Does government spending help or hurt the economy?

Of the many questions economists wrestle with, this one attracts more attention than any other simply because it affects all taxpayers and consumers of government-provided services.

The Great Recession has been a grand experiment that economists will use for generations to understand how government stimulus and austerity affect the economy, especially during severe economic downturns. As economist Ed Dolan points out in a recent blog post, this question has dominated the upcoming parliamentary elections in the U.K.

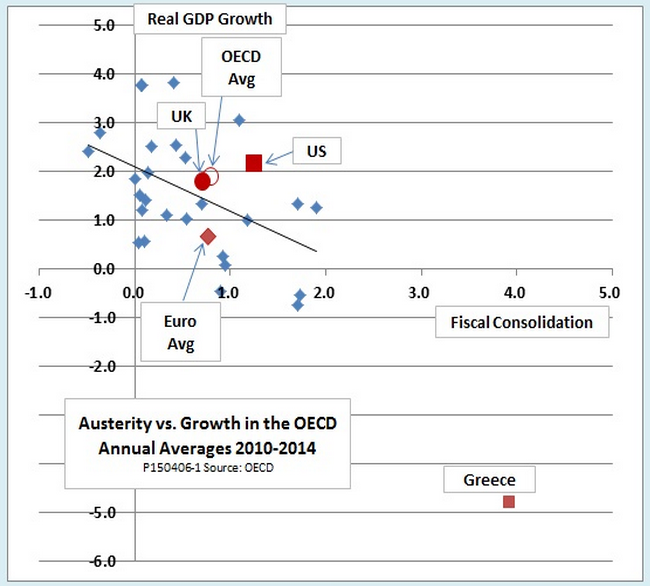

Dolan put together this chart, which includes the level of austerity (labeled on the x axis as “fiscal consolidation’) and economic growth:

As you can see, there is a very weak correlation between fiscal austerity and slower economic growth. Between 2010 an 2014, the United States, for instance, both practiced more austerity and grew more quickly than the average OECD country.

This might come as a surprise to those who follow the economic press closely. After all, the common narrative is that Europe was more eager to commit to austerity following the recession than the United States, where President Obama resisted calls from Congress to cut spending even after the Democrats lost control of Congress in 2010.

But what is often lost in the debate over debt and deficits is that so much government spending—roughly 40%—takes place at the state and local levels. Often, states are constitutionally required to run a balanced budget, so austerity during downturns is inevitable.

Second, Dolan adjusts government spending figures so that he can ignore so-called “automatic stabilizers” like unemployment insurance and the deficits that are incurred because of reduced tax receipts during a recession. Ignoring these factors, Dolan argues, gives us a better picture of what the actions of current policy makers have done to the economy.

Dolan uses this chart to argue that even though the British election appears to be dominated by the issue of austerity, “It [the U.K.] has had neither an exceptional amount of fiscal consolidation nor exceptional growth performance.” Therefore, he wonders “what the fuss is all about,” suggesting that there are more pressing issues British voters should focus on.

For Americans, the chart is instructive in other ways. One could quibble over whether eliminating automatic stabilizers is really a good strategy for analyzing the performance of public policy in the U.S. because extending unemployment benefits has been one of the few spending measures that Democrats and Republicans have been able to agree on during the recovery years.

Nevertheless, it’s informative to look at federal, state, and local government spending holistically and see that the U.S. actually engaged in more austerity and grew faster than its wealthy peers. The data overall show austerity most certainly didn’t lead to better growth, but it at least didn’t prevent the U.S. from outperforming the economic performance of other OECD countries.

Finally, it’s important to understand how America’s federalist system might distort the public debate over stimulus during the downturn. The stimulus package signed by President Obama in 2009 was huge in dollar terms—north of $800 billion. But when you consider that federal spending during downturns must make up for inevitable cutbacks in state spending, this figure seems much smaller.