In June, economists will mark the 10th anniversary of the end of the Great Recession. But even as traumatic memories of that crisis recede, investors collectively have grown more jittery in anticipation of the next one. Market volatility has soared as relatively minor economic setbacks trigger frequent, dramatic selloffs. And over the past 12 months, at the same time that U.S. stock indexes have notched new records, mutual-fund shareholders have pulled out about $100 billion more from stock mutual funds and ETFs than they put in—a sign of mounting unease among Main Street savers.

Ask the pros and they’ll tell you that the caution underlying those jitters is justified. Indeed, 77% of economists expect a recession by the end of 2021, according to the National Bureau of Economic Research, with slowing corporate earnings in the U.S. and sluggish growth abroad stacking the deck against the economy. Investors tend to forget, however, that not all recessions trigger market crashes. David Kelly, chief global strategist at J.P. Morgan Asset Management, argues that the severe impact of the past two recessions has conditioned us to expect the worst. “We often assume when we have a bear market, it’s going to be a grizzly bear,” says Kelly. “But it might just turn out to be a koala bear.”

That said, even koalas have teeth, and nobody wants to get bitten. Here, Fortune’s writers take a look at five lesser-known economic indicators that offer reliable clues about a future slowdown, along with advice about how to react—without overreacting—to bears of any size.

The Yield Curve

When low rates augur bad news

For five days in late March, the three-month Treasury bill paid higher interest than the 10-year note—and cast a gloomy cloud over many investors’ outlooks. The event was an example of the one omen economists rely on more than any other to predict recessions: an obscure-sounding metric called the inverted yield curve. “Not only is it the most reliable, it’s really the only one,” says Rick Rieder, BlackRock’s chief investment officer of global fixed income.

The yield curve is the gap between interest payouts (“yields”) on long-term government bonds—say, 10-year Treasuries—and yields on their short-term counterparts, such as the two-year note or three-month T-bill. Normally long-term bonds pay more, because investors are willing to hold on to a bond for a decade only if they’re compensated more for their patience and risk—so the curve is positive. But occasionally, investors become convinced that interest rates and stock returns will be so low in the future that they’re better off buying long-term bonds now, to lock in today’s yields (even if they’re relatively low) and own an asset that will be less risky than the alternatives. They buy more, driving yields below short-term rates; the yield curve goes negative, or “inverts”; and economists and investors fear bearish times ahead.

Is the yield curve a reliable recession predictor? “Not only is it the most reliable, it’s really the only one,” says one investor.

It’s a phenomenon that has preceded the past nine recessions since 1957, according to economic data from the Federal Reserve. There’s just one big caveat: Flat or inverted curves have also generated at least three false alarms—most recently during the dotcom boom times of 1998, when, after an inversion, the stock market proceeded to rise 55% before it peaked. As Sam Stovall, chief investment strategist for CFRA, put it in a research note: “While all trout are fish, not all fish are trout.”

There’s reason to think this latest fish is one to throw back. Kelly of J.P. Morgan notes that historically, the Fed has to raise interest rates much higher than they are today before the curve inverts. “You need a bubble, you need excess, you need above-average growth before we have a problem,” adds Andrew Slimmon, managing director at Morgan Stanley Investment Management. Other experts argue that the indicator is no longer meaningful in the post–financial crisis era, as unprecedented bond buying by central banks has distorted bond spreads.

Still, when people tell Slimmon the predictor doesn’t apply anymore, he says, “My response is, ‘Explain to me why, every time in the past, this is consistent?’ ” One other trend that anxious investors often miss: Even should the yield curve invert again and stay inverted, investors will still likely have at least a year to adjust their portfolios before a recession hits. Adjusting might mean rotating into less highly valued stocks, keeping more in cash, and scooping up shorter-term bonds while their higher yields last. —Jen Wieczner

Auto Loans

America’s other subprime problem

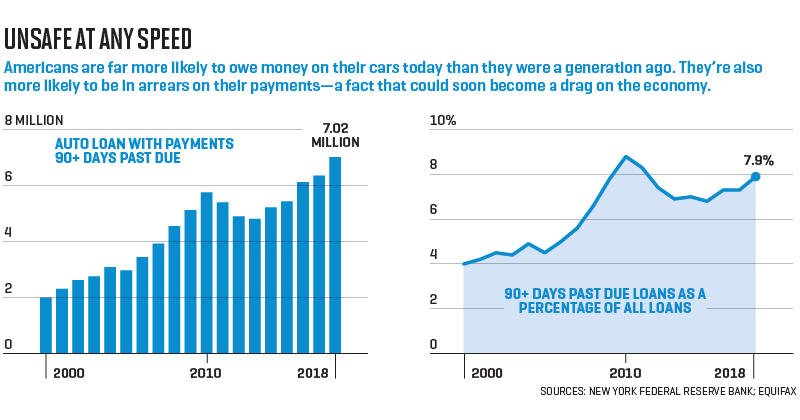

U.S. auto sales bounced back long ago from their Great Recession lows, but car buyers aren’t doing so well. At the end of 2018, more than 7 million Americans were in “serious delinquency,” or 90 days past due, on their auto loan payments, according to the Federal Reserve Bank of New York. That total represents an all-time high—and a further spike could send troubling ripples through the broader economy.

