At 6 a.m. on Thursday, July 23, Heather Bresch was running on the treadmill in her home gym when she found out that four men in Amsterdam had effectively seized control of half her company.

In Bresch’s wild world, this qualified as wonderful news.

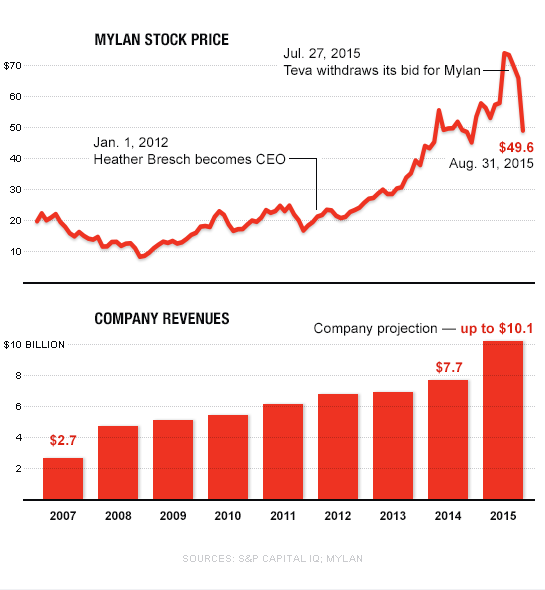

Bresch is the CEO of Mylan (MYL), the generic-drug maker that spent the past summer tangled in a three-way takeover battle with two other drug-industry giants. The Dutchmen’s maneuver, which transferred a large chunk of Mylan shares to a special foundation called a stichting, was the culmination of a strategy Bresch had quietly initiated months earlier. It acted as a poison pill that would undermine Teva Pharmaceuticals’ (TEVA) $40 billion hostile takeover bid for Mylan, taking the power to accept the offer out of common shareholders’ hands. If that bid collapsed, Bresch would be free to pursue the deal she really wanted, an effort she’d launched just before Teva’s offer: Mylan’s own hostile takeover of Ireland-based drugmaker Perrigo (PRGO).

Still, it was too early to celebrate. A couple of hours later, eating breakfast (two hard-boiled eggs, sliced and seasoned) with a reporter in her office at Mylan’s headquarters outside Pittsburgh, Bresch seemed on edge and ready to pounce. Clad in a black leather laser-cut sheath dress and her signature five-inch stilettos, she kept a tense eye on CNBC until she saw what she’d been waiting for: a commentator declaring that the Teva deal was as good as dead.

Mylan’s stock began falling on the news—in fact, its shares would tumble 30% over the next six weeks—but Bresch wasn’t concerned about shareholders’ feelings. Her low West Virginia twang intensified as she stated her resolve to keep Mylan independent at all costs. “We’re not afraid to take the path of resistance, as you’re witnessing today with this love triangle we’re in,” she said, then corrected herself: “Well, not love.”

By the following Monday, Bresch had won: Teva withdrew its offer. The convoluted corporate dance had protected Bresch’s job—and with it, her place as the most powerful woman in the drug industry. But it also thickened the cloud of controversy that has shadowed her career, turning her story into a juicy saga of sexism, drugs, and even rock and roll.

“We don’t cater to Wall Street. And they don’t like that.”

—Heather Bresch, CEO, Mylan

Bresch, a 46-year-old who’s spent more than half her life at Mylan, has steered the company’s transformation from a quirky outfit run out of a West Virginia trailer to a global operator with 30,000 employees in 145 countries. Born into politics—her father, Joe Manchin, is a longtime West Virginia Democratic stalwart who’s now a U.S. senator—Bresch has mastered the regulatory world. Since becoming CEO in 2012, she’s overseen a major revenue increase; Mylan projects sales of up to $10.1 billion this year, up from $6.1 billion in 2011. Today she remains the only woman ever to run a Fortune 500 pharma company—though Mylan was kicked off this year’s 500 list after reincorporating in the Netherlands in a tax-lowering transaction known as an inversion.

Still, Bresch’s accomplishments have earned her … well, not love. Often quite the opposite. As CEO, Bresch has been eclipsed by Robert Coury, her predecessor and mentor, now Mylan’s executive chairman—a brash fountain of expletives who many observers believe still pulls Mylan’s strings. Institutional investors have long accused Coury and Bresch of putting their interests ahead of those of shareholders—a suspicion that Mylan’s rebuff of Teva only deepened. “They’re kind of in the penalty box,” says Marty Sass, a money manager of $7.5 billion who sold half his Mylan stake in July. “Everybody hates them.”

