While the stock market is hitting new all-time highs, so is another more alarming statistic: the amount of debt held by corporations, especially the riskiest kind.

U.S. corporate debt (excluding financial firms) surged more than 50% since 2008 to around $10 trillion, a record 47% of gross domestic product, according to the St. Louis Federal Reserve Bank. The flow of easy money meant C-suite dreams could come true: Managements used the cut-rate borrowed money for new product launches, acquisitions, stock buybacks, dividend boosts—all the hallmarks of the economy’s current expansion.

For Corporate America, heaping on all this corporate debt in recent years seemed rational, after all, it’s a bargain! Following the terrifying 2008-09 global financial crisis, an indulgent Federal Reserve and other central banks eagerly pushed interest rates very low, bidding to revive capitalism’s crushed animal spirits. “Debt’s been cheap, so why not do it?” said Jim Schaeffer, deputy chief investment officer of Aegon Asset Management.

Along the way, though, the credit quality of that growing debt pile has slipped. During the recovery from the Great Recession, the portion of the market made up of investment grade bonds fell to 78.6%, from around 90% in the previous two recoveries, says consulting firm Deloitte. Making matters worse, bank loans to highly leveraged companies are growing, and restrictions on risky debt issuer behavior, called covenants, are much weaker nowadays.

“The magnitude of the next spike in default rates, whenever it occurs, will be severe,” said Edward Altman, professor emeritus at New York University’s Stern School of Business and director of the Credit and Fixed Income Research Program at the NYU Salomon Center. The pain will last longer than is typical, he believes, and more money will be lost than normal through defaults.

With more junk debt around, Peter Schiff, CEO of Euro Pacific Capital, wrote in a recent blog post: “This is a giant house of cards just waiting for something to nudge the table and send the whole thing toppling down.”

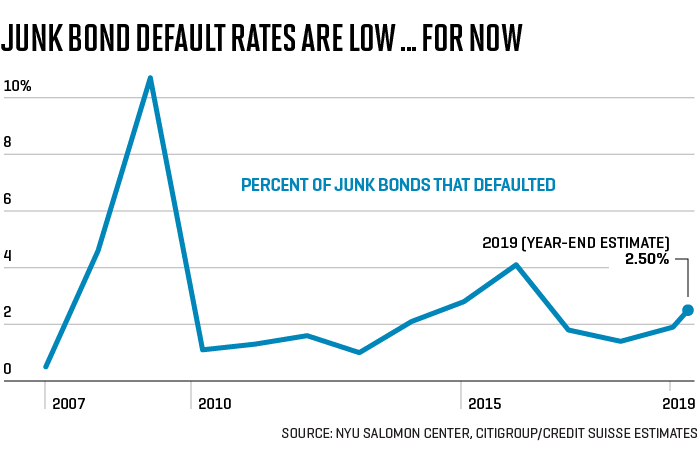

Today, outstanding high-yield bonds in the U.S. total $1.5 trillion, up from $700 billion in 2007 (or $869 billion if inflation-adjusted). When a recession hits, revenues and earnings dry up, and junk default rates tend to surge into double digits. In the last recession, high-yield default levels soared to 10.7%, by Altman’s estimate. For the two downturns before that, they peaked at 12.8% in 2002 and 10.3% in 1991. During the current recovery, defaults temporarily blipped up to 4.1% in 2016, after the oil-price bust lowered earnings and U.S. economic growth.

Feeling the pain

The trouble, when it hits, will mostly be concentrated in companies with below investment grade designations. Gimme Credit, a well-regarded bond research house, lists 10 high-yield issuers whose bonds are most likely to under-perform for investors. They range from auto renter Hertz to apparel purveyor Limited Brands (parent of struggling Victoria’s Secret) to casino company Mohegan Gaming & Entertainment.

Drugstore chain Rite Aid, also on the Gimme Credit’s list, is emblematic of a precarious, debt-laden corporation. Its leverage ratio is high, more than three times what’s considered safe: Rite Aid’s long-term debt is 6.8 times the money the company generates in earnings before interest, taxes, depreciation and amortization, or EBITDA. Amid bruising competition, the chain has been in the red for its last fiscal year and the first two quarters in this year.

