Eight years following the bursting of the housing bubble, Americans are not quite at ease with the real estate market.

Homeownership rates recently hit 48-year lows, with most commentators arguing that such a trend doesn’t bode well for the American economy. “In general, I think rising homeownership is a plus for the economy and it signals a strong economy. The fact that it is falling is generally not a good thing,” Mark Zandi, chief economist at Moody’s Analytics Inc, told the Wall Street Journal.

Adding fuel to this worrying fire is a report released Monday from Zillow, which showed that first-time home buyers are waiting longer than ever—six years—to make the move from renting to owning. Zillow Chief Economist Svenja Gudell attributed this problem to the fact that young people are struggling to “save for a down payment and qualify for a mortgage, especially while the rental market is so unaffordable all over the country.”

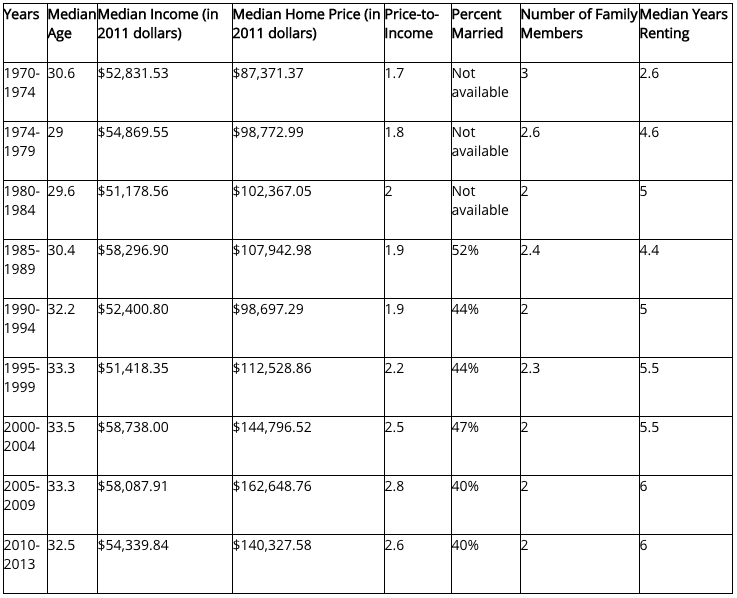

But is it really the case that young adults couldn’t afford to buy a home if they wanted to? Take a look at the following chart from Zillow:

As you can see, the median age of a first-time homebuyer hasn’t changed much in 20 years, while the median amount of time renting has only edged up by one year. What has changed is that home prices have increased a great deal, while incomes have remained stagnant.

But how important is this increase? Since 1990, the median home price has gone up roughly $40,000, while the median American income has only risen $2,000. That seems like a pretty big increase, but if you’re putting down 20%, that means a down payment is only about $8,000 more today than it was 20 years ago. Meanwhile, mortgage rates are less than half what they were in 1990 (4% today versus 10% in 1990), which means that the median American likely has a lower monthly payment, adjusting for inflation, than he had 20 years ago.

Maybe young adults aren’t buying homes simply because they don’t want to. For an unmarried person who hasn’t settled down or found a long-term career, homeownership doesn’t make a lot of sense. As Jed Kolko, Senior Fellow at the Terner Center for Housing Innovation, writes:

The share of young adults living with their parents increased in 2015…. One contributing factor is that 25-34 year-olds are decreasingly likely to be married or cohabitating with a partner, and – unsurprisingly – married or cohabitating young adults rarely live with their parents (just 2% do) compared with 31% of those who aren’t living with a spouse or partner. The decline in marriage among young adults is a long-term trend, pre-dating the recession.

There are many trends in housing that are difficult to explain, but the decline in marriage rates among young adults is hard to ignore. The lack of demand for new homes would also explain why housing starts remain 25% below the 30-year average, despite relatively high home prices. After all, what group is better positioned to gauge demand for new homes than the companies that build them?

What does this say about the housing market overall? As Kolko points out, there’s plenty of room for optimism. Just because young people are delaying marriage doesn’t mean they’ll never get married and start families. At the same time, the secular trend of higher divorce rates among seniors means that it’s actually the 65-74 year-olds who are leading the way in new household formations.

We may not be in the middle of an affordable housing crisis among young adults. Instead, we may very well be experiencing a cultural shift that the homebuilding industry is still adjusting to.