emerging as perhaps the world’s most aggressive force pushing society to confront the costs of a changing climate. Insurers are racing to modernize the models they use to assess wildfire danger—models that, in the era before runaway climate change, had lagged behind those they use to predict hurricanes and earthquakes. They are pressing homeowners to “harden” their homes against fire—to replace wood roofs with ones made of fire-resistant materials, to slash vegetation bordering exterior walls, even to add expensive yard-sprinkler systems that can be turned on, like a Tesla, from afar by phone. When all else fails, insurers are jettisoning clients like Babb and Aloisio—people whose homes, the companies have concluded, now are too likely to go up in smoke. Businesses, too, are facing insurance pullbacks.

The attempts by insurers to recalibrate for a warmer world are spurring a furious backlash from property owners. In California, both the push and the pushback are playing out on two fronts. One comprises the communities whose homeowners and businesspeople are losing their policies. In 2019, the most recent year for which data is available, insurers declined to renew the homeowners policies of 235,274 Californians, according to the California Department of Insurance. Though that’s only about 3% of the 8.6 million Californians who had such policies, it represented a 31% jump in nonrenewals from 2018, with most of the increase coming from areas of high wildfire threat. The fire-insurance fallout, moreover, is compounding a statewide housing shortage; in many pockets of the state the difficulty of obtaining coverage is constraining new construction, a further climate-induced economic squeeze.

The other front is Sacramento, where a battle is unfolding with important implications for other regions struggling to adapt to climate-related disasters. California long has typified two quintessentially American tensions: the one between populism and profit, and the one between idolizing nature and building on it. These long-simmering conflicts are boiling over in a fight over how much regulators will let the insurance industry jack up the rates it charges some property owners. Insurance carriers argue that the state’s regulatory regime doesn’t reflect economic reality in an era of rising wildfire risk. In the decade prior to 2018, the average California homeowner’s total yearly premium—including fire and other protections—increased just 16%, compared to 42% nationwide, according to Property Insurance Report, a trade publication. California’s average homeowner’s premium in 2018, $1,073, placed California 40th among the states in premium as a percentage of household income. Those numbers suggest California consumers have been shielded from global warming’s economic blows—that aligning price with risk could mean jarring price increases for many.

What’s especially telling about California’s conundrum is that the Golden State long has been singularly supportive of charging fees to protect the planet. State legislators years ago imposed an electric-vehicle mandate and a cap-and-trade program for greenhouse gas emissions that amounts to a tax on carbon—both examples that other states and nations have followed. The intensity of today’s fight over wildfire-insurance rates suggests that dinging corporate polluters is, politically speaking, an easier strategy than docking millions of voters.

California’s long tradition of consumer activism makes it particularly difficult for insurers to raise rates. For one thing, state law requires insurers to get approval for any increase from the state insurance commissioner—who, unlike the chief insurance regulator in most other states, is elected rather than appointed, rendering the commissioner particularly attuned to voters’ dissatisfactions. For another, California law allows anyone to file a legal challenge if an insurer requests a price increase that averages 7% or more.

But the biggest barrier is a stipulation that the commissioner may approve only rate increases that fall within a price band determined by averaging an insurer’s prior 20 years of fire-related losses. In theory, the backward-averaging method prevents anomalously light or heavy fire seasons from whipsawing premiums. But it assumes that future fire trends will look pretty much like past ones—an assumption that, as the planet warms, looks increasingly incorrect. In retrospect, the methodology has perpetuated a false sense that the economics of fire insurance in California are sound, said Nancy Watkins, a principal and consulting actuary at Milliman. “Looking behind you says everything is flat,” she said. “What’s ahead of us is the new normal of climate change, where the risk is a lot higher.”

How much higher became clear after the one-two punch of the 2017 and 2018 fire seasons. Starting in earnest in early 2019, insurers shed clumps of customers whose properties they deemed unreasonable risks. The nonrenewals have been most pronounced in the region stretching from south of Lake Tahoe to the Oregon border, where from 2018 to 2019 they more than doubled, to 25,508, according to insurance-department data. But the numbers have risen across the state. The nonrenewals have enraged homeowners and sparked an outcry from the current insurance commissioner, Ricardo Lara. He has issued a series of one-year moratoriums against nonrenewals for residents of a growing string of zip codes that California Gov. Gavin Newsom has declared wildfire disaster areas.

The upshot is evident in the crunch now facing the state’s last-resort fire-insurance pool, the California FAIR Plan. Despite its downsides—including its priciness and the fact that its coverage is limited to $3 million, which is less than the value of not a few California homes—the FAIR Plan has grown rapidly both in the number of Californians forced to use it and in the portion of them who live in high-wildfire-risk areas. In 2019, the number of policies in the FAIR Plan shot up 36%, to 190,196 people. More recent figures aren’t yet available, but FAIR Plan documents suggest the burden continues to rise. In 2014, the portion of the pool’s insured properties that sit in “wildfire-exposed” areas was 25%. By 2020, it was 65%. In August the plan, citing a huge increase in wildfire exposure, filed a request with the insurance department for an average 48.8% increase in its already-high premiums, arguing that the system’s “overall rate inadequacy has grown.”

