André Kostolany had a knack for beating the biggest crises of the 20th century, pocketing huge profits during the Great Depression and later during Europe’s post–World War II reconstruction. The Hungarian-born economist and stock picker famously observed that the relationship between the stock market and the economy is akin to a dog out for a walk with its owner.

The master, holding the leash, and usually behind the dog, is like the economy, he explained. The dog, darting ahead, is the stock market. Kostolany’s point: We should give the stock market credit for anticipating the future.

Read more: From bailout debacle to global dominance: Inside the turnaround at UBS

“We are now in a period where it makes sense for the markets to move ahead,” says Holger Schmieding, chief economist at Berenberg Bank in London, who’s still fond of Kostolany’s metaphor. Schmieding says the markets are scampering forward in the belief we’ve begun to beat back COVID-19—even if the economic data has yet to bear that out. And if we’re listening to the stock markets, they’re increasingly chanting: Europe, Europe, Europe. Even during the epic August equities rally, as the Nasdaq and S&P 500 were climbing to new heights, investors were trading out of U.S. stocks and into European stocks. According to Goldman Sachs, in the four weeks leading up to Sept. 9, investors pulled a combined $17.7 billion out of U.S. equities. Over the same period, they put $1.5 billion into non-U.K. European stocks. To wit, Germany’s blue-chip DAX has outperformed all three major U.S. indexes over the past month.

There are a number of reasons investors are risk-on European stocks. For starters, investors got spooked by sky-high U.S. tech-stock valuations. Emerging from the August rally, the Nasdaq 100 was trading 41% above its 200-day moving average. Compare that to the DAX, which was trading 1.4% over its 200-day moving average on Sept. 10.

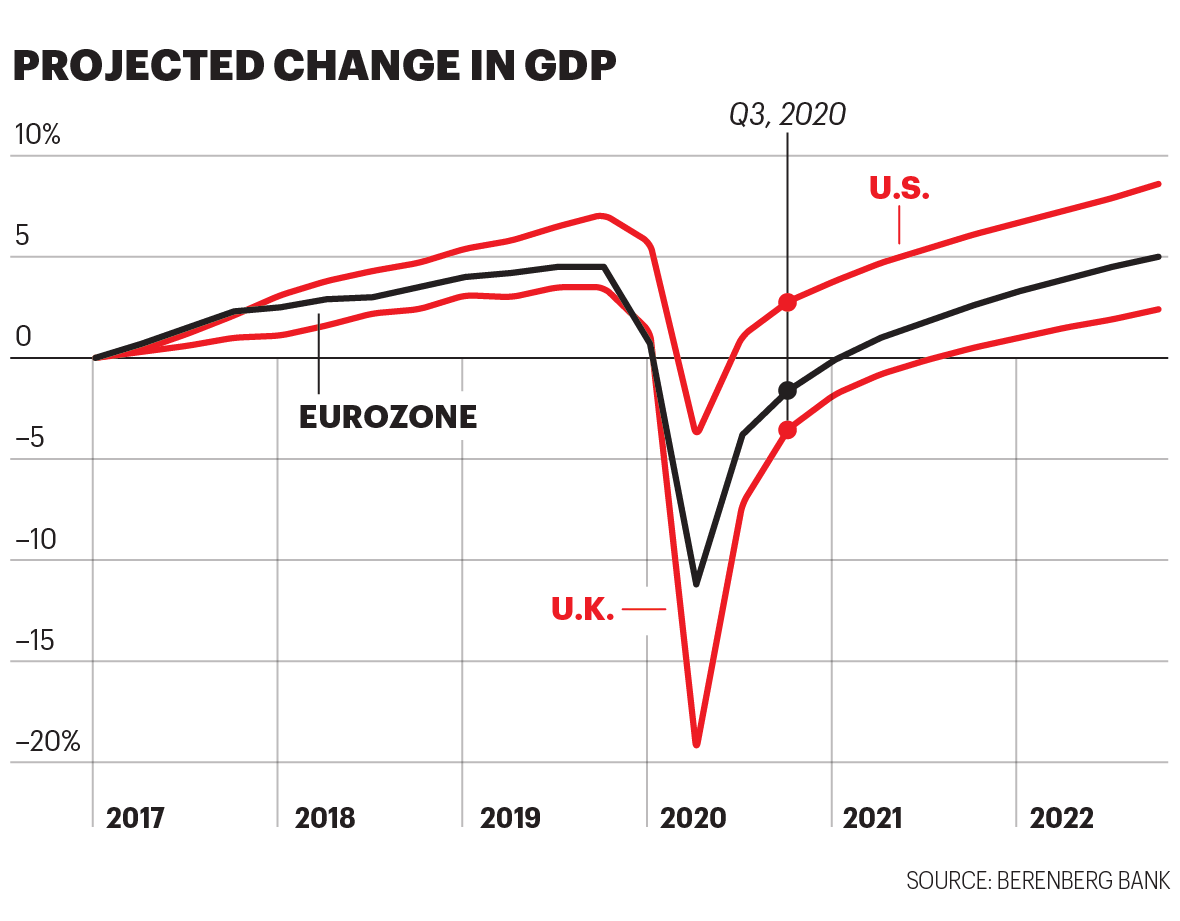

But there’s also a case of Kostolany’s dog principle at play here. The markets believe Europe has done a relatively better job managing the pandemic than the U.S., therefore setting the eurozone recovery up as a real growth play. There’s sound data to back this up: The eurozone fell further in Q1 and Q2, and as such, like a growth play, presumably has more ground to pick up as the recovery accelerates (see chart below). U.S. recovery, meanwhile, is already baked into most U.S. equities high-fliers.

Does that mean Europe will emerge from COVID in better shape than America? Berenberg’s Schmieding thinks so. The U.S. economy will reach pre-pandemic GDP in Q2 2022, around the same time as the eurozone’s biggest economies, Germany and France. But, he adds, “the eurozone clearly is emerging in better shape.”

By Berenberg’s forecast, the U.S. will run a fiscal deficit in 2020 of 18% of GDP, compared with 11.5% for the eurozone. “Even starker,” he adds, “we expect the U.S. to maintain a very elevated fiscal deficit: 12% next year, compared to the eurozone’s 6.2%.” For 2022, he expects a eurozone deficit of around 3.5% of GDP, and closer to 11% for the U.S.

And, Schmieding warns, that “debt is not free forever.” Those heady U.S. deficits must be reined in eventually, which could prove painful for U.S. companies and investors.

All of which means that slow-growth Europe, which investors ignored for years, may be ready to run with the big dogs.

A version of this article appears in the October 2020 issue of Fortune with the headline “Europe shakes off its slow-growth reputation.”