Alarms were going off in the stock market today. And what pulled the cord was a slight change in the interest rates of Treasurys.

Early Wednesday morning, the interest rate on a 2-year Treasury was slightly higher than the interest on a 10-year, an event called a yield curve inversion.

By market close, the Dow industrials were off 800 points, or 3.05%. The S&P 500 was down 85.72 points, which is 2.93%. And the Nasdaq lost more than 242 points, or 3.02%.

But understanding why the yield curve has gained such importance—even Donald Trump tweeted about the CRAZY YIELD CURVE today—and whether it’s sending true or false signals at the moment, is a little complicated.

Yield curves are a way of comparing the interest rates of the different maturity-date bonds a country issues—like U.S. Treasurys. In a normal market, interest rates (called yields) for longer-term bonds should be higher than those for shorter-term ones, because investors tie their money up for a longer time and want a greater reward for doing so.

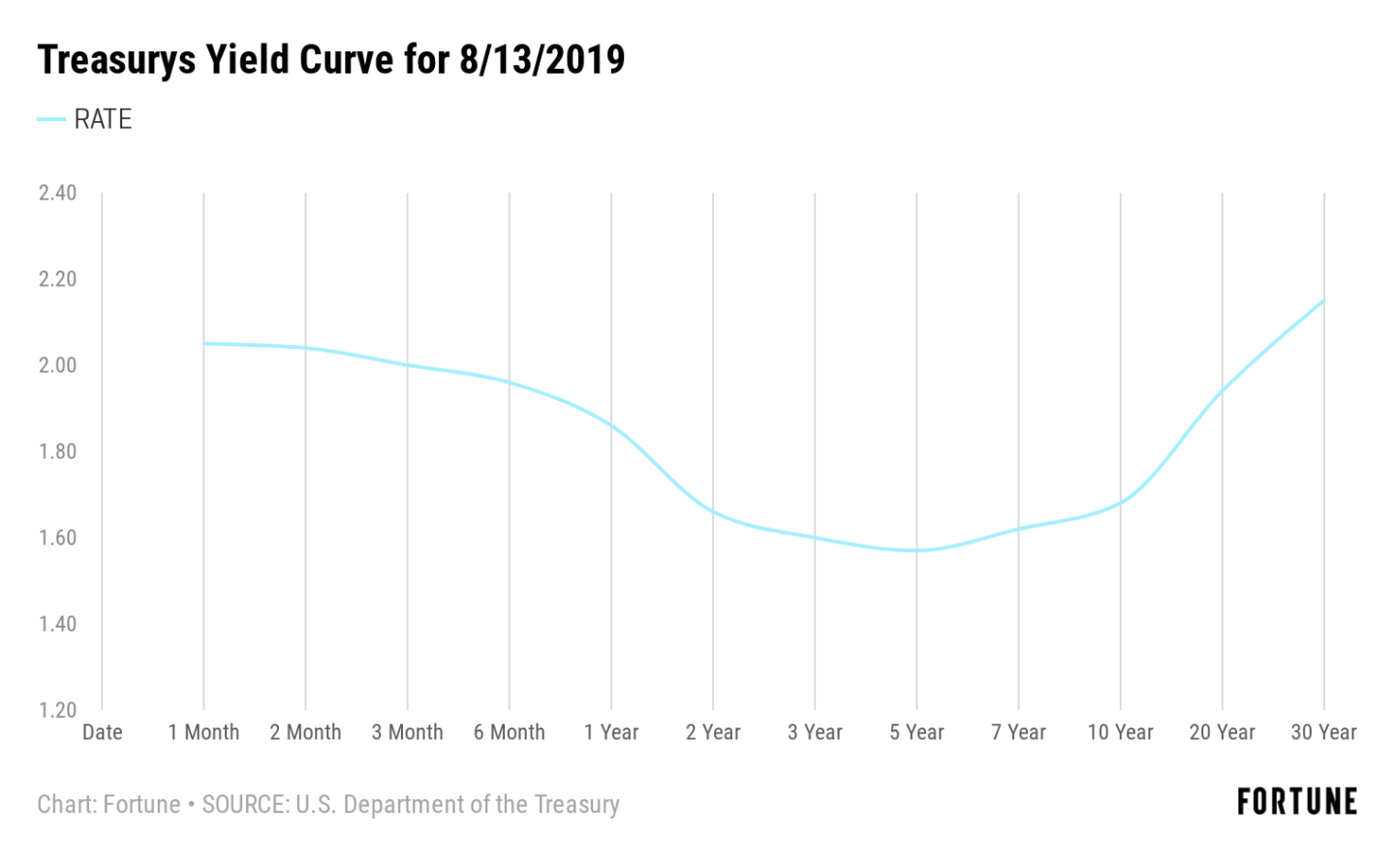

The yield curve is a graph of the interest rates for varying maturities: like 3-months, 6-months, 1-year, 2-years, 5-years, 10-year, 30-year, and so on. A line is drawn through the plotted points to show a curve. Below is an example for the yields on Aug. 13, 2019.

This is not a normal yield curve, even without a brief time where the 10-year yield was a little lower than the 2-year.

Yield curve inversion

Typically, the curve bends upwards because the shorter-term maturities on the left of the graph have lower yields than the long-term maturities toward the right.

However, sometimes shorter-term maturities offer higher yields than longer-term ones, resulting in the curve sloping downward from left to right. That’s called a yield curve inversion, because it does the opposite of what people typically expect.

Inversion is important because of its status as an indicator of coming economic recessions. When short-term rates are higher than long term, it indicates the potential for a future recession because the numbers indicate that investors think the short-term economy is a better bet than the long term.

In this case, instead of a clear climb one way or the other, there’s a dip in the middle—more on that in a minute.

Past inversions

“Typically these inversions occur 12 to 18 months before a recession,” said Andrew Aran, a partner at Regency Wealth Management. But an inversion is just an indicator, as in recent times, only two-thirds of them have actually come before a recession.

But the inversion today is different from the past. “Every recession that we’ve had in the U.S. since World War II, with one exception of the Great Recession, was preceded by the Federal Reserve raising interest rates too far, too fast from much higher levels than the current levels,” said David Kass, clinical professor of finance at the University of Maryland. The Great Recession, which Kass called “one of a kind,” was the result of “an excessive amount of debt in the housing market and the collapse of the housing market and the economy.”

