Suspend your disbelief for a moment, fellow citizens. Here is a fact that defies everything you’ve come to know and believe about the workings of American policy: Big business is a mere featherweight when it comes to getting its way in the nation’s capital. In terms of shaping the broad domestic agenda, that seemingly formidable entity known as “corporate America” is, in reality, a piker. Don’t get us wrong. Washington, we know, is jammed with some 12,000 registered lobbyists (with many thousands more operating in the shadows) who daily, feverishly, often expertly work the levers of government to secure narrow breaks for their company clients. Legend are the stories of corporate giveaways tucked into the latest government-funding “Cromnibus”—a term that sounds as unholy and gluttonous as it is. In a marvel of behind-the-scenes tinkering, we are well aware, emissaries for Wall Street banks managed to peel back the Dodd-Frank rule squeezing their ability to trade derivatives, as other legislative wranglers worked their magic for telecom giants, defense contractors, and countless others.

All told, business interests plowed a staggering $2.78 billion into lobbying last year in hopes of shaping the policymaking process, according to an analysis by the Center for Responsive Politics. They spent hundreds of millions more on political campaigns. And yes, without a doubt, the money bought access to legislators, key aides, and agency officials. The access brought influence. The influence, in turn, was often reflected in changes the companies pushed for: targeted tax breaks, tweaks in legislation, stalled regulations, and new impediments for their business rivals. The tale is a familiar one.

But here’s the strange twist in the saga: For all the billions spent and the K Street swagger, for all the crab-cake receptions, phone-bank blitzes, and hallway huddles, for all the giveaways gotten and special deals secured, corporate America as a whole didn’t get any of the major items on its legislative wish list. None. As in zero.

Consider these four big-ticket asks: an overhaul of the tax code, new foreign-trade agreements, a long-term plan for federal debt reduction and the budget, and comprehensive immigration reform. Those are the long-stated legislative priorities of the Business Roundtable, an elite group of 203 leading CEOs and perhaps the closest thing to an organizational self for big business. What America’s corporate corpus truly wants now—and has demanded for years—are sensible, definitive resolutions to the core issues that divide Democrats and Republicans, President Obama and Congress, labor and management. Solve them, the argument goes, and economic growth will surge, driving unemployment down and wages up. “There’s nothing else that’s going to close the wage gap,” AT&T CEO Randall Stephenson, the Roundtable’s chairman, tells Fortune.

To date, all four of those boxes remain empty on the Roundtable’s scorecard. As this story went to press, congressional Republicans—far from considering their own comprehensive approach to immigration reform—were squabbling among themselves about how to stick it to President Obama for his post-election executive order on the issue (which stuck it to the Republicans). House leaders are now threatening to shut down the Department of Homeland Security in retaliation. (So much for rational budgeting.) Odds for tax reform, likewise, remain long. Progress on trade alone seems even remotely possible in the coming months.