Under Bresch’s leadership, Mylan has also stumbled through a series of ethically messy mishaps and public relations gaffes. Mylan’s inversion took place just as uproar over the tactic reached a fever pitch on Capitol Hill. (Among the politicians who denounced the move was Bresch’s own father, though he later changed his mind.) Critics have called out the company for unusually high executive pay packages, questionable use of company jets, and murky relationships with board members. Then there’s “the Heather Bresch situation,” as she herself calls it, a scandal surrounding her executive MBA credentials—when you Google her name, the episode still ranks even higher than her official Mylan bio.

These stumbles have provided plenty of ammunition for Bresch’s opponents—including Perrigo, which has invoked corporate oversight “failures” in its fight against Mylan’s takeover bid. “Mylan’s governance has always been a weak point for them,” says Bernstein analyst Ronny Gal. The scandals also exacerbate the business-world boys’ club’s tendency to underrate Bresch—to see an attractive, fashionable woman executive and assume those are her best qualities. “What they just really don’t understand is that it’s got nothing to do with sex, nothing to do with male vs. female,” says Mark Greene, a partner at Cravath Swaine & Moore, which has represented Mylan in M&A deals. “She’s the most knowledgeable person in the room on the subject matter. People are caught off guard.”

Bresch rolls her eyes at the controversies, characterizing them as the inevitable cost of making tough decisions. “I just think all that’s built a lot of character,” she says.

Growing up in a political family, Bresch developed a tough shell. During one state legislative race in her teen years, her face was plastered across town as part of a campaign against her father; her first week of high school, she had to cross a picket line—led by her science teacher—of union members complaining about Manchin. The Italian-American family was a frank-speaking, often chauvinistic bunch, by their own description, but also easy-going, and they frequently let loose in the company of their West Virginia neighbors. “There was a wild and crazy side,” says one family friend, famed University of Alabama football coach Nick Saban.

Bresch joined Mylan almost by accident. After graduating from West Virginia University, she taught aerobics in San Diego before moving back to the “Wild and Wonderful” state as a 22-year-old newlywed in need of a job. Her well-connected father ran into his friend Milan Puskar at a basketball game and finagled her an interview at Puskar’s drug company. Dropping by Mylan’s executive offices, then located in a double-wide trailer in Morgantown, Bresch walked out with a job typing labels in the factory basement.

Mylan was a local success story, a company formed in 1961 by a pair of Army vets who distributed medicine out of their car. In the early 1990s the concept of a generic drug—a cheaper copy of a branded medication whose patent had expired—was still new and nebulous. So after working her way out of the basement and into business development, Bresch became an expert on the Hatch-Waxman Act, a 1984 law that basically created the modern generic-drug industry by giving generics a special, faster approval process. CEO Puskar eventually dispatched her to lobby Congress.

But responsibility didn’t bring respect. Bresch’s mother, Gayle Manchin, says Bresch had to put up with a sexist culture at Mylan that reinforced the glass ceiling through demeaning treatment of women. “I’m going to use the term ‘sexual harassment,’ ” Gayle says, adding, “I don’t think that the men in charge there ever, ever would have said in a million years that Heather would be CEO.” Bresch says harassment is too strong a term but notes that it was an “old boys’ club” environment: Still, she says, “I never felt that I couldn’t hold my own.”

Bresch’s arc changed after Mylan named Coury, an industry outsider, as its CEO in 2002. At first it looked as though Bresch might be pushed out of Mylan entirely. Weeding out Mylan’s upper ranks, Coury eyed Bresch as a prime target. He marched into her office to tell her “she was the most overpaid and should be looking for another job,” Coury recalls. Bresch had been thinking of trying a new career. But after Coury’s tough talk, “I said, ‘Well, shit, if I quit now, he’s gonna think he scared me off—like he’s right and I bring no value,’ ” Bresch says.

Bresch strove to outwork her peers and showcase her exhaustive knowledge of the industry. Pregnant with her second child, she powered ahead, even dialing into conference calls from a hospital room just after her son was born. “She just had balls,” says her assistant of 14 years, Laurie Marquis. Coury eventually acknowledged Bresch’s talent—“I was moved,” he says.

One of her formative experiences came in 2004, when Mylan was hit by a hostile takeover attack, from activist Carl Icahn; Coury tasked Bresch with keeping Mylan’s other shareholders from joining Icahn’s side. Icahn eventually backed off, but Bresch says the battle crystallized for her the tensions between the priorities of Wall Street—including maximizing share price in the short term—and Mylan’s own goals. “We really were run more like a family-owned [company],” Bresch says. “We don’t have the same view that Wall Street does.”

In 2007, Mylan scored the deal that would take it global—the $6.7 billion acquisition of German drugmaker Merck’s (MRK) generics business, which had more than double Mylan’s revenue. Coury put Bresch in charge of the integration, promoting her to COO. Skeptics compared the deal to a python swallowing a Volkswagen: Bresch, however, impressed non-believers by summiting with managers across Mylan’s 139 new countries on weekly conference calls (6 a.m., Pittsburgh time). “They rallied, and everyone played above their head, and no one more than Heather,” says Alan Hartman, a partner at Centerview who advised Mylan on the deal.