But the Fed just dropped the rate by 0.25% and investors expect as many as three more small cuts by the end of the year. As for debt, “I don’t see an excessive amount of debt in any sector,” Kass said.

What’s going on?

The pattern of the graph above is also not a clear inversion. Very short-term rates start at 2.05%, drop to a low of 1.57% for the 5-year, and then climb to 2.15% for the 30-year. The long-term yield is a bit above the shortest-term. But yields on the 2-year through 10-year are low.

“Generally speaking is what is a little different is a broad flattening across the curve,” said Tim Alt, portfolio manager at Aviva Investors. People may not expect trouble in the long run but are nervous about medium-term prospects. “One way to interpret that is the market is pricing in lower odds that this is a mid-cycle slowdown and higher odds that it is going to end up in a recession,” he said. There is also worry that central banks may have run out of tricks to stimulate the economy. “The concern is that the market is moving toward believing that fiscal policy is the only thing to move the needle,” Alt said.

That means getting politicians to cooperate and forge useful actions that probably involve spending money to stimulate the economy. Such cooperation is going to be hard to find.

Other concerns

But the market’s response has left many scratching their heads.

“I certainly understand the rally in [bonds],” said Steve Massocca, portfolio manager at Wedbush Securities. “The decline in equities is a mystery. And it’s across the board.”

“[Bank stocks] are being sold aggressively today, but their pricing on their loans is more sensitive to short rates” and short rates are holding, Aran said. “That seems to be possibly another over reaction, taking the banks behind the woodshed at an early point.”

It may all come down to a case of nerves. Trade disputes with China and the EU are scaring many. Economies across Europe have slowed, with negative interest rates still in place there and in Japan. The markets seem primed to take everything at the moment as bad news, as the yield curve enters new territory.

Either that or jittery investors are about to talk themselves into a recession.

More must-read stories from Fortune:

—What people get wrong about artificial intelligence and China

—Will Apple will absorb tariffs on Chinese-made products?

—Is it “only human” to feel anxious about money? Talking finance with Sophia the Robot

—The currency that’s quietly emerged as Asia’s safest bet

—Listen to our audio briefing, Fortune 500 Daily

Follow Fortune on Flipboard to stay up-to-date on the latest news and analysis.