The question “Home Depot or Lowe’s?” can prompt spirited debates among handy homeowners. But for the past five years the answer for investors has been “Both!” Since the beginning of 2011, Lowe’s (LOW) stock has more than tripled and Home Depot’s (HD) has nearly quadrupled, with each company trouncing the broader retail sector and the S&P 500. As customers gear up for this spring’s peak sprucing-and-renovation season, it’s a good time to ask, Can either stock continue its run?

The two companies are “about 90% identical,” notes Oppenheimer analyst Brian Nagel, and both have benefited from improvements in consumer spending and the housing market. Both recently made acquisitions that reflect their growth strategies: Home Depot bought Interline Brands, which sells repair products to property managers, while North Carolina–based Lowe’s absorbed Canadian hardware chain Rona.

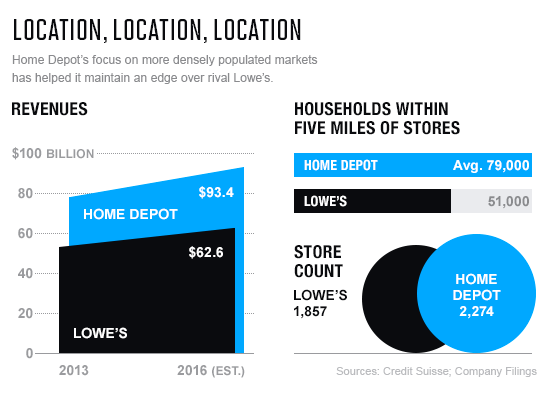

Home Depot remains by far the bigger brother, with roughly 50% more revenue and 2½ times the market cap. Its stock is also about 12% more expensive than Lowe’s, as measured against estimated 2017 earnings. Both the size and the price reflect competitive advantages. Most notably, Home Depot has a bigger footprint than Lowe’s in urban areas and densely populated suburbs. The Atlanta-based chain has an average of 79,000 houses within a five-mile radius of each store, says Credit Suisse analyst Seth Sigman; the average Lowe’s store has only 51,000. During the past five years home values have risen much faster in cities than in suburbs, according to Zillow, and Home Depot has been better positioned to take advantage of the upticks in construction and upgrades that accompanied that growth.

Some analysts think Lowe’s can gain ground by capturing more of the $120 billion professional home-improvement market. The average pro contractor customer at Home Depot spends $6,500 a year, while Lowe’s garners about $2,000 per pro. To narrow that gap, Lowe’s recently launched an e-commerce platform for contractors and began partnering with brands preferred by professionals, like Sherwin-Williams paints. Piper Jaffray analyst Peter Keith says those initiatives could enable Lowe’s to boost its overall growth.

For more on retail, watch this Fortune video:

All this assumes that the economy stays on course and housing prices don’t stall. If the outlook darkens, says Keith, Home Depot’s size and its dominance in urban markets, where housing slumps tend to be shallower, could help its stock outperform the broader market. Bottom line: “Both” is still a good answer for investors who feel bullish about the economy in general, but cautious types should own only the orange-apron option.

A version of this article appears in the May 1, 2016 issue of Fortune with the headline “D.I.Y. Duel: Lowe’s vs. Home Depot.”