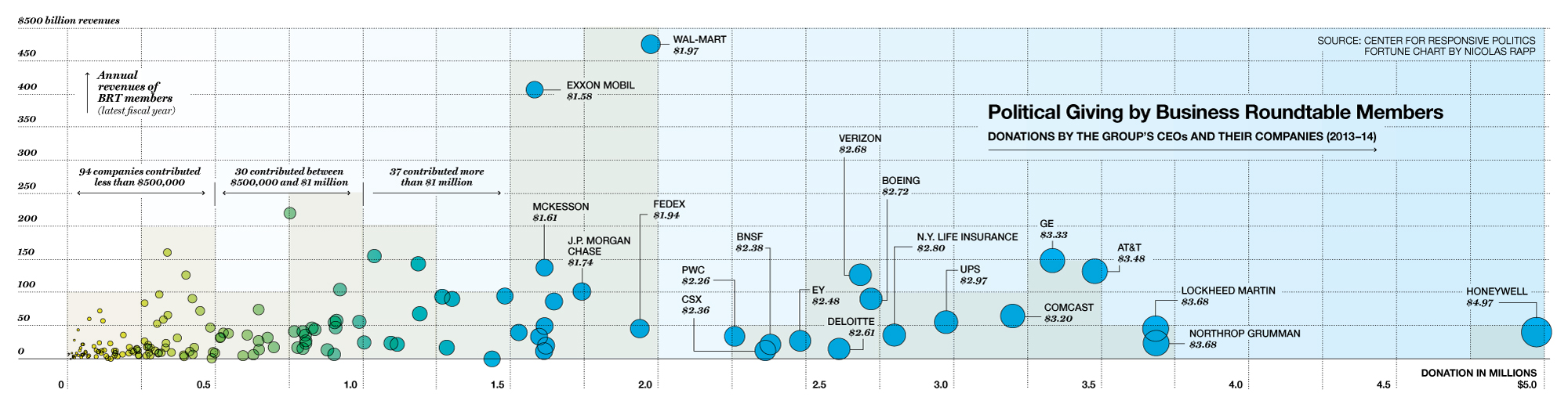

Click on graphic to enlarge

All of which brings up the question of why? Why can’t America’s corporate titans—a group whose economic impact is weightier than that of many entire countries, with a demographic that in theory ought to move political mountains—nudge the debate even modestly forward in Washington?

The answer, arguably, has very much to do with the Roundtable itself, a group that despite its high-powered members (or maybe because of them) has barely generated any light or heat. What follows is the story of how those CEOs lost their voice in Washington—how they stumbled into a confrontation with a new political order skeptical of their authority, one that shook loose their traditional grip on the Republican Party—and what they learned from that showdown. The question is, Did they learn enough to finally get the government to listen?

Big business can blame its current political impotence partly on its own past success. During the post–World War II economic boom, America’s corporate leaders helped glue together a consensus that recognized the need for regulation and accepted the legitimacy of organized labor—though that sense of a shared mission began to fray by the early 1970s, with the rise of stiffer competition abroad and new regimes in the federal government, such as the Environmental Protection Agency and the Occupational Safety and Health Administration. At the urging of the Nixon administration, chief executives including General Electric (GE) CEO Fred Borch and Alcoa (AA) CEO John Harper founded the Business Roundtable in 1972 to strengthen the hand of corporations.

Several business lobbying groups were operating already—notably the U.S. Chamber of Commerce, founded in 1912, and the even older National Association of Manufacturers (1895). But whereas the Chamber’s sprawling membership spanned the gamut from mom-and-pop companies to multinationals, the new Roundtable drew authority from its exclusivity, counting only the country’s top CEOs themselves as members. It was a sort of corporate priesthood. And as Mark Mizruchi, a University of Michigan sociologist, argues in his 2013 book, The Fracturing of the American Corporate Elite, the group achieved much of what it sought so quickly that by the dawn of the Reagan era the need for collective action had weakened. Its sense of urgency gone, the outfit earned a rep as a club for CEOs largely to rub elbows with one another and with the governing class.

During the opening years of the Obama presidency, the Roundtable stood out in large part for being the only major business lobby that was not outright hostile to the administration—remaining at the negotiating table, for example, for most of the fight over the President’s health care overhaul. That relationship soured in 2010, when the CEOs concluded that Obama’s economic team was only pantomiming respect for their policy concerns. The group suddenly found itself distanced from the Democratic leadership—just as a new assault was coming from the right. The Tea Party was now stoking a wave of popular revulsion over federal bailouts of big business.

At a moment when policymakers were trying to engineer a fragile economic recovery, CEOs were discovering that they had few friends left in Washington. And after the nation’s near debt default in 2011, the stakes of inaction had never seemed higher.

The results of the 2012 election promised a reckoning. President Obama won a second term on a pledge to stare down congressional Republicans. His plan was to use the year-end expiration of the Bush tax cuts as leverage to seize concessions from the GOP on a sweeping budget deal. Corporate chiefs viewed it as a moment of opportunity, and with many Roundtable members included, they formed an ad hoc group called Fix the Debt to rally Washington to go big.

It was an effort fraught with peril. Failure to reach a deal before New Year’s Eve would cause tax rates to spike across the board, a jolt that could pitch the economy back into recession. But this time, as another avoidable, Washington-made economic calamity loomed, Roundtable CEOs were done holding their tongue. Corporate concerns simply weren’t being heard. Congress “didn’t fear the business community, nor were they representing us,” says Tim Keating, the top lobbyist for Boeing, whose CEO, Jim McNerney, chaired the Roundtable at the time.

