Let’s face it—today’s top companies are radically different from the ones we grew up with. The corporate campus has given way to the private home or co-working space. The independent contractor now vies with the full-time employee. And for some, physical products have become digital downloads. The firms built for this new reality—what Fortune calls 21st-century corporations—are rapidly adopting technologies that allow them access to new business models and newer ways of working. Investors should rightly see the companies developing these technologies as attractive investment vehicles, but not all stocks are created equal. We dug into 12 prominent companies working in four promising categories—the Internet of things, data analytics, cloud computing, and artificial intelligence—to see where investors should place their bets. Six are slam dunks. The rest? Well, read on. Here’s how they stack up.

Internet of Things

What kind of “things” make up the so-called Internet of things? Consumer gadgets like intelligent thermostats, smartwatches, and connected cooking scales, sure—but also factory equipment, vehicles, and grid infrastructure that can predict problems and optimize operations.

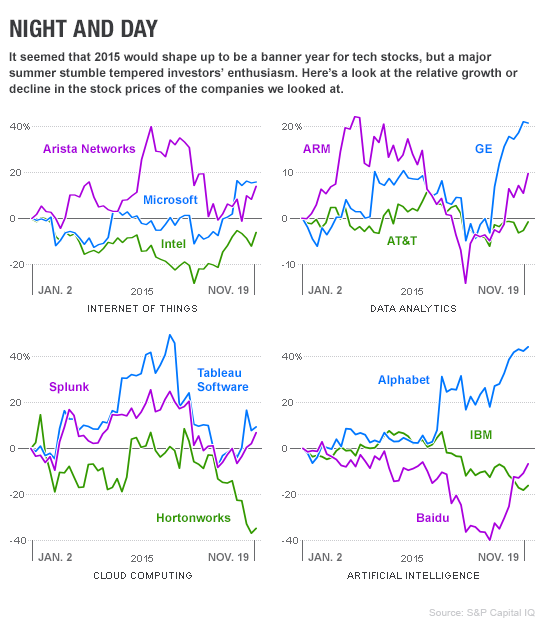

Founded in 1892, General Electric (GE) believes that the “industrial Internet” will serve as the connective tissue between its century-old strengths and a new era. Can an old dog with a $307 billion market cap learn a new trick? GE predicts its revenue from these technologies will total $5 billion in 2015 and $15 billion in 2020. Nick Heymann, a research analyst who follows global industrial infrastructure companies at William Blair, estimates that they can generate up to 25% of earnings by 2020. With such potential, GE is undervalued, Heymann says, and could easily double its share price to $60 by 2020. The Fortune take: Buy.

More than 95% of today’s smartphones use chips based on designs by ARM Holdings (ARMHF). Now the fast-growing British company wants to put them in the connected gadgets that make up the Internet of things. Hans Mosesmann, a managing director at Raymond James, believes ARM’s ability to raise its royalties for all kinds of chips and boost profits makes it a solid long-term investment. Revenue growth doesn’t hurt either: Analysts predict 2016 revenue of $1.7 billion, up 13% from 2015. Our take: Buy.

If every object in the future will be connected, telecommunications giant AT&T (T) wants to be the one to provide that service. A realized Internet of things stands to generate new revenue for a company that made $39 billion in its most recent quarter. But that’s a long way off. In the meantime, growth has slowed in the fiercely competitive U.S. wireless market, prompting AT&T to diversify away from the business with its $49 billion acquisition of DirecTV. A silver lining? AT&T pays a cushy dividend, to the tune of 5.6%, for investors who are willing to wait. Our take: Wait and see.

Data Analytics

When the term first rose to prominence, no one really knew what “big data” was, let alone which companies had it. That’s all changed today. Corporations have built out entire departments to glean insights, find savings, and generate revenue from that information. And data startups are everywhere—though it���s too early for most to be investment vehicles.

San Francisco’s Splunk (SPLK) sells software that analyzes the data generated by corporate systems. Splunk continues to reliably grow its annual revenue—$451 million in 2015; a predicted $650 million in 2016—as it adds customers and renews others like Comcast. It’s expected to become profitable in 2016. John Rizzuto, a managing director at SunTrust Robinson Humphrey, believes that Splunk’s $60 share price is a bit high—the company’s forward P/E ratio is 202.3—but justified as it becomes increasingly trusted among networking and security companies. Our take: Wait and see.

