For many investors, it may matter little that China reported today that second quarter GDP growth stayed steady at 6.7%, a bit better than economists’ expectations.

That’s because many in the investment community don’t trust the government’s official releases, and for good reason.

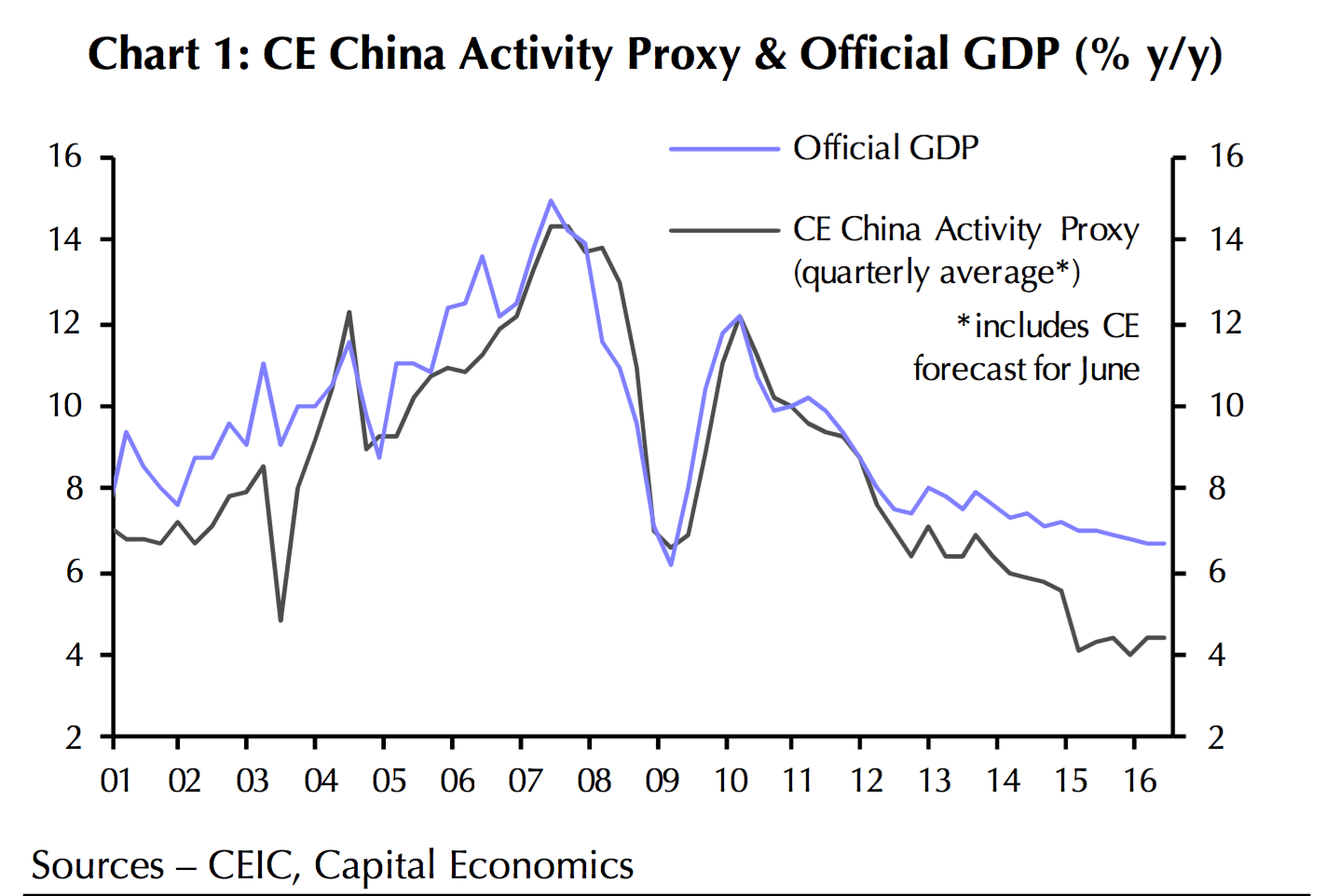

The alternative to the official GDP figure—which is broadly thought to be manipulated—is to use proxy measures of the Chinese economy from private researchers. One such firm, Capital Economics in London, has been tracking Chinese economic activity since 2009 via an index it calls the China Activity Proxy, or CAP.

The firm’s estimate for Chinese economic growth broadly followed the government’s GDP figure until about 2012, when the government’s figure only inched down slowly as the economy hit a wall because of the two-punch combination of massive slowdowns in industrial production and real estate construction.

Now, the firm estimates that second quarter GDP grew 4.5%, more than two percentage points below the official release. But importantly, the CAP rate has stayed as stabile as the official GDP measure. That suggests the Chinese economy has stabilized from an chaotic 2015.

Another GDP proxy showed China’s GDP actually rising, to 7.1%, in the second quarter.

China's GDP steady at 6.7% in 2Q. Our monthly tracker shows an acceleration to 7.1% in June pic.twitter.com/rgTfBD0dlj

— Tom Orlik (@TomOrlik) July 15, 2016

Together the two proxies suggestthat China’s economy is getting its two feet on the ground.

Driving that stability has been a large government stimulus that has included infrastructure spending, relaxed mortgage requirements, and reduced mortgage rates.

But just as stimulus can’t last forever, neither can the political will to continue it when economic times are optimistic, like they are slowly reaching in China. Capital Economics’ economists Daniel Martin and Mark Williams see that as the biggest trouble ahead. “As worries about the outlook have diminished, so has the likelihood of further stimulus,” they wrote today. “Any turnaround would therefore be short-lived and, with structural issues still unresolved, a renewed slowdown over the next couple of years is looking increasingly likely.”