In a single day in early December, Team Boeing gathered 171 CEO signatures for a letter to congressional leaders warning that the impending damage would be “long-lasting, if not permanent.” And while other trade groups declined to weigh in on specifics, the CEOs went on to endorse a “balanced solution” that included new revenue from the individual side of the tax code.

To the chief executives, the missive was nothing more than an appeal for a return to sober-minded governance, based on compromise. Republicans and other business lobbyists read it very differently. “It was like a bomb went off,” one lobbyist with close ties to the Republican leadership says. GOP leaders felt the Roundtable was picking sides at an exceedingly dicey moment, undercutting Republicans’ negotiating position in the process.

The blast’s radius was wider still. Small-business interests—represented by essentially all the other leading trade associations—believed that the Roundtable was selling them out. Since many of their members pay business taxes through their individual filings, they viewed the Roundtable’s letter as a call by the corporate elite to shift the budget-balancing burden onto smaller operators through higher rates.

Tension had already been tugging at the traditional unity among the business trade groups. Earlier in the year, Sen. Rob Portman, an Ohio Republican, convened a clutch of trade-group heads for a private preview of a corporate-only reform package he’d been assembling. Attendees say Roundtable president John Engler, a former three-term Republican governor of Michigan, endorsed Portman’s approach, while others insisted it was a nonstarter: They could support only a reform push that tackled business rates on both the corporate and individual sides of the tax code, to ensure small companies didn’t get shafted. Now, with the December letter urging a “balanced” approach, the Roundtable appeared to be thinking only of its own corporate constituents.

The backlash was swift. Republican leadership aides lit up the phone lines to the Roundtable to make their objections known. The starkest response came from House Ways and Means chairman Dave Camp, a Michigan Republican, who fired off a direct and public reply to the group that same day, declaring, “Big business may support raising tax rates on small businesses, but I do not.”

In the carefully calibrated argot of official Washington, the Camp statement amounted to a haymaker. There are some in the GOP who still seem to feel the hurt. Kevin Brady, a Republican representative from Texas and a senior member of the Ways and Means Committee, says even today “there is some frustration lingering” among Republicans on the tax-writing panel over the Roundtable’s moves during the 2012 fiscal standoff.

The fact that a single letter from a trade group could reverberate so widely and for so long helps explain why the organization remained gun-shy nine months later when yet another bout of fiscal chest-thumping broke out between the President and House Republicans. In the fall of 2013, against the better judgment of their leaders, Tea Party–affiliated House Republicans managed to drag the party into an impossible position. The GOP insisted on shutting down the government, and potentially defaulting on U.S. debt, unless Obama agreed to a repeal of his signature health care overhaul. The President refused to blink, the government shuttered, and for 16 days Republicans watched their public approval crater before finally conceding defeat.

In the lead-up to the crisis, the Roundtable once again weighed in. But this time, in lieu of a directive prescribing a solution, the corporate chieftains hewed to an equivocal call for Kumbaya, urging “both sides to adopt a new spirit of cooperation.” Some in the group’s ranks pressed for a stronger stand against Tea Party recklessness. But Keating, the Boeing lobbyist, muffled the group’s response to avoid aggravating the wound between the CEOs and the GOP. “Every situation is an individual read,” he says. “Sometimes you need to throw gasoline on a fire, and sometimes you need to throw water.”

To critics, however, the episode was just another example of the Roundtable’s fecklessness. Saying nothing was just as bad as saying something provocative and not backing it up with muscle.

The battles with the Tea Party did provide the Roundtable with one important lesson. In politics, ultimately the only currency that matters is votes. The groups on the new right draw their potency from their ability to motivate a dedicated corps. Republican office-holders fear them. Big business had struggled to make that same claim: It wasn’t convincing.

Perhaps no event in the recent past frames that contrast as sharply as the shocking defeat of House Majority Leader Eric Cantor in the Virginia Republican primary last June. His vanquisher: a small-town economics professor named Dave Brat, who on the stump had bashed Cantor’s support for “the agenda of the Business Roundtable and the Chamber of Commerce.” The temperature within the House Republican conference changed immediately after that. “It was a wake-up call for a lot of interests in Washington that maybe a new day had dawned,” says House Financial Services chairman Jeb Hensarling, a Texas Republican.

