A grant from the NIHCM Foundation helped fund reporting for this story.

Even against the backdrop of the past 18 months, and epic levels of American suffering, John and Jodi Philipp have had a rough go.

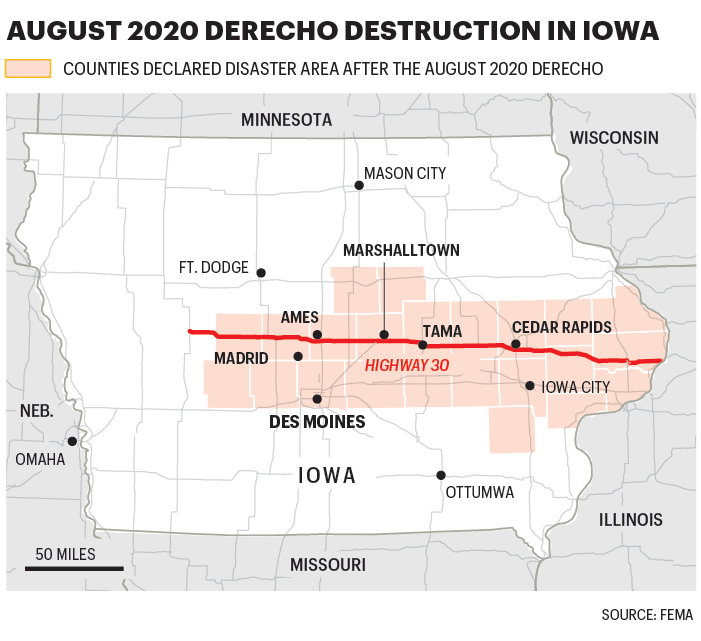

They both struggle with serious health issues—she a brain tumor, and he Stage 4 cancer that was diagnosed in November 2019 after experiencing a couple of strokes. As the pandemic began in early 2020, their rural Iowa businesses—2 Jo’s Farm and Periwinkle Place Manor—took a hit, since both depend on visitors and gathering for events. Then, on Aug. 10, as Jodi was driving John home from a cancer treatment at the University of Iowa to their farm in Van Horne, a town of 900-some people, they were caught in a freakishly intense windstorm—a derecho, or straight-line wind event—that wreaked havoc that day on a 770-mile swath across the Midwest and would go down in the books as the most expensive thunderstorm in history.

They pulled over, but as the torrential rain and hurricane-force wind blasts—gusts peaked at 140 mph—rattled their car, “we felt like we were going to die,” said Jodi, who was receiving a stream of texts and calls from her son at the farm until his signal went dead. His last message to her was that they should “be prepared.”

The drive, normally 50 minutes, took hours. As they passed silos that had blown onto the highway, and barns and crops that had toppled to the ground, they took in what seemed like a full preview of the storm’s destruction.

Even so, what Jodi found at the farm, a 13-acre property off Highway 30 (the old Lincoln Highway) in Iowa’s rural Benton County, left her dazed.

The Philipps’ farm is not a traditional Iowa farm. The couple, who for decades have played Santa and Mrs. Claus at venues and holiday parties around the Midwest, raise reindeer and have a camel named Kringle. The property, which hosted events, also had a mini Western town and a riding arena. Their farm buildings were demolished. Most of the trees were down, and the house and garage had too much damage to quickly process. The place was uninhabitable, she says, and most of their personal belongings damaged beyond repair. “It’s still unbelievable,” she told me when I first spoke with her. “When we go there, we just walk around and stare and wonder, what are we going to do?”

That conversation was in early January, when Jodi was making trips to Van Horne two times a day to feed and water the animals. She and John were living 30 minutes away, at their other business, Periwinkle Place Manor, a former funeral home that they bought and restored several years ago before converting it into a bed-and-breakfast (or dead-and-breakfast, as Jodi winkingly markets it) that hosts murder-mystery theater.

