It’s the 1990s, the dawn of the Internet age—and you, like everyone you know, has a genius of a dotcom idea. Somehow, you get in to see one of the hottest venture capitalists in Silicon Valley. Your pitch, fired up and ready: You’re going to sell books over the Internet. (The VC yawns.)

You tell him that you’re planning to spend years, or really decades, building up technological infrastructure and warehouse capacity, focusing relentlessly on customer experience—you’ll even call the company “Relentless.com” to capture that ferocious customer-centricity. Sure, you’ll have to discount prices to gain market share, and take a hit on delivery, but in time you’ll have the phenomenal scale to sell “Anything … with a capital ‘A’ ”—to everyone. You’ll be “earth’s biggest store.”

The VC stirs a bit. When he asks you for some hard-number projections, you don’t bat an eye: You and your investors will bleed cash, of course, before you go public. Then you’ll lose gobs more, going 17 straight quarters in the red. You’ll be in the hole about $3 billion in your first nine years as a going concern—and when you do eventually turn a profit, the margins will be razor thin for a decade or more, averaging about 2%.

As elevator pitches go, this one would almost certainly end on the first floor. Except it didn’t. The story of Amazon.com—Jeff Bezos did indeed toy with the name “Relentless.com” before changing his mind (Go ahead: Type it in your browser)—is now engraved into the corporate mythos. The backer was the legendary John Doerr of Kleiner Perkins, who invested an initial $8 million in the company in 1996, and who three years later would back another ludicrously ambitious startup called Google.

What Doerr saw in Bezos (and in Larry Page and Sergey Brin, for that matter) wasn’t just a grand business vision but also the maniacal tenacity to see it through. Others saw it too: In 1999, Morgan Stanley analyst Mary Meeker, a prominent Amazon bull on Wall Street, brushed off concerns of the company’s “aggressive” investment in its infrastructure, calling the strategy “rational recklessness.” Bill Miller, the former Legg Mason fund manager whose 15-year market-beating streak remains unmatched, invested early and heavily in Amazon—and then doubled down on the stock as it careened from triple digits to six bucks a share (after 9/11) and up again. It’s now trading above $1,600, a 106,669% gain over the split-adjusted closing-day price of its 1997 IPO.

Such legend-making is easy in hindsight, of course. Everyone with access to a historical stock chart can plot the last generation’s certain winners and losers. That said, when it comes to gaining wisdom, the past is one of best teachers we have—and the striking rise of Amazon, No. 8 on the Fortune 500 and the subject of a profile by Beth Kowitt this issue (see “Amazon Gets Fresh” on page 90), offers a core management lesson that ought to be carved in tablets by now: Building a great business requires not only a relentless focus on doing things well this minute (what business-book thumpers call “execution”), but also an equally relentless focus on doing things better in the future. As Bezos told my colleague Adam Lashinsky some years ago, “The three big ideas at Amazon are long-term thinking, customer obsession, and a willingness to invent.”

Most of the celebrated company builders of our era—Apple’s Steve Jobs, Walmart’s Sam Walton, FedEx’s Fred Smith, Southwest’s Herb Kelleher, Intuit’s Scott Cook, Salesforce’s Marc Benioff—have known that instinctively. It’s a message reinforced by one biz-school case study after another and preached by the most acclaimed of investors. Warren Buffett, whose investing horizon is the horizon, likes to say his preferred holding period is “forever.”

While the parameters of what defines a long-term-focused company are still somewhat squishy, the limited evidence so far suggests that they make better investments too. At least compared to short-termers: companies that are chasing quarterly earnings targets, buying back stock to pump their share prices, cutting R&D, and slashing other key investments in technology and people. An October study by S&P Global found that an index of large and midsize companies that, it says, “embody long-termism” had consistently higher returns on equity over the previous 20 years than various quartiles of companies with more of a “next quarter” focus. (Working with the Boston Consulting Group, Fortune also unveiled in November a list of forward-looking companies—the Future 50—that steadily reinvest in the capacity to grow.)