One of the unlikely issues that had dragged Cantor to defeat, as it turns out, was his support for the Export-Import Bank. If you’ve never heard of Ex-Im, as it’s known, that’s fine with it. The federal agency was birthed in happy obscurity back in 1945, when Congress set it up to help the American industrial machine export its wares to a war-ravaged world. And it has remained a backwater ever since, offering credit financing to foreign buyers of everything from wines to jumbo jets. Today it employs 450 people—fewer than the Office of Surface Mining—most of them occupying the top five floors of a building that looks down at the White House from across Lafayette Square.

Yet the bank has become the staging ground for one of Washington’s fiercest lobbying fights. The brawl pits Boeing, which has tapped the agency to finance more than $1 billion in exports since 2007, against Delta, which argues that those deals use American tax dollars to subsidize its foreign competition. More significantly, newly assertive free-market ideologues in the GOP are framing it as a proxy war for the soul of the party’s economic policy. “The Bank of Boeing,” as they call it, is an indefensible bastion of corporate welfare that must be shut down.

The Roundtable might have hugged the sideline in a war dividing such corporate titans. But through a quirk in its membership—it counts no airline CEOs in its ranks—the group has come out swinging for Boeing and other heavy-equipment manufacturers that lean on the bank, including Caterpillar and GE. To hear the Roundtable tell it, at issue is nothing less than American competitiveness abroad: The U.S. can’t afford to disarm while our rivals pump up their own exports with similar credit-financing agencies.

This past September, California businessman Don Nelson flew to Washington to explain to his own congressman, Kevin McCarthy—who had succeeded Cantor as House Majority Leader and who had supported Ex-Im before Cantor’s loss—why he needed the bank. Nelson’s 80-employee firm, ProGauge Technologies, manufactures steam plants used for oil extraction. He says that for the past few years he’s relied on Ex-Im to finance roughly $115 million in equipment sales to Middle Eastern countries, deals that private banks wouldn’t back. McCarthy wasn’t swayed, calling the bank a giveaway to corporate powerhouses.

Hensarling, the bank’s most powerful foe in Congress, says he wants to end the bank “period, paragraph”—and in a warning to the Roundtable and other big-business lobbyists, frames the battle as “the first skirmish” in a broader struggle of Republican allegiance. He sums up his side’s philosophy succinctly: “I do not subscribe to the theory that what is good for GM is necessarily good for America.”

Strikingly, Hensarling’s less firebrand counterpart in the Senate, Richard Shelby, who chairs the powerful banking committee, shares his skepticism. “The bigger they get, they just seem to be for themselves,” says Shelby, a conservative Alabama Republican, reflecting the views of an electorate ever more disillusioned with the corporate elite. Polls bear that out. The Pew Research Center last year found that 78% of Americans believe too much power is concentrated in the hands of a few players, and most think those companies are not striking a balance between profit and the public interest. (That animus may explain the reluctance of chief executives to discuss their efforts to reclaim their Washington muscle. For this story, Fortune reached out to 12 CEOs on the Roundtable roster, including nine who sit on the organization’s executive committee. All except for Stephenson declined to comment.)

Stephenson himself acknowledges business’s diminished power in the halls of government. “We’re well past the day when a CEO calls a congressman and somehow has this great epiphany for the congressman to consider how he votes,” he tells Fortune. “What matters for congressmen today is that they hear from the grass roots.”

That comment isn’t sour grapes. It’s the seed of the Roundtable’s new strategy.

Before the AT&T chief took the organization’s reins, he directed his right-hand man in Washington, Jim Cicconi—a veteran of the Reagan and George H.W. Bush administrations who also sits on the Chamber of Commerce’s board—to inventory the Roundtable’s weaknesses. One leaped out. The organization has long touted its members’ collective economic might as the wellspring of its credibility in policy debates. But the group had no way of parsing its aggregate strength by congressional district. That is, when Roundtable representatives went to lobby a member of Congress, they couldn’t say how many people the group’s own members employed back in that lawmaker’s district—or how many facilities they counted there, or how much was invested, to say nothing of the breadth of their supply chains and third-party vendors.