The manor, a Victorian mansion that dates to the late 1800s, is in Chelsea, Iowa, a low-lying, flood-prone town of 300 residents on the other side of the Lincoln Highway (so flood-prone that the city council voted to move Chelsea to higher ground decades ago; it hasn’t). Chelsea got crushed by the derecho, too—its town library was a casualty—but the manor sustained only minor damage (though it did lose power for 2.5 months), and that’s where the couple were staying with their intellectually disabled 26-year-old daughter and dog when both John, 72, and Jodi, 62, came down with COVID in late November. Jodi recovered quickly enough to take on a few Mrs. Claus jobs in December, but John, who had blood clots in his lungs and pneumonia, was in the hospital for a month. For the third time in a year, Jodi thought John was going to die. He came home on Christmas Eve day.

Yet, for the almost boundless trauma the Philipps faced in 2020, Jodi would argue that this year hasn’t gotten better. In the aftermath of these events, and the effort to recover, things have only gotten worse.

That’s largely because of a battle with her property insurer, which by Jodi’s telling has been a frustrating, confusing, lonely, and increasingly desperate monthslong slog. To date, their insurer has paid out $212,525.43 for derecho-related claims to the property—almost all of it for the demolished riding arena—a small fraction of the total cost of the damages and of the sum that Jodi and experts she has hired argue she and John are owed under their $673,000 policy. Her home, on which the insurer has paid out just $29,663.13, remains in tatters and exposed to the elements. The family remains living at Periwinkle Place Manor, in an austere limbo.

“We have good insurance, or we thought we did, for many, many years,” said Jodi. “It’s been a rough year, and for the insurance company to completely turn their back on you after you’ve paid for insurance for 20 some years and never had a claim—in my opinion that should be a crime.”

I had initially gotten in touch with Jodi when I came across a GoFundMe page that a family friend had made on their behalf last year. At the time, I was reporting a story about how my home state was coping with its dual disasters—the derecho and the pandemic. With John just out of the hospital, I had assumed the couple’s battle with COVID would dominate our discussion, but even as John struggled with the lingering effects of the virus, it was clear the source of greatest stress for Jodi was the utter helplessness she felt about the situation around her farm.

When we spoke again in March, there had been little progress. It was the same story in June, though Jodi, at a breaking point and hoping to call attention to her plight (a car dealership in a neighboring town had successfully deployed the strategy), had custom-ordered for $360 bright orange banners, which she then tacked up to their fence that runs along the highway. The banners, which are no longer displayed, trumpeted out over three 10-foot-long signs the distress she felt due to the treatment by her insurer Benton Mutual and NCP Group, the third-party administrator working on the claim.

In response to the Philipps’ allegations, Benton Mutual said it could not comment on individual claims, as did NCP Group, which as a third-party claims administrator, and not the Philipps’ insurer, noted that it did not have authority to do so.

The long road to recovery

The Philipps are among thousands of Iowans still struggling to resolve claims related to the storm, an administrative task that is often just the first step for homeowners trying to get back on track. They’re also up against the clock: In Iowa, a state that promotes itself as the nation’s new insurance capital, most policyholders have just one year before the statute of limitations runs out for filing suit over claims—the only recourse (albeit an expensive one), some argue, that consumers have in disputes with their insurers.

In a year when the recovery process in Iowa has been slowed and complicated by a global pandemic and a slew of natural disaster and pandemic-induced shortages, those pressures add to what many, including Jodi, describe as a second trauma: navigating the red-tape-ridden obstacle course to recovery.

But this story is about more than one couple’s travails, or one bad experience with an insurance company, or even the messy aftermath of a single horrible natural disaster. The derecho, along with damaging homes and blowing the roofs off buildings, exposed the fundamental problems of an entire industry. As the business model that undergirds the insurance sector faces ever more pressure from climate change and bank-breaking catastrophes, some argue that it has become increasingly stacked against homeowners and fails to provide the safety net that ordinary people believe they have paid for.