It was during this odyssey that the Heather Bresch situation surfaced. The October 2007 news release announcing Bresch’s promotion declared that she had received an MBA from West Virginia University; by December, the Pittsburgh Post-Gazette reported that WVU had altered her transcripts and awarded her degree retroactively. Joe Manchin by then was West Virginia’s governor, and the implication of cronyism tainted Bresch just as she was emerging as a corporate leader.

A subsequent investigation by the school stripped Bresch of her degree. Its 95-page report concluded that administrators had given Bresch grades “pulled from thin air” because of her “high profile”—but it didn’t directly fault either father or daughter. “I certainly to this day believe I did everything I needed to do to get my degree,” says Bresch. By 2010 the benefits of the Merck acquisition were flowing to Mylan’s bottom line, and people stopped caring as much about Bresch’s business school pedigree. “Mylan’s board decided it wasn’t a requirement for the job, and Wall Street moved on,” says David Buck, managing director and pharmaceutical analyst for Northland Capital Markets.

Bresch’s leadership on the Merck deal made her the clearest candidate to be Coury’s successor. Still, Coury shocked Bresch and the Mylan board when he informed them, in the fall of 2011, that he’d be handing over the reins. When Coury announced the change on an earnings call in October, analysts’ first question was, “Why now?” Coury retorted, “The real question is, Why not now?”

Some investors and analysts believe Coury was under pressure to kick-start Mylan’s stock price; shares had recently plateaued, and Coury had a troublesome tendency to overpromise on earnings forecasts and FDA approvals. His unabashed potty mouth (“I like four-letter words, and ‘cute’ is not one of them, okay?” he tells Fortune) also grated on many. The ascent of Bresch, a media-savvy executive who knew when to be politically correct and when not to be, smoothed some ruffled feathers. “They moved from being strange people you can’t trust to just being eccentric,” says Derek Taner, portfolio manager of Invesco’s Global Health Care Fund, of Mylan’s management.

But Coury did anything but retire. As executive chairman, he says, he retains four responsibilities: talent management, major M&A, dealing with “all the issues” (read: any controversies), and the not-so-minor task of “leading the strategic direction of the company.” He insists that Bresch “is the one that runs this company every day—period, said, done, dry!” But even his compliments have a way of minimizing her role. “You know what a woman can do for a home?” says Coury. “That’s what she’s done for this corporation.” (“I hate that,” groans Bresch. “He’s said that before and I’ve told him not to ever say it again.”)

The result: Bresch often looks like she’s merely Coury’s deputy. Some investors and analysts have concluded she’s irrelevant, referring to her as a placeholder or a figurehead when discussing Mylan. “Heather Bresch might be a very talented, loyal employee,” says Jeffrey Sonnenfeld, a leadership expert at the Yale School of Management, “but I don’t think anybody believes that she’s really the functioning CEO—that’s Coury.”

Executives who work closely with Mylan say that such dismissals underestimate her. She’s a key, eloquent voice in Mylan’s major strategic decisions, and her operational deftness has far exceeded her board’s expectations, says Mylan board member and former AmerisourceBergen (ABC) CFO Neil Dimick: “Her ability to lead—that we did not know.” Admits Hartman, the Centerview adviser: “Most people would have bet against” Bresch as a leader, “but she has an incredibly good gut feel of it.”

Bresch demonstrated that feel early on as CEO with a long-overdue brand overhaul, writing Mylan’s first mission statement, which articulated a vision to reach 7 billion people—in other words, everyone in the world—with Mylan’s medicines. The politician’s daughter also helped draft and rally industry support behind the 2012 Generic Drug User Fee Act, a law that funded more FDA inspections of generic-drug factories overseas. Bresch persuaded Mylan’s competitors to accept greater regulatory oversight and pay the government for the pleasure. GDUFA also gave a chance for Mylan to toot its own horn: After going nearly 50 years without any manufacturing-related product recalls, Mylan has the best quality record in the industry, outside experts agree.

Under Bresch, Mylan has more consistently met earnings expectations, investors say, and its stock is up 124% during her tenure, more than double the S&P 500. Bresch is particularly proud of the hidden gem she found during the Merck acquisition: the EpiPen, a 25-year-old pocket-size injector for alleviating potentially fatal allergic reactions. The product grossed less than $200 million annually before Mylan bought it. Bresch made it “my baby,” she says; last year it became Mylan’s first billion-dollar blockbuster product—a rare achievement for a generics company.

