In 2018, the Tesla board fashioned a 10-year pay plan for founder and CEO Elon Musk that so far stands as the most successful long-term compensation blueprint in history. The structure is highly innovative in rewarding Musk for raising Tesla’s market value, and it has delivered brilliantly. In the just over three years the program’s been in place, Musk has multiplied the EV pioneer’s value 12-fold to $647 billion at the market close on March 9. Musk hit many of the laddered targets that trigger the awards years earlier than the board could possibly have anticipated, leapfrogging one market-cap goal after another. His reward is what this writer anticipates to be the largest stock options award, secured in a brief period, in the annals of capital markets: $31.7 billion since May 2020, including over $10 billion alone in the first quarter of 2021.

Musk deserves every one of those multiple billions. Although the numbers sound mammoth, his big take is being paid out of what he created. In fact, it’s such a small sliver of the mountain of value he’s built that it’s costing his shareholders relatively little in dilution. That’s how a great comp plan is supposed to work.

While the Musk model has proved a runaway winner for folks and funds who’ve held his shares in the past, it’s a lot less promising for investors buying today. This is a 10-year plan that triumphed so fast that it’s mostly gone obsolete after just three years. “The plan’s a victim of its own success,” says Bennett Stewart, cofounder of consulting firm Stern Stewart and developer of the economic value added, or EVA, tool for squeezing maximum profits from each dollar in added capital. “The original was great because it resembled leveraged stock options; they vested only if Musk raised Tesla’s value. But now he’s satisfied all the market-cap metrics before anyone dreamed he could. What’s left are sales and Ebitda goals that a CEO could gin up without increasing a company’s value.”

First, let’s look at the building blocks of Tesla’s “2018 CEO Performance Award.” The program grants Musk the right to purchase options in 12 equal tranches of 8.45 million shares each. At the plan’s origin in late 2017, each slice represented 1.0% of Tesla’s shares; today, grants to employees and new stock offerings have lowered the dilution caused by each award to 0.88%. Musk’s strike price is $70, at which Tesla was selling when the program launched. Since its shares closed at $693.73 on March 12, one award is worth a mind-boggling $5.271 billion, net of the $70 purchase price.