Such battles in the wake of disaster are hardly a new problem. The story of wronged policyholders is the animating force behind Delay, Deny, Defend, the 2010 book by Rutgers law professor Jay Feinman. The book argues that some property and casualty insurers, in an effort to boost their bottom lines (following a playbook developed by management consultants), have developed tactics to sap people of the will, emotional energy, and financial wherewithal it takes to collect what they’re rightfully owed by their insurers. “It’s much more difficult to get paid for a valid claim now than it was 25 years ago,” Feinman told me.

The frustration and injustice of that experience is what led Douglas Quinn, a then-financial adviser whose waterfront home was badly damaged by Hurricane Sandy, to found the American Policyholder Association, an organization aimed at stopping fraud in the sector. The power dynamic in these battles is heavily tilted in favor of the multibillion-dollar insurance industry, he said. “It’s the storm after the storm, and in my experience the storm was the easy part,” said Quinn, who added he’s seen the same patterns he experienced—from insurers using age-old intimidation tactics to trying to shortchange policyholders by swapping in artificially low material prices on their Xactimate software (which adjusters use to price claims)—play out in Iowa, not to mention every other place where there’s been a natural disaster. “We see these things all over the country,” said Quinn.

The industry, to the extent that it engages, is dismissive of such characterizations, which it sees as self-serving messaging of plaintiffs’ attorneys, and often the result of consumers not fully understanding their policies before disaster strikes. In response to my outreach, companies emphasized their commitment to handling claims with care and honoring the coverage they set out in their policies. The Information Insurance Institute (III) also encourages people to know exactly what’s in those policies by asking questions and shopping carefully; it cautions people against choosing the cheapest policies without scrutinizing the coverage provided. “Don’t buy a junk car and then expect a Cadillac of a product when you have a claim,” III Media Relations director Scott Holeman told me.

Dave V. String, a vice president at NCP Group, the administrator that processed the Philipps’ claim, commented generally on disputes: “We as adjusters are involved in handling claims in very tenuous, stressful and scary times for insureds, many of whom have never filed a claim before. NCP Group wants every insured we assist to be paid every dollar their policy allows. Sometimes this takes further investigations; sometimes it takes additional inspections; and sometimes it takes additional discussions. These add to insureds’ frustrations, but we do everything we can to get it right as quickly as possible…One of the largest obstacles to overcome with insureds is when they expect coverage for something their policy does not provide. NCP Group’s clients require that we follow the language of the policy in any recommendations we make to our clients. We will go out of our way to make sure nothing is missed, but we cannot change the terms of an insured’s contract.”

Regardless, climate change and the increasing frequency of extreme weather events—not to mention the mounting costs associated with them, and the underpreparedness of all involved for this new reality—suggest these battles between insurers and policyholders will only become more frequent and bruising, with a growing number of people likely to fall through their insurance safety net.