As the New York Fed noted, the numbers indicate “not all Americans have benefited” from a strong labor market. Borrowers between the ages of 18 and 29 had the highest delinquency rate of any age group, in another sign of how younger adults—often saddled with student debt obligations that sap their disposable income—are struggling to establish themselves.

But cash-strapped borrowers aren’t the only destabilizing factor. As big banks like JPMorgan Chase and Wells Fargo have stepped back from the sector, nonbank lenders that specialize in auto finance have filled the void. Many of them are “not regulated as prudently as banks are,” according to Mayra Rodríguez Valladares, managing principal at financial consultancy MRV Associates, and “have been loosening their underwriting standards.”

As a result, there is more borrowing than ever—with $1.27 trillion in loans outstanding at the end of 2018—and an unusually high percentage of borrowers are risky. Some 22% of auto loans, and 50% of those underwritten by auto-finance companies, qualify as subprime, according to the New York Fed. “We’re seeing loans where people are paying 29% interest for a loan on a 10-year-old [used] car,” says Eric Poe, COO of CURE Auto Insurance, based in Princeton, N.J. Wall Street has fueled this dynamic via its appetite for auto loan asset-backed securities, whose total outstanding value reached a record $222.8 billion in 2018, according to the Securities Industry and Financial Markets Association (SIFMA).

Overstretched young borrowers, loose regulations, iffy loans “securitized” for investors. If that pattern gives you a queasy sense of déjà vu, you aren’t alone: Analysts agree that the dynamics are similar to the subprime mortgage lending boom that preceded the last recession. The good news is that the auto loan market is far smaller than the mortgage market. (Subprime mortgages alone represented around $1.3 trillion of the mortgage market in 2007—larger than the entire auto loan market today.) And the effects of any crisis would be smaller too. Still, a spike in delinquencies would likely be bad news for investors in banks with auto loan exposure, for some insurance companies, and, of course, for the automakers themselves. Buckle up, and watch the road. —Rey Mashayekhi

China’s Consumers

Forget GDP—keep an eye on retailers and tourists

Over the course of a single day this January, Apple lost $74 billion in market capitalization, after warning investors that spending in the country it most relied on for growth—China—was slowing. Investors in Ford Motor Co. and Japanese electronics giant Panasonic endured similarly ugly days soon after, for the same reason, a reminder of how broad and bitter the impact of a Chinese slowdown could be.

The question is how to forecast that slowdown. The usual barometer of a nation’s economic health, GDP, is widely seen as unreliable in China. Local governments are rewarded for hitting growth targets set by the central government and so self-report impressive numbers; many commentators believe the central government also smooths out the data. Chang-Tai Hsieh, an economics professor at the University of Chicago, coauthored a paper earlier this year making the case that China had overstated GDP by about 15% in 2016.

Even if the figures were reliable, GDP arguably can’t fully capture a rapidly changing ecosystem in which consumer spending is overtaking heavy industry as an economic driver. “GDP doesn’t tell you if a project is good or bad, or if services are useful,” says Yukon Huang, a senior fellow at the Carnegie Endowment and former China director at the World Bank. “It just tells you what is being produced—and it doesn’t matter if it’s ghost cities or roads that don’t go anywhere.”

For a more trustworthy indicator, many investors look at household expenditures and personal income data, published by China’s National Bureau of Statistics (available on its website in English, as well as in news reports). Hsieh argues that those reports’ survey-driven methodology makes them harder to manipulate. Professional investors, meanwhile, reinforce that information with harder-to-find consumer data that’s completely outside the state’s control. Andy Rothman, an investment strategist at mutual fund firm Matthews Asia, cites import-export statistics and data on Chinese tourism spending in Japan as examples.

“GDP doesn’t tell you if a project is good or bad, or if services are useful,” says one China expert.

What story are Chinese consumers telling the world right now? It’s a cautiously upbeat one, and one that suggests they won’t be the trigger for the next recession. Income growth slowed in the fourth quarter of 2018, to 6.5% year over year, its slowest pace since 2016. Retail activity remains robust: In fact, consultancy eMarketer expects Chinese retail spending to hit $5.6 trillion this year—exceeding American retail spending for the first time ever. The warning sign to watch for: Nicholas Lardy, senior fellow at the Peterson Institute for International Economics, says investors should worry if income growth lags China’s reported GDP growth rate over multiple quarters. That would be a signal to reduce exposure to emerging markets, where business fortunes rise and fall with China. —Lucinda Shen

Corporate Debt

How much borrowing is too much?