While drugstores aren’t a cyclical industry—people always need prescriptions, toothpaste and Band-Aids—Rite Aid’s financial picture is wobbly enough to make investors worry about its future. Its same-store sales growth shuttles between negative and anemic. Over the last three years, the stock has tumbled 92%.

Certainly, no one can predict whether a stressed company today will be in Chapter 11 when the recession arrives. But the hammer blows of a bad economy will probably make things a lot worse, as it increases the likelihood that a company can’t pay interest or return principal when it’s due.

Calm before the storm?

Amid the junk market’s present calm, admonitions like Altman’s and Schiff’s seem alarmist. Thus far this year, the U.S. junk default rate is a low 1.9%, well beneath the 3.3% historical average. Demand is healthy for speculative paper, since its interest rates are enticing in a low-rate world. “Investors will reach for yield these days,” said Bill Zox, chief investment officer for fixed income at Diamond Hill Capital Management.

As buyers bid up prices, most junk bonds have seen their average yields drop in 2019: B-rated junk, for instance, has fallen to 6.0%, from just over 8.45% in early January. (Prices and yields move in opposite directions.) Bank of America’s high-yield index has climbed 11.6% year-to-date.

What’s troubling, however, is that investor confidence doesn’t extend to the lowest level of junk, CCC. Investors are dumping the CCCs, much of them from woebegone energy issuers, before something bad happens. This little-noticed development has prompted worry that the CCC selloff might be the harbinger of a malaise that will spread to other junk issues.

Future imperfect

Once cash flows dry up in a recession and big interest payments loom, look out. Then, everything can go to hell very quickly. Small cracks become major fractures. Aware of their debt exposure, many companies—whether in the junk yard or not—are preparing for a change in the financial weather by de-levering as best they can.

Junk-rated Rite Aid has made valiant efforts to shed its big debt load, although it has a long way to go and tight resources to get there. Rite Aid has the misfortune of being the distant third in the U.S. drugstore chain realm, behind Walgreens Boots Alliance and CVS Health. Attempts to merge fizzled with Walgreens and later with food and drug retailer Albertsons. To raise cash to retire debt, Rite Aid ended up selling almost half its stores to Walgreens, which had the added effect of crimping revenue going forward.

Citing operational shortcomings, Standard & Poor’s in April downgraded Rite Aid to B- from B, following weak results in its just-concluded fiscal year. Recently, management repurchased $84 million worth of bonds at a 39% discount and offered to buy in another $100 million at a similar level. Rite Aid is paying for this via a revolving loan facility that apparently charges less interest than the bonds pay out, 7.7% and 6.875%.

That tactic landed the chain in trouble with S&P, which branded the repurchase a “distressed exchange” because the maneuver offered investors less than what they had. The agency lowered Rite Aid’s junk B- rating to a category called SD, for selective default.

Rite Aid responded, through a spokesman, that this designation is “temporary and common in these types of transactions.” S&P added that it will reevaluate the issue once the company’s offer is complete.

The company notes that its next bonds aren’t slated to mature for a while, with the first due in 2023. In remarks at the drug chain’s second quarter earnings call in late September, new CEO Heyward Donigan said, “Rite Aid needs a clear new strategic vision and a pathway to execution that drives future organic growth and profitability.”

No one can tell how Rite Aid and others like it will fare when the chill recession winds blow. But one thing’s for sure: there’s always payback time.

More must-read stories from Fortune:

—Saudi Aramco being crowned world’s biggest IPO hinges on the “greenshoe”

—Fortune poll: Two-thirds of Americans anticipate a 2020 recession

—Want stock market buying opportunities? There’s always a bear market somewhere

—The stock market has hit 19 new highs in 2019 alone. Why?

—The 2020 tax brackets are out. What is your rate?

Don’t miss the daily Term Sheet, Fortune’s newsletter on deals and dealmakers.