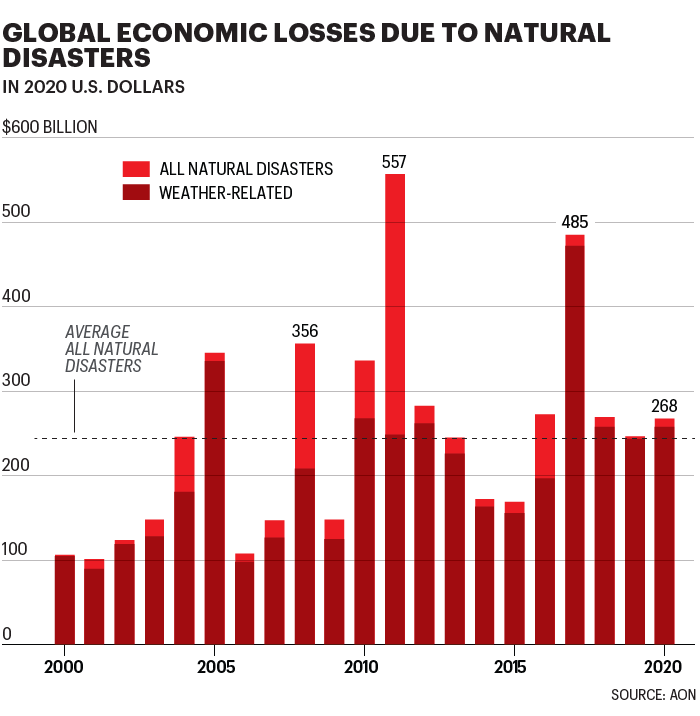

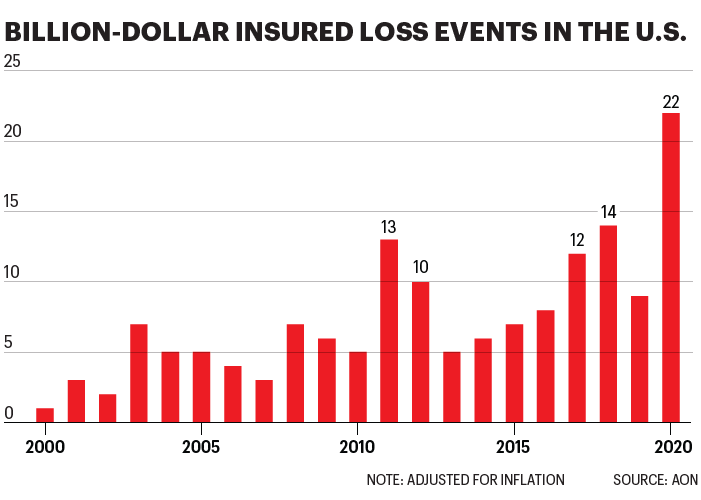

Evidence of those forces, of course, is already in plain view. The U.S. faced a record number of devastating and costly weather and climate disasters during 2020—a total of 22 events in which losses exceeded $1 billion—according to data from the National Oceanic and Atmospheric Administration, or NOAA. The government agency noted last year’s count “shattered the previous annual record,” which involved 16 such events. Insured losses due to those events in 2020 stand at $73 billion, 82% above the (inflation-adjusted) average figure for the past 20 years.

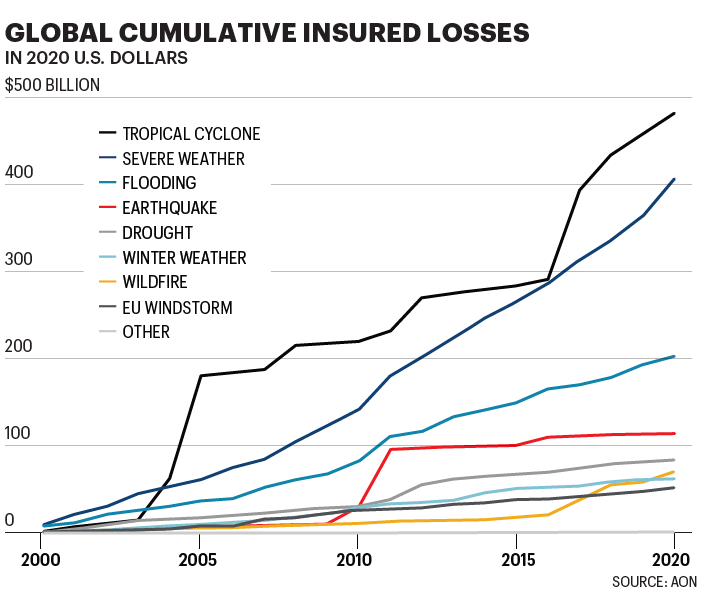

“We’ve witnessed insured losses caused by natural disasters increasing at an alarming rate, growing nearly 700% since the 1980s,” Holeman wrote in an email to Fortune, adding that last year brought record-breaking Atlantic hurricane and Western wildfire seasons (which included five of California’s six largest ever wildfires). “Still, the insurance industry has demonstrated leadership through disruption, paying claims for the insured.”