On governance, however, Mylan hasn’t looked as impressive. In 2012 the Wall Street Journal reported that Coury was regularly using Mylan company planes to fly to cities where his singer-songwriter son, Tino, was performing. (Coury and Bresch are granted personal use of the company aircraft under Mylan’s employment contracts.) As the Teva takeover battle was coming to a head, the Journal reported that Mylan had built its Pittsburgh offices on land previously co-owned by the lead independent director of the board—who sold it for $1 to a third party hours before Mylan bought it. Corporate ethics experts decried the previously undisclosed transaction as a conflict of interest involving a “related person.” Bresch tells Fortune the director was “gracious enough” to relinquish his interest in the plot before Mylan bought it. Bresch even blames Teva for planting the story “to make us look like bad people.” (Teva declined to comment.)

Bresch shrugs off these issues with striking ease. Comfortable in her scandal-thickened skin, Bresch says she has pardoned many colleagues whose dirty laundry might have led other employers to demand their resignations. As long as they didn’t break the law, she’s unfazed. “The easiest thing to do would have been to let somebody go or not hire them because it’s messy,” she says. “But you know what? Life’s messy.”

Mylan’s relations with investors have only grown messier during this year’s takeover battles. Mylan began its inversion last July, by acquiring part of Abbott Laboratories’ (ABT) international drug business. But when shareholders overwhelmingly approved the agreement in January, they largely missed or ignored an “anti-takeover” clause about the stichting. Of the more than a dozen analysts, investors, and governance experts polled by Fortune, only one remembered even reading about it. (Several struggled to pronounce the word, calling it a “stitching,” like a needlepoint pillow.) Mylan is now the target of two shareholder lawsuits claiming that references to the anti-takeover measure in the agreement were vague and misleading. (Mylan says the suits are meritless.)

A few weeks after the inversion was completed, Mylan set up the stichting foundation, whose charter gives its four-man board (chosen by Mylan) the right to combat threats to Mylan’s interests by calling in preferred shares worth up to 50% of the company’s voting rights. A “stealth” feature native to the Netherlands, the stichting is “an invisible fortress,” says Stephen Davis, senior fellow of the Harvard Law School Program on Corporate Governance. “It’s there to sort of short-circuit accountability to the investors.”

That’s exactly what happened in July, when the stichting sabotaged the Teva deal. Mylan investors who had salivated over Teva’s offer—which represented a premium of as much as 48% over their shares’ value—were left with a “sour taste in their mouth,” says Invesco’s Taner. Bresch and Coury told them that Mylan was a stakeholder company, not a shareholder company: It could consider the interests of their employees (who might lose their jobs) and patients (whose drugs might cost more if the merger reduced competition) alongside those of investors. And as Mylan said in the new articles of association it issued when it inverted to the Netherlands, some of its stakeholders “will have have interests that are different from, or in addition to” its shareholders’ interests. “It came across as we’ll do anything to remain independent, and basically screw the shareholders,” says Taner, whose firm is one of the largest owners of Mylan stock. Bresch’s response is a familiar one: “We don’t cater to Wall Street, and they don’t like that.”

Nor does Bresch subscribe to the Big Pharma playbook. The deal doesn’t conform to the shareholder-friendly formula currently driving other mergers in the sector: Mylan isn’t predicting an immediate earnings boost from the deal; Perrigo doesn’t have a hot new drug, and it won’t greatly expand Mylan’s share of the prescription generics market. The leader in “white-label” generic over-the-counter products, Perrigo dominates the market for cheaper, drugstore-brand versions of Advil and Neosporin. Owning Perrigo would thus make Mylan a more diversified health care company, putting it both behind and in front of pharmacy counters.

Bresch managed to sell that vision to a majority of her shareholders, who approved pursuing Perrigo on Aug. 28, with 66% of the vote (against the recommendation of influential proxy advisory ISS). It will be harder to persuade Perrigo’s shareholders to take the deal, especially since the sinking price of Mylan’s shares has sharply lowered the value of the bid. “This offer isn’t even in the right zip code,” Perrigo CEO Joseph Papa tells Fortune in an email.

Bresch will have until Nov. 13 (the deadline for Perrigo investors to tender their shares) to win them over. If she succeeds, the roughly $35 billion deal would be the largest hostile takeover in history, according to Dealogic. But if there’s one thing Mylan and Bresch are comfortable with, it’s hostility. Bresch slips back into plain-speaking West Virginia mode as she describes what will happen when—not if—the bid succeeds: “We will absolutely embrace them, and they will see and feel our authenticity.”

To see the full Most Powerful Women list, visit fortune.com/most-powerful-women.

A version of this article appears in the September 15, 2015 issue of Fortune magazine.

Editor’s note: This article has been revised to remove an anonymous quote. Also: An earlier version of this article stated that Mylan’s status as a “stakeholder” company allows it to place interests of employees and customers above those of shareholders; the article has been revised to describe its relationship with stakeholders more completely.

[fortune-brightcove videoid=4474150272001]