A separate February 2017 study by the McKinsey Global Institute, likewise, found far better financial performance from far-horizon companies. From 2001 to 2014, long-term firms, drawn from a data set of more than 600 large and medium-size companies, had an average of 47% greater revenue growth than other firms as well as faster growth of earnings and market capitalizations. Although share prices for this group did suffer more during the financial crisis, they also recovered more quickly, the McKinsey researchers discovered. And from a broader economic standpoint, the farsighted companies also created a lot more jobs than other firms did during the same period.

So why do so many companies still habitually manage to the next quarter? You guessed it: Wall Street. Nearly nine in 10 executives and directors feel mounting pressure to deliver strong financial results within two years or less, McKinsey found. And much of that push is coming from activist hedge funds, many of which are incentivized to goose their own investment returns in the near term.

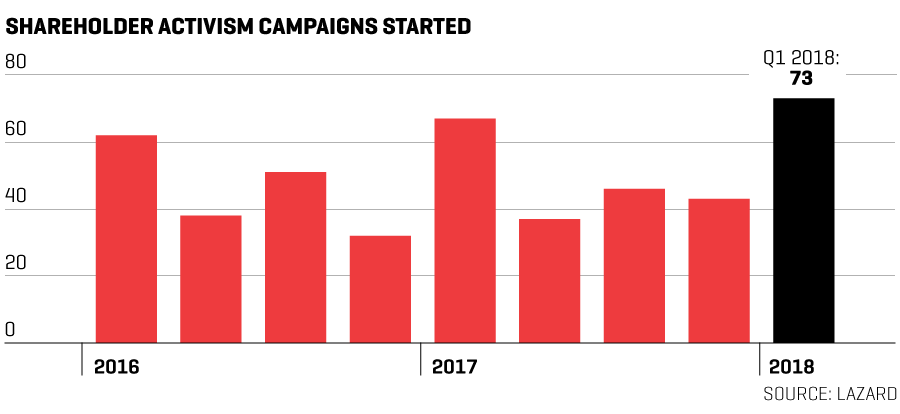

A record 73 activist campaigns, deploying some $25 billion in capital, were initiated in the first quarter of 2018, according to Lazard, which has been tracking shareholder activism for years. Some campaigns push for a breakup or sale of the business; some for share buybacks or a seat on the board (activists won 65 board seats in the first quarter alone). Others are merely interested in “bumpitrage,” Lazard says—that is, to block an M&A deal from going through or to influence its negotiations.

“To be sure there are some activists who actually behave a little more long term than we give them credit for,” says Dominic Barton, McKinsey & Company’s global managing partner, who has been championing efforts to encourage long-termism in corporate suites and boardrooms for more than a decade. These investors can often push for better execution of a far-thinking strategy and get company managements to move much faster in critical areas.

But short-termers dominate this crowd—and their influence is often outsize compared with their shareholdings. “Part of the challenge is that people often sit on multiple boards,” says Barton. “Given the amount of activist activity going on, someone will very likely have had experience with a campaign and will share it with the board,” he says. “It’s a good way to scare the hell out of the other members: ‘My God, you don’t want to go through this! It’s like you’ve come back from a war. You just don’t want to go there.’ ”

An even bigger threat to long-term managing is the way we do CEO compensation, says Fortune contributor Brian Dumaine, coauthor with Dennis Carey, Michael Useem, and Rodney Zemmel of an important new book titled, Go Long: Why Long-Term Thinking Is Your Best Short-Term Strategy. Today, most chief executives are rewarded based partly on how the stock performs during their tenure. Shareholder advocates like Vanguard chairman Bill McNabb are pushing instead to have half or more of the stock compensation vest five years after a CEO leaves the job—which is what Exxon Mobil actually does.

The rationale is straightforward: “If you’re the CEO of an oil company, you can decide to cut way back on exploration and you’d have lower capital spending and suddenly your earnings are going to look great,” says Dumaine. “But five years down the road your successor is going to be in trouble.”

That right there is the problem with short-termism. The great majority of shareholders in the U.S. do hold their stocks for years, if not decades. Inevitably, when managers chase the next quarter, it’s a nation of long-term investors who lose out.

This article originally appeared in the June 1, 2018 issue of Fortune.