He noted that while insurers have built climate risk into their business models for years, “2020 illustrated how the disruption continuum is evolving.”

And 2021 is proving to be disruptive too. As of July 9, NOAA had tallied eight $1 billion weather and climate disasters in the U.S. this year, which, beyond economic losses, resulted in the deaths of at least 331 people. They include events that were previously simply unfathomable, like Texas’s crippling 10-day winter freeze and the Pacific Northwest’s record-shattering heat wave.

The derecho, too, outdid the imagination, racking up in a matter of hours last August an estimated $11.5 billion in damage across the Midwest. The devastation was particularly severe in eastern Iowa, where the intensity of the wind led to destruction well beyond what weather forecasters or actuaries ever thought possible. Just about every home in Cedar Rapids—a metropolitan area of nearly 258,000 people—sustained some sort of damage in the storm. Many people in the very hot month of August lost power for more than a week, and some for far longer. “The derecho really opened a lot of eyes in terms of the fact that thunderstorms can end up leading to hurricane levels of losses,” said Steve Bowen, head of catastrophe insight for Aon, the global professional services firm. He noted that properties in the region, whether brand new or decades old, weren’t built to withstand such wind speeds. “It was a reminder that even perils that historically haven’t necessarily been massive drivers of damage are increasingly becoming higher risk,” added Bowen. “This is an event that caught a lot of us off guard.”

Indeed, Iowa was not ready for hurricane level losses. Compared to wildfire country, and hurricane-prone coastal states, Iowans are relatively inexperienced when it comes to widespread natural disasters, and Iowa lacks the robust infrastructure and know-how that more practiced states have developed over time to deal with such events. The state has no licensing requirements for insurance adjusters, meaning just about anyone can do the job of assessing damage for insurers.

Finding help

Meanwhile, resources to support insureds with the claims process or in disputes with their insurers are few. Public adjusting, or working as an independent advocate for policyholders (rather than for insurers), does require a license, and there are a relatively small number of them providing the service in the state. (They number in the thousands in Florida.) Similarly, lawyers who specialize in disaster-related insurance losses are extremely few. On the website of United Policyholders, a nonprofit that aims “to level the playing field between insurers and insureds,” the Iowa “Find Help” resource page lists just one public adjuster, Swift Public Adjusters, and one law firm, Larew Law Office. (The listings are sponsored.)

James Larew, who served as general counsel to Iowa Gov. Chet Culver from 2007 to 2011, started his practice to support policyholders in 2011 after realizing there were many people in the state who had issues with property and casualty insurers and nowhere to turn (they often tried to meet with the governor about their problems). Born and raised in the state, Larew noted that Iowans tend to take their lumps, meaning they’re culturally unlikely to challenge their insurers over claim payments. Even when they do, the state is not hospitable to such challenges because of laws and policies that bend in favor of the industry, he and others contend. (Iowans have to pay their own legal fees, even if they do win, for example, and the state allows insurers to write into their contract a limitations period as short as one year, compared to the 10-year statute of limitations that is presumed for written contacts more broadly in the state.)

Add to that the vulnerable circumstances of people whose homes have been been stricken by disaster, and the fact that lawsuits are wearing and expensive. Insurance companies know the risk they will be sued is low, a dynamic that allows them to underpay policyholders with little fear of consequence, Larew said.

When I spoke to Doug Ommen, commissioner of the Iowa Insurance Division (IID), in late July, insurers had paid out more than $3 billion on 225,000 derecho-related claims in the state. Roughly 18,000, or 8% of those claims, remained open, a volume that Ommen said reflected the scale of losses as well as shortages of labor and materials. The IID had received 392 derecho-related complaints, most of which have been investigated and closed by the agency. Of those, 110 of the complaints were confirmed—largely over “delays in the claims process as well as damages missed during inspections of the property”—resulting in an additional $307,000 paid to policyholders in the state. After Fortune asked about the issue, the IID also issued a bulletin advising insurance carriers to accommodate requests for extensions given the circumstances, including a shortage of insurance adjusters, that have slowed the recovery process for many in the state; at least one public adjusting firm says, in most cases, insurers continue to deny extensions. Ommen said his office was investigating issues raised by the derecho, like whether allowing one-year limitations in policies made sense.

