Everyone knows that the fate of the Russian economy is tied to oil prices, right?

So, if oil prices have rebounded from $45 a barrel to $70/bbl, that means that things aren’t so bad. And if the dollar now only buys 52 rubles instead of the 70 it bought three months ago, that’s surely a sign that things are getting better.

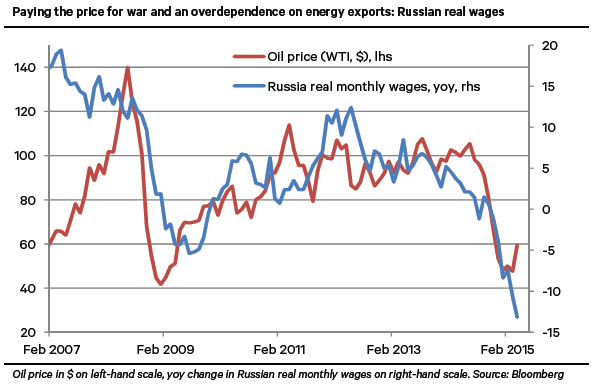

So the argument goes, at least in the short term. But this chart shows a very different story threatening to develop over the longer term, with profound consequences for President Vladimir Putin’s grip on power.

The blue line is the key one. It shows Russian incomes, adjusted for inflation. They were growing at nearly 20% in the years before the crisis, when Putin was able to redistribute gushing oil revenues freely through public sector wages and pensions.

Inflation had been on a steady if painfully slow downward trajectory for years before the ruble’s collapse last December exploded the price of imports. It peaked at 16.9% in March and may fall below 12% by the end of the year, according to Finance Ministry forecasts (much will depend on the harvest and its effect on food prices, which are 40% of the consumer spending basket).

The chart’s author, Berenberg Bank’s chief economist Holger Schmieding, concedes that the blue line isn’t going to get much worse from here, barring some unforeseen disaster. “But,” he says, “my rough guess is that Russia needs an oil price of over $80 a barrel to generate meaningful growth and a noticeable rise in living standards.”

That’s above the level expected by virtually anybody in the global oil industry these days. Goldman Sachs, for example, said last week it reckons the Brent global benchmark will average $58 this year, falling to $55 by 2020.

“While Russia’s domestic political situation still looks stable, this cannot enhance Mr Putin’s chances of clinging to power in the long run,” Schmieding says, pointing to the ominous news out of Moscow this week.

On Thursday Putin made sweeping extensions to the law on state secrets, meaning that anyone trying to report on the deaths of Russian soldiers in Ukraine can face up to eight years in jail (even if you’re a bereaved relative). And elsewhere this week, NATO released a detailed report on a new buildup of Russian troops on the Ukrainian border. Both look more like a doubling down bet on intervention and repression, rather than reform and economic revival.

As Schmieding says, “a rational Putin would use this (rebound in the ruble) to strengthen the Russian economy rather than to trigger new sanctions and capital flight through a further military adventure. But who knows what an autocrat is really up to?”