The insurance lobby has launched short- and long-term campaigns in Sacramento for rates that better reflect climate-related disasters. The immediate bid is for permission to charge more. A large number of carriers have recently asked Lara to grant them rate hikes just below the 7% threshold that permits legal challenges. These asks have come to be known by the just-under-the-wire increase they request: “6.9s.” Other insurers are, like the FAIR Plan, risking bolder action, requesting double-digit average rate hikes.

More lastingly, insurers are pushing to replace California’s 20-year-backward-averaging methodology. They want the state to let them use models to substantiate their requests for fire-insurance price hikes, much as other states do, and much as California already does for disasters such as earthquakes. They contend that the freedom to use models would let them more accurately—and, of course, more profitably—assess wildfire risk and apportion premiums. Rather than toss Californians off their books, they say, they’d be able to insure them—at higher prices than many of those consumers have been paying, but at lower rates than the FAIR Plan would impose. Insurers say modeling also would trim premiums for some homeowners who are penalized by the backward-averaging rules.

But in California, a state whose tech giants have spawned algorithms humanity loves to hate, the notion of computer models setting prices raises hackles. Politicians and consumer groups deride the idea as just the latest corporate feint to gouge the public. Lara in 2020 lambasted a bill that sought to allow insurers to use them, saying it would harm consumers by deploying “secret, confidential catastrophe models cloaked from public transparency.” Nevertheless, this July a state task force recommended hearings on the prospect of using modeling, with an emphasis on public openness.

Transparency, at least in the physical sense, is a rarity in Portola Valley. Redwoods and oaks—along with notoriously flammable invasive species such as eucalyptus and acacia—grow prolifically, prized in large part for their provision of privacy. The town was born in 1964 primarily to protect the landscape; locals incorporated to block the proposed development of a vast tract. (They won; it’s now an open-space preserve.) In 1966, a young band called the Grateful Dead played the annual Christmas dance of a local school.

As nearby Silicon Valley took shape and prospered, Portola Valley changed too. It began to morph into a high-priced bedroom community. Today it brims with technology titans and tree-huggers; often they’re the same people. Porsches and Teslas share its sylvan, serpentine roads with high-end racing bicycles. The town has a population of about 4,600 and a median household income of $250,000; the median value of its homes, many of which enjoy stunning views of plunging canyons or of San Francisco Bay, is $2 million.

Portola Valley’s angst about wildfire insurance dates at least to 2007. That year it, like communities up and down California’s hillsides, was served with a new Cal Fire map flagging about 10% of the town’s acreage as a “very-high-fire-hazard-severity zone.” The map incensed many locals. They worried the documents would saddle them with higher insurance rates. Because the state requires that the designation be disclosed to prospective homebuyers, they fretted it would jeopardize their property values too.

The opposite fear dogged Denise Enea, then the fire marshal of the Woodside Fire Protection District, which includes Portola Valley: that the maps underestimated the town’s areas of greatest combustibility, leaving unwitting residents in harm’s way. She recalls contentious discussions with town officials, after which they agreed to hire a private consultant to assess local vegetation. When the consultant, Ray Moritz, began putting together his own map and report, town leaders were floored to discover he had identified more of the town than Cal Fire had as of very high concern. In a vitriolic 2008 town council meeting, speaker after speaker fumed that the Moritz map would hit their homes’ insurability and values. One council member, according to the official minutes, declared the body “should do whatever it could to get the State to adopt its original map.”

That opposition infuriated Enea, who saw it as valuing money over life. “I was blown away,” she told me. “My job was to protect them and they didn’t want any part of it.”

Portola Valley did adopt a slate of tougher state building rules designed to improve the fire resistance of structures. And it inserted in its overall planning document references to Moritz’s map and report. But the town council declined to formally adopt either the Cal Fire map or the Moritz one. Dennis agreed that town residents and leaders back then were leery of anything they thought would raise insurance rates and lower property values. That’s a reticence he ventures would not prevail today. “There would be many more voices in that conversation, because of climate change,” he told me. “We’ve got new information. New times.”

That new information hit the town in the form of California’s disastrous 2017 and 2018 fire seasons. It has prompted Portola Valley to start reckoning with some hard choices. In 2019, just as insurers began gunning to update state policy governing fire-insurance pricing, the town council created a committee to recommend ways to reduce wildfire danger. The 2020 CZU fire further fanned local concern, said John Richards, a soft-spoken architect who has served on the town council since 2009. “That woke people up. There was a massive plume over there,” he told me, gesturing westward as we sat at the town-hall picnic table. One wrenching realization this arboreal retreat is confronting, he said, is that it should no longer allow the unchecked growth of trees. “The idea that we could let nature take its course,” he said, “is no longer an option.”