A common trauma

Homeowners insurance should be a blessing when disaster strikes. Commercialized in the 1950s as a product to protect families against life-altering, wealth-destroying events like fire and tornadoes, mortgage lenders soon made it a requirement, and today 93% of American homeowners have a policy, according to the Insurance Information Institute. While standard home insurance doesn’t cover all catastrophic events—see earthquakes and floods—it does generally cover wind damage, meaning that private insurers were on the hook for the majority of derecho-related losses suffered by homeowners in the state.

That helped the state bounce back quickly, Dennis Harper, recovery division administrator for the Iowa Department of Homeland Security and Emergency Management, told me in January. “[Private insurers] were able to get in and get checks written right away,” jump-starting the repair and recovery process for homeowners, he told me. While the pandemic and widespread power outages due to the derecho complicated the job somewhat, the path to recovery for most was relatively clear and well-funded. (By comparison, explained Harper, 60% to 70% of people affected in the state’s occasional flood events tend to be under- or uninsured against losses.)

Indeed, many Iowans had a fine experience in the aftermath of the storm. They may have had to jump through a few hoops—my parents, who live in Cedar Rapids, for example, got a new roof after their contractor successfully challenged the insurance company’s denial for one—but they feel they were treated fairly. After talking with people and officials in January, my sense was that between robust insurance protection and Iowan neighborliness (Iowans helping Iowans with chain saws), the state’s derecho-impacted communities were doing pretty well, or at least moving forward in what would necessarily be a long and arduous recovery due to the scale of damage.

But as the months have worn on, it’s become clear that that’s not the complete picture. There are lots of stories involving homeowners like Jodi, who despite considerable effort feel they are stuck in the process and poorly served by the insurance companies whose policies, at least in theory, were supposed to protect them. Some of these cases involved my friends and family; scores of others are posted, SOS-like, on Facebook pages—such as the Iowa Derecho Storm Resource Page and Iowa Insurance Claim Q&A—that were formed as a support network after the storm. Both of those groups have thousands of members who, among other things, exchange information on their dealings with State Farm, Allstate, Benton Mutual, NCP Group, and any number of other insurers. Many, at this point, are exasperated. Their experiences, as I’ve learned in talking with a number of them, are uniquely complicated, but they share common traumas: a feeling of powerlessness and a sense of betrayal by an industry that so prolifically advertises itself as a good neighbor. They feel trapped in a labyrinth of their insurer’s making.

Take Rebecca Yoder, a 52-year-old Procter & Gamble employee who lives in Cedar Rapids with her husband; she describes her experience as “an utter nightmare.” For her property claim, she’s had to deal with five different field adjusters and so many desk adjusters at Allstate that she’s “lost count.” She has the sense that none of them talk to each other or make use of the copious documentation—150 photos and a detailed list of damages—that she provided them. Throughout the process, she has felt “ignored, lied to, made to feel stupid.” Her roof is leaking and, she argues, in need of replacement, but Allstate has agreed only to patch it. (She said none of the five adjusters who visited actually got on her roof to properly inspect it.) Contractors, meanwhile, were unwilling to give her quotes unless Allstate approves a full roof replacement. She finally found a contractor who would, but he disappeared on her, as have a painter and a public adjuster she hired (ghosting is a common problem for derecho-impacted homeowners, I’ve learned). Initially, Allstate paid the couple a little over $10,000 for the claim; through dogged follow-up, Yoder, with the help of a public adjuster, has gotten the total to a little over $20,000—less than half of what her public adjuster estimates she is owed.

