If you’ve noticed the prices of of everyday goods are on the rise, you’re not alone.

On Friday the Labor Department announced that the core consumer price index (CPI)—which strips out volatile food and energy costs—rose 2.3% over the past 12 months, up from 1.8% one year ago. “The data help the case for Fed tightening,” writes Jim O’Sullivan, chief U.S. economist for High Frequency Economics.

The futures market concurs. It is indicating that the chance of a rate high at or before the Fed’s December meeting is above 50% for the first time in months. But some analysts are once again calling for the Fed to go ahead and raise rates at their September meeting next week. Their logic: It now appears prices are rising faster than the Fed’s annual 2% goal.

The problem: The Fed doesn’t use CPI to judge its performance, but relies on the personal consumption expenditures (PCE) measure instead.

These two measures aren’t usually that far apart, but have begun to diverge significantly of late. Torsten Slok, Chief International Economist for Deutsche Bank Securities, writes in a research note Friday that this could be a problem for Fed policy makers.

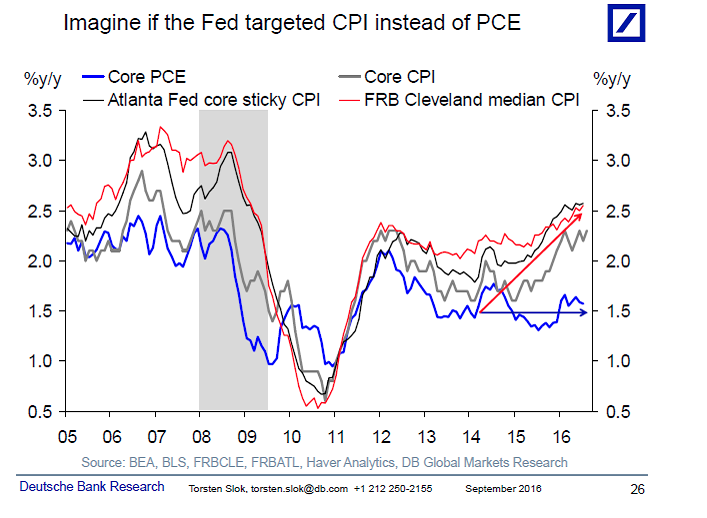

As you can see, there’s quite the gap growing between the two measures, and the Fed targeting the PCE rather than CPI measure could potentially be pivotal. Writes Slok:

The Fed has an inflation target of 2% and most other countries target CPI inflation, but the Fed has chosen to target PCE inflation. As a result, the current narrative from the Fed and in markets is that inflation is not a worry, and the Fed will stay on hold because core PCE is only 1.6%. But, try to imagine if the FOMC instead were targeting CPI, see chart below. In that situation, the Fed is clearly behind the curve because they are already meeting the dual mandate of full employment and inflation at 2%.

The key issue in the chart [above] is if PCE inflation moves up to CPI inflation or vice versa. With the economy already at full employment and more and more signs of higher wage and unit labor cost inflation, the risks are rising that it will be PCE moving up to CPI. In that case, the Fed will no longer have the luxury of being slow, gradual, and cautious, and this continues to be a significant risk to the ongoing hunt for yield in markets.

At the same time, Janet Yellen has said that she’s willing to tolerate a period of time in which inflation is above the Fed’s 2% goal, if that stance can help guarantee that slack is eliminated from the labor market and full employment is achieved. And even if the Fed doesn’t target the CPI specifically, the Fed will still take this data into consideration.

The smart money is on the Fed standing pat next week, but today’s data added some much needed ammunition to the arsenal of Fed hawks as they hope to raise interest rates sooner than later.