Work crews in the town are scrambling to clear away brush, but the task is “monumental,” Don Bullard, the current fire marshal, told me as we drove around town one recent morning in his official SUV. “Those are all assets at risk,” he said, pointing at a line of high-end houses on a ridge. “A torch,” he added a bit later, pointing to a dying, and thus particularly flammable, redwood tree.

The town council has, on the suggestion of the fire-safety committee, banned the planting of a handful of highly combustible trees: acacia, cypress, eucalyptus, juniper, and pine, which officials dub the “flammable five.” Another of the committee’s suggestions is under consideration: prohibiting wood-shake roofs and wood siding, and decreeing that wood decks and wood fences, basically matches to flames, may not be connected to houses, so as not to ignite them. Some town officials expect a fight but predict passage.

More battles are brewing. A group of worried residents recently hired Moritz to produce an updated report. He believes the town in 2008 “buried” his findings, and he said his new research finds that the fire hazard in Portola Valley has since only worsened: Not only has wildfire activity in the vicinity intensified, but vegetation—what firefighters call, simply, “fuel”—has thickened on the slopes of the town’s many so-called box canyons. Those V-shaped ravines form the backyards of many Portola Valley houses; in the event of fire, they act as chimneys, speeding the uphill spread of flames. Moritz said the situation brings to mind an aphorism that’s a firefighter favorite: “If you stick your head in the sand, you’re going to get your ass burned.”

Heads are poking up over new fears about uninsurability. Another round of updated Cal Fire fire-risk maps is due out starting later this year, and those maps are expected to label as very-high-fire-hazard-severity zones a much greater portion of California. Because of the money riding on the maps, discussion around them has been “lively,” noted Daniel Berlant, chief of Cal Fire’s wildfire planning and engineering division. But he said the maps, in the works for about five years, will be based on science—specifically a new Cal Fire model designed to better reflect increased fire danger, largely from climate-linked increases in wind.

The specter of those maps prompted Dennis, Richards, and another Portola Valley council member to write state officials in August declaring themselves “very concerned” the updated Cal Fire maps will put the town in a vice grip yet again. One of their worries is that the maps will make it harder to comply with another Sacramento requirement: that California localities add a specified number of new housing units—in Portola Valley’s case, 253—to help ease the state’s housing crunch. “If insurance nonrenewals continue,” they wrote, “it may prove impossible for newly constructed homes to be insured, let alone existing properties.”

Babb, the Portola Valley homeowner now relegated to the FAIR Plan pool, knows that threat firsthand. When I drove up to her house one recent morning, she pointed to the tree jutting out of her roof and deadpanned a greeting: “There’s the candlewick.”

After she and Aloisio gave me a tour of the place, we took seats on soft outdoor furniture on a second-story deck—made, naturally, of wood. As blue jays chirped, Babb recounted how summers seem to have gotten hotter in the six years she and Aloisio have lived in the house, how recent wildfires north of San Francisco have destroyed the homes of not one but two families who are their friends, and what the heavens over Portola Valley looked like as the summer 2020 CZU fire approached. “The sky was orange,” she recalled. It evoked “a nuclear winter.”

Babb and Aloisio decided to flee that fire, driving to a hotel near relatives in Los Angeles, where they stayed until the smoke subsided. Babb needed no education about fire’s power to destroy: In 2008, a blaze ignited by a short circuit in old wiring destroyed the 106-year-old wood-shingled house in San Francisco’s storied Presidio Heights neighborhood in which she then lived; luckily, no one was home. Today, Aloisio and Babb blame themselves for having bought a wooden house encasing a massive tree on a wooded hillside in the vicinity of worsening wildfires. “I think we were ignorant,” Aloisio said. (A spokesman for Liberty Mutual Insurance, which owns Safeco, said the company has “taken the difficult but necessary step to reduce our overall exposure to wildfires” but continues to sell California policies that it thinks don’t “present an unacceptable wildfire exposure.”)

After a while, Babb and I strolled up her street, a winding, one-lane affair that, she noted, would be hellish to drive down if everyone in the neighborhood were fleeing oncoming flames. We passed house after wooden house perched on steep terrain and fringed with vegetation. At the crest of the hill, we came upon a ranch gate. Beyond it lay one of the many stunning trails that Babb loves to hike. But the trailhead, she noted, has a second purpose. In the event of wildfire, the gate is to be flung wide open and the path used as an evacuation route.

CORRECTION: Insurers paid out $37 billion for wildfire losses in California from 2016 to 2019, according to a Milliman report relying on data from the National Association of Insurance Commissioners. An earlier version of this story incorrectly said that $37 billion was the total for wildfire losses nationwide.

A version of this article appears in the October/November 2021 issue of Fortune.

More must-read business news and analysis from Fortune:

- What a modern energy crisis looks like and why no country is safe

- Frustrated carmakers upend industry after chip shortage shatters their faith in suppliers

- Portugal leads the world in COVID-19 vaccinations

- A WHO-approved Novavax vaccine could upstage mRNA jabs—if it can solve its manufacturing delays

- Bitcoin has another major pollution problem brewing

Subscribe to Fortune Daily to get essential business stories straight to your inbox each morning.