“The emotional toll of it has been very tough,” she wrote to me. “Getting our hopes up, shuffling our schedules around meetings and phone calls has been inconvenient. Doing some of the work ourselves because we can’t afford to hire someone out-of-pocket is frustrating.” Yoder is holding out hope that Allstate will come around on her roof; it’ll be hard to contemplate the future until the repairs are complete. “For now, we are trapped.”

In an emailed statement, Allstate said it “promptly paid all the agreed upon amounts” from the customer’s claim and that it was “working actively to resolve any remaining differences and thoroughly investigate all open claims to ensure accurate and timely payments to our customers.” The company noted that Allstate has settled 98% of its Iowa derecho claims and provided customers over $120 million to recover from their losses.

When the derecho caused a tree to fall on Marie Hancock’s southeast Cedar Rapids home, resulting in damage to her garage and dwelling, she felt more confident than most in her ability to navigate the situation. As a realtor, she understood the fine print of policies and the tedium of the claims process. But nearly a year later, she’s surprised to be in a situation similar to Yoder’s, with her garage still not functional and her roof in need of repair. Water seeps into her home anytime it rains heavily, worsening water damage within. The $12,000 she and her husband received for their claim feels hard-won—a first adjuster told her there was nothing wrong with her property; a visit from the second yielded a payment of $4,000—but also far less than what she believes she is owed under her policy. “We’re not in Florida,” she said, still a little stunned by what she’s witnessed. “They’ve had years of collecting premiums with very little payouts [here].”

Originally from Togo, in West Africa, Hancock feels discrimination has made her family’s battle tougher—she hired a public adjuster for that reason—and she’s noticed a similar pattern with immigrant families she’s helped through the process. With her own battle, she is close to conceding. “I don’t have energy to spend fighting a system that I know is very well structured [to the benefit of insurers],” she told me in late July, adding that she and her husband plan to refinance their home and use that money to fix what the insurance money hasn’t covered.

The story of John and Jodi Philipp is another specific and complicated case. Their losses and circumstances are extreme, but according to those who have dealt with derecho cases, the battle with their insurer follows the patterns of others. For more than 20 years, Jodi and John Philipp had what they thought was a $1 million homeowners insurance policy through Benton Mutual Insurance Association, which, founded in 1872, is one of many small farm mutuals that serve Iowa’s rural communities. Headquartered in Keystone, Iowa (pop. 600), 10 miles west of Van Horne, it offers home and farm insurance in a 19-county area in eastern Iowa; more than half its policyholders were affected on the day of the derecho. Like many homeowners, John and Jodi didn’t think much about their policy, which they originally purchased through an agent in Vinton, another nearby town, and renewed every year. The policy, which has an annual premium of $1,718.30, covered the couple’s home well as the garage, the riding arena, and personal property.

The couple had never filed a claim, and so in the wake of the derecho Jodi was surprised to learn she actually had a $673,000 policy with a restrictive roof endorsement stating that Benton Mutual would “not pay for loss to roofs caused by windstorm or hail until acceptable repairs have been made or a new roof is installed.” The roof endorsement, which Fortune has seen, is dated August 2017, and John Philipp’s name had been printed in for a signature by an insurance agent, with the note “by phone 10:18 a.m.” Neither John nor Jodi remembers a conversation with an agent about the endorsement, or ever agreeing to it. (The insurance agent did not respond to multiple requests for comment; Benton Mutual declined comment on individual claims.)

That piece of paper is key to the Philipps’ dispute, as Benton Mutual argues it absolves it from covering roof damage or anything inside the house that was damaged because of a faulty roof, according to the public adjuster and attorney hired by the Philipps. It also reflects what Amy Bach, an attorney and the executive director of United Policyholders, the nonprofit she cofounded in 1991, calls a “problematic” trend in the insurance industry: the quiet modification of homeowners’ insurance policies.