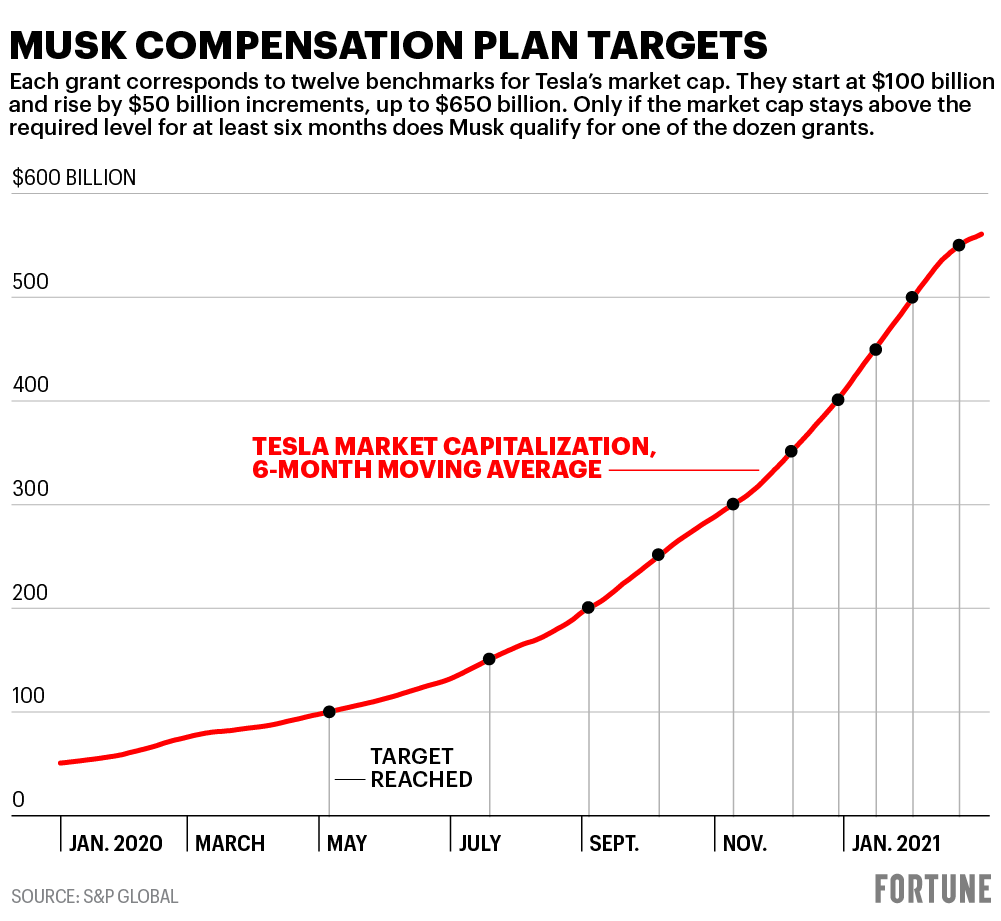

Each option grant corresponds to 12 ascending benchmarks for Tesla’s market cap. They start at $100 billion and rise by $50 billion increments, so that for Musk to win the 12th and final award, Tesla’s valuation would need to hit $650 billion for an extended period. Only if Tesla’s market cap, based on its average price, stays at or above the required level for at least six months, and has met that mark for the 30 days prior to reaching the six-month goal, does Musk qualify for one of the dozen grants.

Musk doesn’t automatically collect a heap of options by just meeting the market-cap goals. For a grant to vest, he also must achieve one revenue or Ebitda target. Think of the plan as a vault filled with 12 safety-deposit boxes, each of which requires two keys to open. For each box, the first key is released for hitting targets for valuation; Tesla hands Musk the second key if he also reaches one new operational benchmark that can be either a target for revenue or Ebitda. Only with two new keys in hand can Musk unlock the next treasure chest. Platinum handcuffs go along with the keys: Musk must also continue as CEO, or serve as both executive chairman and chief product officer, in order to receive the grants.

Each sales and Ebitda category has eight milestones that get increasingly difficult. Those 16 goals (or “keys”) are more than enough to open the 12 boxes in the vault. That gives Musk some latitude, since once he reaches the valuation bogeys—as it turned out, a feat that he’s mostly accomplished—he could win all the awards and open all the boxes by hitting 12 of the 18 operational marks. Each operational key can be used only once, and they’re hard to obtain because the numbers ramp up fast. For revenues, the eight levels start at $20 billion and rise to $175 billion; for Ebitda, the tiers run from $1.5 billion to an eighth and final target of $14 billion.

The program was structured so that even if Musk aced the valuation marks, he’d only get the next grant if he kept reaching higher and higher benchmarks for sales or Ebitda, enabling him to secure that second key.

Sounds like a great blend that demands big rewards for shareholders while ensuring that Tesla’s underlying business grows robustly. The problem is that Musk has already beaten or is close to beating almost all the market-cap targets way ahead of any conceivable schedule. Now he can unlock the next grant by hitting any one of the sales or Ebitda bogeys that he hasn’t yet reached. He doesn’t have to nail a revenue and profitability objective at the same time. As we’ll see, he could even get most of the remaining grants just by increasing sales.

When the Tesla board introduced the program in January 2018, the EV-maker’s cap of just over $50 billion was around half the requirement for the first award. Amazingly, Musk didn’t get “in the money” until the huge run that began in April of last year brought its trailing six-month valuation to well over $100 billion during the spring of 2020. As Tesla disclosed in its May proxy and also its 10-K in February, Musk won his first tranche in the June quarter by first reaching the $100 billion market-cap goal, and second registering sales, based on the trailing 12 months, of over $20 billion.

By the end of September, Tesla’s price had soared in six months from $150 a share to around $400, raising its average market cap in that period to over the $200 billion required to qualify for tranches two and three. By Q3, Tesla’s Ebitda was running at an annual pace of $5.1 billion. That enabled Musk to exceed the first two Ebitda goals of $1.5 billion and $3.0 billion. Hitting both enabled him to pocket the next two tranches. Officially, he won tranche two by matching the market-cap goal with scoring $1.5 billion in Ebitda, and tranche three by reaching $3.0 billion.

By the December quarter, Musk had climbed to the fourth rung in valuation, exceeding the $250 billion bogey. His Ebitda waxed the next leg of $4.5 billion. The combination handed Musk the two keys unlocking the fourth tranche.