“When you’re embarking on a more ambitious agenda, you want to have the ability to make it as effective as possible,” Cicconi says. “That starts with some basics: finding out where Roundtable member companies have employees and matching those up with congressional districts so you at least have a sense of your own presence in each state or district.” Indeed, the group’s lack of that visibility was tantamount to lobbying malpractice, so mapping the Roundtable’s resources became the first order of business for Bill Miller, the organization’s top strategist, who was recruited in 2012 after 12 years of building the Chamber into a prodigious lobbying force.

The capacity to cite those numbers, however, is only a starting point. Next, Miller wants to summon the people behind them to press the group’s agenda, since CEO voices don’t carry the weight they once did inside the Capitol. Many of its member companies are already doing that for themselves. At Boeing, McNerney successfully marshaled his company’s vast supplier network into a lobbying force that in 2011 helped secure a $35 billion Air Force contract to build a refueling tanker—the culmination of a decade-long war with European rival EADS for the job. And insurer Allstate just hired an outfit called RAP Index to survey its employees’ personal ties to pols (think: kids on the same Little League team), turning up 934 such connections it aims to redeem for lobbying leverage. Miller also plans a debut for the Roundtable’s new in-house grass-roots network, assembled by mining sites like LinkedIn to find workers and other “sympathetic individuals” like retirees who’ll echo the group’s message to lawmakers. “We start off with the idea that, theoretically, we ought to be able to reach 16 million direct Roundtable employees,” he says.

The Roundtable intends to make maximum use of these ground troops in the next major battle in its strategic war plan—the fight over new international trade agreements.

Miller is holding court in a small conference room in the Roundtable’s laboratory-white headquarters, occupying the eighth floor of the America’s Square building at the foot of Capitol Hill. The structure is a gleaming glass hive of corporate lobbying that sits catty-corner to the Teamsters headquarters, a marble mausoleum for a diminished foe, and Engler moved the group here from downtown three years ago to be closer to the action. It is Feb. 5, and the action in the trade debate is rumbling to life. An hour earlier the Roundtable fired off a “CEO action alert,” calling on its members to throw themselves, plus “your executives and employees, your Washington offices, and companies in your supply chain,” into the pressure campaign to give the administration new negotiating room on trade deals. Specifically, the corporate lobby wants lawmakers to hand President Obama what’s known as “trade-promotion authority” to guarantee that the complex pacts his team hammers out with foreign leaders will get a simple up-or-down vote in Congress. That wiggle room is seen as key to wrapping up work on the Trans-Pacific -Partnership—a 12-nation megadeal linking markets from Japan to Chile that make up 40% of the global -economy—and, probably later, another agreement with European countries.

The Roundtable’s challenge may look steep. Congress hasn’t considered a trade deal since blessing a trifecta of them in 2011, and with the turnover since, roughly a third of each chamber has never cast a vote on one. There’s also a real fear among free-traders that before the debate turns to the deals themselves, populist Republicans who may not oppose new pacts per se will balk on principle at handing any additional power to President Obama. “People who think we’re going to get [trade promotion authority] done are living in a dream world,” one Republican leadership aide tells Fortune.

Cummins CEO Tom Linebarger, who is leading the Roundtable’s trade push, acknowledges that the group has its work cut out for it. “If being populist means you’re against trade, it means I haven’t yet convinced the population at large that it’s good,” Linebarger told reporters at a recent Roundtable briefing. But he is nonetheless confident of a win. “The data is on our side. The problem is the stories are not yet compelling enough that people understand it and agree with it. That’s a job we have to do.”

The odds are with them. The issue, after all, represents a rare point of agreement between the White House, congressional Republican leaders, and the business community.

Miller is plotting strategy in tight formation with the administration’s economic team, hosting a weekly Thursday huddle in the Roundtable offices with coalition members, while checking in regularly with U.S. Trade Representative officials.

More than just the breadth of the President’s latitude in trade talks will be settled in the bargain. If this alignment of institutional power can’t get back on offense with a win here, forget the truly contentious stuff like tax and immigration reform.

Then again, if the Roundtable is successful, the words mounted and backlit on the wall of its headquarters—not just leaders.leadership.—will prove more than aspirational.