“Because of the increasing number of wind and water events associated with climate change, insurers have gotten more and more aggressive in limiting what they pay for roof damage and roof repairs,” she explained, dating the start of the practice to around 2013. “That’s a problem that’s come home to roost in Iowa, and in a situation like the derecho because it involved wind and rain.”

Bach said such changes, which reduce the value of homeowners policies but rarely the cost of them, are usually not communicated clearly to policyholders, and have been implemented too quickly for homeowners and regulators to keep up. (Ommen said this is another issue the IID is examining in light of the derecho.) Bach’s organization launched a national initiative, Restoring the Insurance Safety Net Coalition, in 2020 to bring to regulators, officials, and courts an awareness of the issue and to institute standards that prevent excessive coverage-shrinking policy rewrites. What, after all, is the value of a house with no roof?

Very little, the Philipps would discover, according to the report prepared by NCP Group, a Florida-based company that Benton Mutual had hired to adjust and process claims. The company determined covered damages, or the actual cash value of damages to their three-story farmhouse, to be $16,786.17. “It was almost comical,” Jodi told me. “They wanted to give us [a payment] to the paint the rooms in the house when the ceilings are caving in.” Despite appeals and the help of a public adjuster Jodi hired (which assessed the covered damages as exceeding their $673,00 policy), NCP Group hasn’t sent another adjuster to reinspect the place to the knowledge of Jodi or anyone representing her. The first adjuster no longer works for NCP. (NCP does not comment on individual claims.)

The public adjuster secured a few additional payments for the property, but nothing close to the firm’s huge estimates. And when those efforts stalled, Jodi’s relationship with the public adjuster—once a source of so much hope—soured. She couldn’t get answers from the firm either.

As with others I spoke with, my sense from Jodi was that the most upsetting part of this process was its lack of humanity: the fact that at a time of extraordinary personal loss and trauma, the people they depended on for help didn’t return calls or texts; that they communicated things poorly, if at all; that an adjuster or contractor or public adjuster would just up and disappear, sometimes replaced by another one, restarting the whole process, and sometimes not. It’s a pattern that seems to happen after widespread disasters, like this one, where there’s a scarcity of time and resources.

It’s at this point that Jodi returned to one of the Derecho Facebook groups, which led her to Greg Usher, a young and energetic attorney who grew up in the Cedar Rapids area and eventually found his way to property and casualty claims. By early 2021 he was getting eight or 10 calls a week and working nights after putting his young son to bed. After reviewing so many issues, he had reached the depressing conclusion: “Almost everyone’s getting screwed.” When we spoke in early June, he seemed both exhausted from the past year and freshly outraged by it, rattling through the worst practices of the major insurers and the upsetting things he had come across. There was his client Becky Hudson, whose house had been crushed under a tree and her basement—where she ran a home day care—flooded with sewage. She had dealt with multiple Allstate adjusters, including one who suggested she just clean, rather than replace, the day-care items that had been contaminated by the sewer water. Usher believes Allstate has underpaid her claim by more than $100,000. (Allstate said it had promptly paid all undisputed damages from the claim, and that “all open claims are thoroughly investigated to ensure our customers receive accurate and timely payments.”)

He’s now shepherding the Philipps’ case through appraisal, a dispute resolution process that, while not without risk, is quicker and less expensive than litigation. He says communication with Benton Mutual’s attorney has been positive as they prepare for a joint inspection of the Philipps’ property. While Jodi’s case is far from resolved, she is feeling more hopeful now that it is in Usher’s hands and that this miserable chapter—“the worst frickin’ year,” as she described it—seems to be inching toward an end. In recent weeks, with Jodi having secured the Chelsea city council’s approval, Kringle and the reindeer moved to Periwinkle Place. She is fixing up a structure on the property for her and John to move into, and she has begun hosting murder-mystery events again. She is coming to accept that she will probably never again live at the farm and is instead trying to remember that beyond this insurance battle and the limbo of the past year, there is a future.

Subscribe to Fortune Daily to get essential business stories straight to your inbox each morning.