By early March, Tesla was on such tear that its average, six-month market cap had reached over $550 billion (it hit a high of $837 billion on Jan. 22). That was already big enough to qualify for grants five through 10. Musk is likely to achieve two operating goals in the current quarter that will reap awards five and six. Beating the next Ebitda target of $6 billion over trailing four quarters should be a breeze since Tesla already posted $4.9 billion from June through December. It should also easily reach the next $35 billion sales milestone. Put those two operating beats together with the giant market-cap beat, and Musk should amass awards five and six in the March quarter.

Musk’s total haul comprises four tranches of 8.45 million shares each from June to December, with another two to come by the close of March. That’s a total of 50.7 million shares. At the March 12 closing price of $693.73, he’ll be holding options on $35.2 billion in shares at face value. As of the latest proxy filing in late May 2020, Musk has exercised a tiny number of options that he had exchanged for $30.5 million in Tesla shares, all of which he still owned. If he does exercise options granted under the 2018 plan, he can’t just pocket the cash difference between the strike and market prices. He has to purchase the underlying shares and hold all of them for at least five years before he can sell.

Right now, the value of Musk’s grants is that $35.2 billion less that $70 “exercise price” he must pay to acquire the shares, amounting to $3.55 billion. Hence, Musk’s six grants since June of last year will have lifted his net worth by an astounding $31.65 billion by the close of the March quarter, if Tesla’s price remains near the current level.

As of today, Tesla’s average valuation over the past six months is on the cusp of exceeding $600 billion. If Tesla settles at its current market cap of $661 billion, it will soon reach that goal. That qualifies Musk to receive five of the six remaining tranches. Sustaining its current valuation of $666 billion would put Musk in the money for slice number 12. What was designed as a super-long-term incentive is paying off incredibly fast, both for Musk and his shareholders.

Ebitda and sales

But Musk has already rung the bell on market cap. Raising Tesla’s valuation from here won’t get him any more grants. That destination’s in the rearview mirror as he speeds ahead. Sure, Musk would like to see his shares appreciate a lot more, since he has options to buy over 50 million of them at just $70. But huge money, another $30 billion at today’s price, now depends entirely on hitting targets for Ebitda and sales.

Stewart notes that the original plan was superbly fashioned because for Musk to win every tranche, he had to greatly increase Tesla’s value. “It would have been bad if it was just Ebitda and revenues,” he says. “But requiring better and better shareholder returns was baked into the plan. Coupling that with sales and Ebitda was good because it ensured that he’d have to build a business with substance behind it, and not just get paid if the stock was in a bubble.”

“I can’t criticize the overall plan; look at the results,” says Stewart. “But it isn’t optimal going forward. He’s already burst through 10 years of market-cap performance in three years. Now it’s all about sales and Ebitda.” Put simply, Tesla’s board needs a better way to motivate its superstar in the years head.

Hence, Musk can come out way ahead by pocketing huge grants if he increases those two metrics, even if Tesla’s market cap flatlines or falls. So far he’s hit, or will soon hit, only two of the sales goals. Achieving strong revenue growth alone could unlock all six of the remaining grants, without reaching any of the Ebitda targets designed to require rising profitability. This is a major weakness in the plan going forward.

Building the business from scratch required Musk to lavish giant amounts of capital on producing a revolutionary product. Now he needs to focus on profitability. Carefully targeting new investment spending will be critical to that effort. Musk can keep rewarding shareholders only by garnering high returns on each dollar Tesla invests in making cars and batteries. The company must resist spending gobs of capital to gun sales.

The current plan is already out of date, because it would reward Musk for spurring revenues at all costs. Pouring capital into models with relatively low margins or cutting prices to sell a lot more EVs would boost sales. Those go-go strategies would backfire by blunting what Musk’s done so phenomenally well, but at these prices will be a far harder going forward: keeping Tesla’s share price marching upward.

Stewart says that the board should recast Musk’s comp plan to incorporate either new incentives based on raising Tesla’s valuation from here, or an EVA-like measure that rewards him for generating high returns on capital while rapidly growing the business. Tesla needs a comp plan part 2.0 to keep its superstar driver in the fastest of fast lanes.