Seattle’s Tableau Software (DATA) sells software aimed at helping regular employees make sophisticated data analyses. It’s growing rapidly: Tableau expects to end 2015 with $620 million in revenue, and analysts expect it to generate $870 million in 2016. “The downside to that is that it’s very expensive,” says Rizzuto, noting Tableau’s forward high P/E ratio of 259.3. Our take: Wait and see.

Then there’s Hortonworks (HDP). The Santa Clara, Calif., company is a major driver of development of Apache Hadoop, the open-source framework underneath many of the largest big-data projects. It is well-known within the data community and has the potential to hit profitability in two to three years, Rizzuto says. Analysts expect the company to rake in $186 million in 2016. But there are reasons for investors to hesitate: “The company is putting a lot of money back into its business, rather than rewarding its shareholders,” Rizzuto warns. Our take: Don’t buy.

Cloud Computing

By now nearly everyone’s heard about “the cloud,” one of the buzziest tech terms of the past decade. The creation of cloud infrastructure and provision of it to other companies have given rise to a generation of Internet-based businesses that outsource the computing resources they need from day one.

Microsoft (MSFT), one of the “big four” cloud infrastructure companies alongside Amazon (AMZN), Google, and IBM, stands to greatly benefit from a cloud-computing era. Its $5.9 billion in cloud revenue in the quarter ended Sept. 30 was up 8% from a year ago, but revenue from Azure, its cloud platform, more than doubled year over year. Though Microsoft’s overall revenue continues to decline, analysts expect cloud growth to reverse that. Our take: Buy.

Known for supplying the chips that power most personal computers, Intel (INTC) also sells chips for the servers in corporate data centers—the machines that make up the cloud itself. That business brought in $4.1 billion in the three months ended Sept. 26. But the steep decline of the consumer market and stiff competition in the enterprise market continue to weigh on an otherwise stable company. Intel must truly innovate, Mosesmann says, to have any chance at prosperity. Our take: Don’t buy.

Arista Networks is not a household name to most, but the 11-year-old company has amassed a roster of big-name customers like Netflix (NFLX) and Salesforce (CRM) by providing networking equipment to power their cloud-based software. Its stock has had a great run; at $73, Arista shares trade 70% above its June 2014 IPO. But Morningstar analyst Ilya Kundozerov says Arista lacks any advantage that would preclude competitors from offering similar technologies. With a forward P/E of 28.5, it’s better at a lower stock price. Our take: Don’t buy.

Artificial Intelligence

The term “artificial intelligence” still invokes sci-fi movie nightmares for many, but the category is on fire as industry realizes the incredible levels of efficiency the technology can achieve.

Revenue continues to decline for IBM (IBM). (Analysts predict total revenue of $81.8 billion in 2015 and $80 billion for 2016.) But its effort to reinvent itself include a big bet on AI in the form of Watson—a layer of intelligence that IBM hopes to add to its various businesses. There’s hope, says Scott Kessler, head of tech-sector equity research at S&P Capital IQ. “We see IBM as an attractive turnaround candidate for 2016.” Our take: Buy.

In 2015 the company formerly known as Google—Alphabet (GOOGL)—revamped its corporate structure to allow further scrutiny of the various efforts (Nest, Google X, Life Sciences) adjacent to its core advertising business. Its dedication to AI spans both its core and experimental divisions and could accelerate the ad business responsible for most of its revenue. (Alphabet is expected to make $85.7 billion in total revenue in 2016.) “Investors can tolerate losses in moon-shot businesses because they’re planting the seeds for longtime growth,” says Colin Sebastian, a senior analyst at Robert W. Baird. Our take: Buy.

Finally there is Baidu (BIDU), which operates China’s top search engine and is often called China’s Google. Though it has been listed on Nasdaq since 2005—it’s trading at about $205 today with a forward P/E ratio of 30.7, higher than Google’s 22—most of its business is still in China. That makes Baidu vulnerable to its economic swings. (Baidu’s share price fell 35% between July and September for that reason.) The company has invested heavily in artificial intelligence as a means of improving its search and advertising businesses. So long as it can keep new competition at bay, Kessler says, Baidu should be well-positioned to maintain its upward trajectory. Our take: Buy.

A version of this article appears in the December 15, 2015 issue of Fortune with the headline “How to Invest in the 21st Century Corporation.”