Even in good times, servicing the interest on a hefty debt load can hurt a company’s profitability. In the face of a slowing economy or rising interest rates, you get a double or triple whammy. All of which makes it sobering to realize that global business debt now exceeds $66 trillion, up from $29 trillion before the financial crisis, according to consultancy McKinsey.

Total U.S. corporate debt remains near its all-time high of 73.5% of GDP, at about $15 trillion. Corporate bond debt hit $9.2 trillion at 2018’s close, according to securities industry estimates. And although interest rates have been low, much corporate debt represents higher-risk, more-expensive borrowing. At the end of February, more than 20% of U.S. corporate debt was rated in riskier junk categories, according to Fitch Ratings, and 46.7% was classified BBB, one step above junk.

Some industries are swimming in more debt than others. Patrick Finnegan, a senior director at Fitch Ratings, identifies health care, pharma, food and beverage, and energy among the sectors that have built up heavy leverage, with much of it going to fund mergers and acquisitions. Leverage isn’t inherently bad, of course, if a company’s earnings are strong enough. To figure out whether a given company’s debt load is manageable, McKinsey partner Susan Lund recommends checking whether its interest coverage ratio—revenue divided by interest payments—is at least 1.5. Lund estimates that 5% to 6% of U.S. companies fail to clear that bar, while as many as 25% of companies in emerging markets fall short.

That latter figure is troubling because businesses in emerging markets, including China, are particularly dependent on bank debt—that is, loans. This debt is largely opaque—it’s not easy for investors to tell how much companies have borrowed. And bank debt is more likely to be “variable rate,” meaning that interest payments on the loans go up if rates rise more broadly in the market.

To reduce exposure to corporate debt if rates spike, Tom Graff, head of fixed income and a portfolio manager at Brown Advisory, suggests steering clear of bond ETFs, whose prices could get very volatile if investors stampede out when interest rates rise. (Try open-end mutual funds or direct bond buying instead.) And in both the bond and stock markets, look for clean balance sheets: If a company has a heavy debt load, now’s a good time to walk on by. —Erik Sherman

Corporate Profits

As workers get more, shareholders could get less

For decades, it’s been one of Warren Buffett’s guiding principles: When corporate profits swell to a disproportionately large share of GDP, the Omaha sage has cautioned, the competitive nature of capitalism exercises a gravitational force that pulls them back to historical norms. Profitability shrinks, and stock returns become sluggish, or worse.

If that principle holds true, investors could be facing a rough ride. By some measures, Buffett’s gravitational shift is already underway. U.S. earnings peaked at 11% of GDP in 2012, but in the fourth quarter of 2018, they still accounted for 9.3%, or 2.6 percentage points higher than the 60-year average (see chart), suggesting they have further to fall. Analysts polled by FactSet forecast a year-over-year decline in earnings per share for the S&P 500 of 4.2% in the first quarter, and zero growth in the second.

The change reflects a tipping of the balance back toward labor. Since 2000, the share of GDP going to salaries, wages, and bonuses has dropped from 46% to 43%; lately, that trend is reversing. “America now has 7 million job openings, more than one for every unemployed worker,” says Ryan Sweet of Moody’s Analytics. That tightening labor market and the increased rates at which workers are leaving jobs for new ones are why wages are growing at 3.1%, twice the pace of 2010. Ordinarily, these trends would continue pressuring profits, and suppressing share prices, across the economy.

But there’s one investor who thinks we may have entered a new normal that could sustain higher profitability for a long time—and that investor, surprisingly enough, is Warren Buffett. At the 2018 annual investor meeting for Berkshire Hathaway, Buffett acknowledged that the Internet, social media, and data revolutions have spawned an “asset-light economy,” driven by tech giants that generate floods of profits from mere trickles of capital. Amazon, Apple, Google parent Alphabet, Facebook, and Microsoft dominate their industries, and their powerful brands and enormous scale swell their revenues per customer and lower their costs of attracting new ones. It’s not coincidental that those five companies now account for 12% of the S&P 500’s profits. While they, too, face rising labor costs, they don’t need nearly as much labor (or plants, or inventories) to generate hefty sales.

The takeaway: The profitability of the tech titans will decline more gradually than margins in other industries, which should help their stocks outperform too. Overall U.S. stock returns will likely be lower than what investors have grown used to. But if workers pocketing higher wages are a reason for that slowdown, that will be a silver lining. —Shawn Tully

A version of this article appears in the May 2019 issue of Fortune with the headline “Decoding the Market’s Messages.”